Crude Reality

March 16, 2026

Market Roundup for the Week

The week ending March 13, 2026, will likely be remembered as the point where geopolitical risk and macro-inflationary fears collided. What began on Monday with a "violent" shock to global energy markets—triggered by the effective closure of the Strait of Hormuz—concluded with the major indices posting their third consecutive week of losses.

Equity investors spent the week searching for a bottom. WTI Crude surged toward the $100 level, and the 10-Year Treasury Yield climbed to 4.28% as inflation expectations were recalibrated upward. Even with a mid-week attempt at a "relief rally" led by a few tech earnings beats, the weight of a 0.7% GDP revision and the looming shadow of next Wednesday's Fed meeting kept the bears in control. For now, the market appears to be tethered to every diplomatic headline coming out of the Middle East, while bracing for a Federal Reserve that may no longer have the luxury of a "wait and see" approach.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

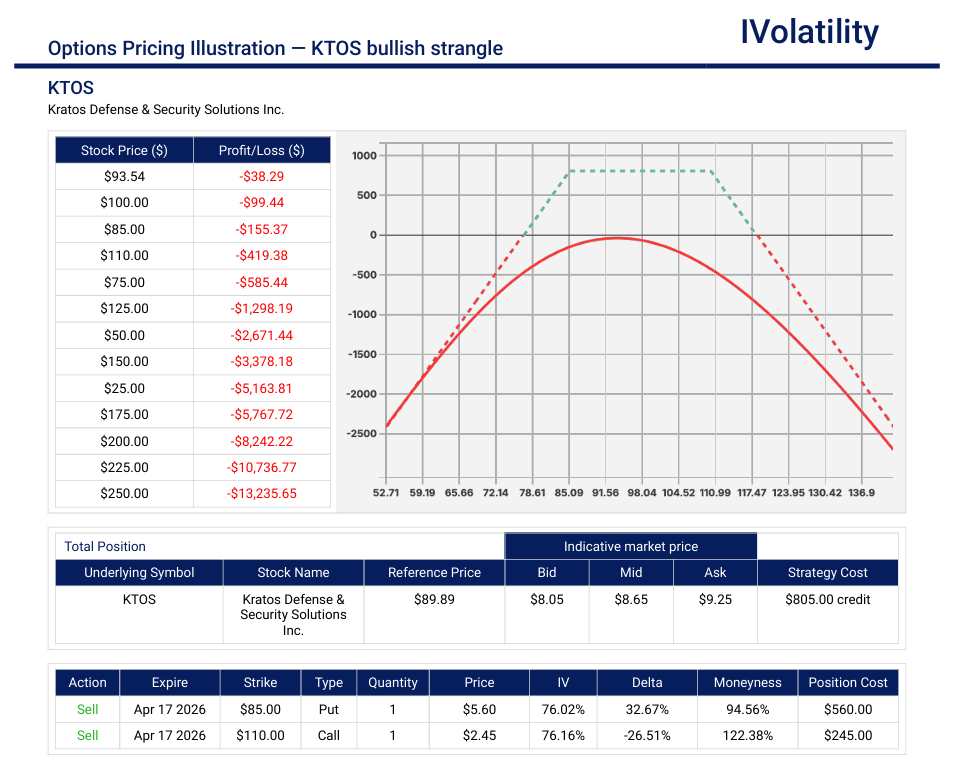

- Underlying: KTOS (closed at 87.53 on Friday, March 13th)

KTOS is a technology company that specializes in high-growth, "disruptive" sectors of the defense and national security markets. Unlike traditional "prime" contractors that focus on massive, multi-decade hardware platforms, KTOS centers its business on affordability and rapid prototyping, particularly in unmanned systems and space. - Strategy: Sell the April 85/110 strangle

- Rationale: This strangle leans bullish and, given the current market volatility and political conditions, a healthy premium can be harvested.

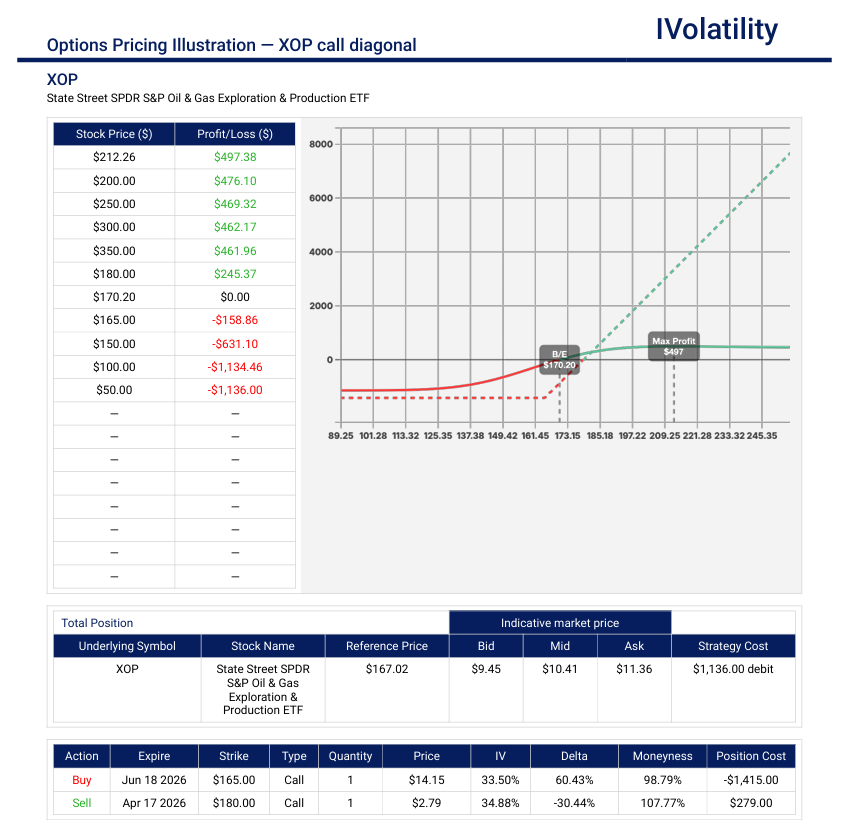

- Underlying: XOP (closed at 167.92 on Friday, March 13th)

XOP (SPDR S&P Oil & Gas Exploration & Production ETF) represents a specific, targeted slice of the energy sector: the upstream companies that find and extract oil and gas - Strategy: A bullish call diagonal

- Set up: Buy a slightly ITM call in June monthly expiration and sell a 30delta call against it in the April monthly expiration. For example, at current price of 167, buy Jun18 165call and sell the Apr 180call.

- Debit paid about $10.90

- Max potential value in excess of $15 with a few rolls between the expiration dates.

Movement of the Major Market Indices:

Equities faced a grueling week as a "triple threat" of geopolitical escalation in the Middle East, a sharp downward revision to GDP (0.7%), and a surging 10-year yield truly diminished risk appetite. The broader indices fell into correction territory, with the Russell 2000 hitting its lowest level of the year. The VIX retreated slightly from its Monday spike but remains at an elevated level of 27 as the markets head into next week's Fed decision.

| INDEX | UP | DOWN |

| SPY | -1.60% | |

| QQQ | -1.26% | |

| IWM | -1.79% | |

| DIA | -1.99% | |

| GLD | -1.12% | |

| BTC/USD | 3.70% | |

| TLT | 3.56% | |

| Crude Oil | 3.74% | |

| VIX | -7.86% |

Movement of the Major Market Sectors:

The sector rotation this week was a classic flight to defensives and energy. Energy (XLE) led the pack as oil marched toward $100, while Utilities (XLU) and Staples (XLP) provided the only other green shoots in a sea of red. Conversely, Consumer Discretionary (XLY) and Technology (XLK) were the primary laggards, punished by a combination of rising yields and cooling consumer sentiment following the disappointing retail and GDP data.

| SECTOR | UP | DOWN |

| TECH (XLK) | -2.14% | |

| FINANCIALS (XL) | -1.42% | |

| INDUSTRIALS (XLI) | -0.95% | |

| ENERGY XLE | 2.90% | |

| HEALTHCARE (XLV) | 0.33% | |

| UTILITIES (XLU) | 0.38% | |

| MATERIALS (XLB) | -0.80 | |

| REAL ESTATE (XLRE) | -1.60% | |

| CONSUMER STAPLES (XLP) | 0.40% | |

| CONSUMER DISCRETIONARY (XLY) | -2.24% |

The undisputed winner of the week was XLE, with WTI Crude jumping over 35%.

As growth projections for the first half of 2026 were slashed following the weak Jobs report, investors moved into defensive sectors like XLU, XLP and XLV. Despite the Broadcom bounce, the XLK sector finished down 1.2% as rising yields and global supply chain concerns from the Middle East conflict weighed on valuations. The week's laggard, XLY, fell as fears of higher gasoline prices and a slowing labor market dampened outlooks.

Notable gainers for the week of March 9th–13th:

In a week marred by a historic energy spike and the "Stagflation" shock of Friday's labor data, the standout winners were primarily those insulated by M&A activity or those demonstrating undeniable momentum in the AI infrastructure supercycle.

Notable losers for the week of February 9th–13th:

The week's "Stagflation" narrative and the geopolitical energy shock left nowhere to hide for sectors sensitive to fuel costs, consumer spending, or interest rate fluctuations. The laggards of the week represented a market that is aggressively pricing in a slowdown in domestic growth.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

Monday was a classic "wild ride" session, defined by a massive gap down at the open followed by a dramatic afternoon reversal fueled by geopolitical headlines.

The week began with a classic "V-shaped" session. Markets opened in a state of panic as the conflict in the Middle East intensified, with crude oil futures (WTI) gapping toward $120/barrel overnight. However, an afternoon comment from President Trump suggesting the war was "pretty much complete" triggered a massive short-covering rally that turned a deep morning rout into a solid green close.

By the bell, the major indices didn't just recover—they finished comfortably in the green, completely erasing the morning's deep losses.

S&P 500: Finished up about 0.81%, staging a dramatic comeback from an early -1.5% gap down.

Nasdaq: Led the major averages with a 1.38% gain, buoyed by a fierce rebound in large-cap technology and AI-related names.

Bonds: The 10-year Treasury yield edged slightly higher to 4.13%, as the bond market weighed persistent inflation risks from energy costs against safe-haven demand.

Gold: Remained volatile, holding firm near the $5,200/oz level as investors maintained defensive positions despite the equity recovery.

Oil (WTI): Experienced a massive intraday swing, collapsing from a midnight peak of $120 back into the $80/barrel range by the closing bell as "peace hopes" flooded the tape.

Bitcoin: Successfully tested support at the $70,000 level, stabilizing after early-session weakness in sympathy with broader risk assets.

Monday's Movers to the Upside:

- Live Nation (LYV): Jumped over 6% to lead the S&P 500 after news of a proposed settlement with the US Department of Justice. Investors cheered the likely removal of a forced Ticketmaster divestiture, significantly reducing a long-standing regulatory overhang.

- Xenon Pharmaceuticals (XENE): Skyrocketed over 46% following the announcement of positive topline results from its Phase 3 X-TOLE2 study for focal onset seizures.

- Hims & Hers Health (HIMS): Surged nearly 40% as it recovered a large portion of recent losses, fueled by shifting sentiment regarding the regulatory landscape for compounded medications.

- Nvidia (NVDA): Gained over 3% as the "AI-leader" attracted massive dip-buying after Morgan Stanley reiterated its bullish outlook amid the geopolitical volatility.

- Moderna (MRNA): Rose 5.0% on the day, continuing its strong 2026 momentum following leadership changes at the FDA's vaccine division.

Monday's Movers to the Downside:

- Ulta Beauty (ULTA): The day's biggest laggard in the S&P 500, plunging over 11%. The stock was hit by concerns over slowing consumer discretionary spend as "at-the-pump" gas prices hit their highest levels in years.

- Carnival (CCL) & Royal Caribbean (RCL): Cruise lines were hammered by the threat of rising oil prices, falling 8.0% and 6.5% respectively. Even with the late-day market recovery, the group struggled to bounce back as fuel-hedging concerns outweighed the "peace hope" rally.

- Southwest Airlines (LUV) & United Airlines (UAL): Major carriers took a significant hit, dropping over 7% and nearly 5% as the prospect of a prolonged Middle East conflict appeared to threaten to erase airline profitability through skyrocketing jet fuel costs.

- Old Dominion Freight Line (ODFL): Declined over 6%, leading a broader sell-off in the logistics and trucking sector. Higher operational costs for diesel-heavy fleets remained a primary concern for investors.

- Fair Isaac (FICO): Slumped 6.5%, continuing a period of volatility for the credit-scoring giant as investors worried that sticky inflation and high rates might finally dent consumer loan volumes.

- GE Aerospace (GE): Dropped over 5.5% following reports of potential durability issues with engine seals on the Boeing 777X, combined with profit-taking after the stock's strong run-up earlier in the year.

Tuesday's Markets and News:

Tuesday saw a cautious, narrow-range session as the market digested Monday's massive "Trump Reversal" and moved into "wait-and-see" mode ahead of Wednesday's critical CPI inflation report. While oil continued to retreat on G7 talks, the early enthusiasm for a quick end to the Middle East conflict began to face structural skepticism.

S&P 500: Slipped 0.21% as investors de-risked ahead of Wednesday's inflation print.

Nasdaq: Inched up +0.01%, buoyed by a resilient semiconductor sector.

Bonds: The 10-year Treasury yield held relatively steady, drifting down slightly to 4.12% following a successful 3-year note auction.

Gold: Challenged major resistance, gaining 1.1% to settle near $5,200/oz as geopolitical hedges remained in place.

Oil (WTI): Continued its descent, falling 12% intraday to settle near $83/barrel on news that G7 nations were considering a coordinated strategic reserve release.

Bitcoin: Maintained its bullish bias, climbing 1.0% to hold firm above the $70,000 threshold.

Tuesday's Movers to the Upside:

- Himax Technologies (HIMX): Surged 27.0% after a major automotive display contract win, highlighting continued strength in specialized semiconductor niches.

- Micron Technology (MU): Rose 3.4% following a partnership announcement with Applied Materials, reinforcing the "memory cycle" bull case for 2026.

- Firefly Aerospace (FLY): Jumped over 15% as private space sector sentiment improved following a successful test launch milestone.

- Oracle (ORCL): While it finished the regular session down slightly, the stock skyrocketed nearly 10% in after-hours trading after reporting record Q3 cloud revenue and providing bullish guidance driven by AI infrastructure demand.

- Hewlett Packard Enterprise (HPE): Gained over 3% on the back of second-quarter revenue guidance that exceeded analyst estimates.

Tuesday's Movers to the Downside:

- BioNTech (BNTX): Plunged nearly 18% following disappointing earnings combined with the surprise announcement that both co-founders would step down at year-end that appeared to rattle investor confidence.

- Waste Management (WM): Dropped 4.5% as profit-taking hit the industrials sector. Analysts noted concerns over rising operational costs for its massive vehicle fleet despite the dip in oil.

- United Rentals (URI): Declined nearly 6% as part of a broader cooling in the infrastructure and industrial services group following Monday's rally.

- Campbell's (CPB): Fell 4.0% after missing quarterly revenue expectations and lowering its fiscal EPS guidance, citing shipping delays and weak consumer snacks volume.

- PayPal (PYPL): Slipped over 2% as competitive pressures in the fintech space and cautious consumer sentiment weighed on the shares ahead of the CPI data.

Wednesday's Markets and News:

Wednesday was a session of extreme paradox. The day was centered on the February CPI report, which arrived exactly in line with expectations, briefly offering a "goldilocks" sigh of relief. However, that sentiment was immediately crushed by a historic escalation in the energy market. Despite the IEA announcing the largest emergency oil reserve release in its 50-year history (400 million barrels), oil prices actually rose as the market signaled that even these reserves might not be enough to offset the potential closure of the Strait of Hormuz.

S&P 500: Declined 0.42%, marking its third losing session in four days as valuation pressure mounted.

Nasdaq: Showed relative strength but still dipped 0.21%, kept afloat by a massive earnings-driven surge in Oracle.

Bonds: The 10-year Treasury yield jumped to 4.21%, up 5 basis points, as the bond market began pricing in "war-driven" inflation that the February CPI data had not yet captured.

Gold: Reversed Tuesday's gains, slipping 1.0% as the U.S. Dollar reasserted itself as the primary safe-haven.

Oil (WTI): Defied the IEA's massive 400-million-barrel reserve release, surging nearly 4.5% to settle at $87.19/barrel.

Bitcoin: Remained remarkably steady amidst the macro chaos, hovering just above the $70,100 mark.

Wednesday's Movers to the Upside:

- Oracle (ORCL): Skyrocketed 13.0% to a record high. The company delivered a "defining" earnings report with a $553 billion backlog and 22% revenue growth, proving that AI infrastructure demand remains decoupled from the broader macro slowdown.

- Uber Technologies (UBER): Gained 2.4% as investors looked for resilient platform models that could potentially pass through higher energy costs via dynamic surcharges.

- Hims & Hers Health (HIMS): Continued its momentum, surging another 16.9% as the market re-rated the stock following recent regulatory tailwinds.

- Victoria's Secret (VSCO): Rose 4.1% as the stock gained traction as a momentum play following positive analyst coverage regarding its multi-year turnaround.

Wednesday's Movers to the Downside:

- Kosmos Energy (KOS): Plunged over 18% after the company announced a massive public offering of 97.5 million shares to shore up its balance sheet amidst the volatile energy landscape.

- Dollar General (DG): Dropped 6.5% after being hit hard by the combination of sticky food inflation and the impact of higher gas prices on its core lower-income customer base.

- Newmont Corporation (NEM): Fell 2.5% in tandem with the broader pullback in precious metals.

- Campbell's (CPB): Continued its slide, falling another 3.8% as the "tame" CPI report actually highlighted rising "food at home" costs (up 0.4% monthly), raising fears of continued margin compression.

- Lowe's (LOW): Declined 3.0% following a neutral analyst rating and data showing that the building and garden supplies segment was the only retail category to see a year-over-year decline in February.

Thursday's Markets and News:

Thursday was a day of intense "risk-off" sentiment. While the morning's

S&P 500: Slumped over 1.5%, marking the lowest close of 2026 as investors fled to safety.

Nasdaq: Led the declines with a over 1.75% drop, pressured by rising yields and high-growth valuation concerns.

Bonds: The selloff accelerated; the 10-year Treasury yield spiked to 4.26% as the market priced in the inflationary power of $100 oil.

Gold: Surprisingly dipped nearly 1.5% despite the chaos, as the US Dollar surged to its highest level since last November, appearing to be acting as the primary haven.

Oil (WTI): Skyrocketed 10% to approximately $96/barrel following the newly-appointed Iranian leader Mojtaba Khamenei's vow to keep the Strait of Hormuz closed.

Bitcoin: Fell sharply by over 3%, slipping below the $68,000 mark as "risk-on" assets were liquidated across the board.

Thursday's Movers to the Upside:

- Chevron (CVX): Gained nearly 3% as energy-focused names became the sole beneficiaries of the spike in crude prices.

- Costco (COST): Rose over 1% and continued to exhibit resilience as a preferred consumer staple play during periods of economic uncertainty.

- Applied Materials (AMAT): Held up better than most chips, inching up 0.8% as investors focused on long-term infrastructure spend despite the macro noise.

Thursday's Movers to the Downside:

- Goldman Sachs (GS) & Boeing (BA): Both blue-chips fell nearly 4.5%, dragging the Dow lower as fears of a "drawn-out" conflict raised concerns over global lending and aerospace supply chains.

- Delta Air Lines (DAL): Dropped 2%, leading a broader 3.5% decline in the airline sector as the reality of sustained $100+ oil appeared to threaten summer travel margins.

- Harmony Gold (HMY): Slid over 5% despite hiking its dividend. The stock appeared to follow the broader pullback in the metals sector caused by the surging US Dollar.

- Salesforce (CRM): Declined over 2.5%, reflecting the general malaise in SaaS and enterprise software as the "SaaSpocalypse" narrative resurfaced amid rising interest rates.

Friday's Markets and News:

The trading week concluded on a heavy note as the "Friday the 13th" jitters felt all too real for equity bulls. While the morning attempted a bounce on rumors of a diplomatic "backchannel" to ease the Persian Gulf blockade, those hopes evaporated when the afternoon's downward revision to GDP confirmed that the U.S. economy grew at a sluggish 0.7% in Q4. This "growth scare" combined with energy-driven inflation fears sent the S&P 500 to its lowest close since last autumn.

S&P 500: Fell 0.61%, ending the week down more than 3% as the index hit its lowest level since November.

Nasdaq: Dropped 0.93%, weighed down by a significant delay in Meta's AI pipeline and the post-earnings fallout at Adobe.

Bonds: The 10-year Treasury yield edged up to 4.28%, reflecting market skepticism that the Fed can cut rates next week given the current oil spike.

Gold: Slid 2.11% to just over $5000/oz, as the US Dollar Index (DXY) broke above the 100 level, making dollar-denominated assets more expensive for overseas buyers.

Oil (WTI): Remained extremely volatile, gaining nearly 3% to settle around $98.50/barrel as the blockade of the Persian Gulf entered its second week.

Bitcoin: Remained a bright spot, climbing 4.6% to $72,777 and appears to continue to act as a non-sovereign alternative during the currency and energy crisis.

Friday's Movers to the Upside:

- Micron Technology (MU): Jumped over 5% to lead the S&P 500. Investors piled into the chipmaker ahead of its earnings next week, betting on continued AI-driven memory demand despite the macro gloom.

- Blackstone (BX): Gained over 4.5% as asset managers saw a late-day rebound, with some investors seeing value in private credit yields amidst the equity sell-off.

- Ollie's Bargain Outlet (OLLI): Rose over 4% following its Q4 report; the "extreme value" retailer is seen as a natural hedge for consumers pinched by $4.00/gallon gasoline.

- UnitedHealth (UNH): Clambered up nearly 2% as defensive healthcare names provided one of the few safe harbors in the Dow.

- Boeing (BA): Rose over 2.5% as investors looked past engine seal issues to focus on the long-term backlog and potential for defense-related revenue increases.

Friday's Movers to the Downside:

- Ulta Beauty (ULTA): The week's worst performer, plunging another nearly 12% after missing profit targets. The company's outlook highlighted a "noticeable pullback" in discretionary beauty spending.

- Adobe (ADBE): Fell over 7.5% following news of the CEO's upcoming departure and light guidance for recurring revenue. The stock sank to its lowest point in years.

- Meta Platforms (META): Dropped nearly 4% following reports that its next-gen AI model, "Avocado," has been delayed to May after underperforming against competitors in internal logic tests.

- Creative Media & Community Trust (CMCT): Cratered 44% to an all-time low, highlighting the intense pressure on REITs and commercial property developers as rates move higher.

- Carnival (CCL): Continued its descent, falling another 3.5% as the reality of $100 oil and a potential global recession hit the travel and leisure sector for a third straight day.

Notable Earnings to be announced March 16th–20th:

The schedule is lighter as the Q4/Q1 crossover season winds down, but several major discount retailers and global industrial players will provide critical data points on consumer health and international trade.

The actual date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday: DLTR / CMTL / BALY / SPSP / CDIX / ZBRA

Tuesday: FDX / STNE / TRVI / CNM

Wednesday: GIS / FIVE / M / VALN / XONA

Thursday: ACN / NKE / YRD / RLMN

Friday: CLLS

According to earningswhisper.com, the expectations are :

Beat: ACN / M

Miss: FDX / DLTR

Inline: GIS / NKE

Economic Calendar for Week of March 16th–20th:

This could arguably be the most consequential week for economic data for the quarter: a combination of industrial data, housing starts, and the centerpiece, the FOMC Interest Rate Decision, where the Fed must balance "stickier" energy-driven inflation against a cooling industrial backdrop. This could determine if the market can maintain its current "AI-driven" resilience in the face of skyrocketing energy costs.

The end of next week, Friday March 20th, is Quadruple Witching. This is the simultaneous expiration of stock options, stock index futures, and index options. It is not unusual to see elevated, and often, erratic trading volumes.

The daily schedule of notable economic data releases is:

Monday: March 16

- NY Empire State Manufacturing Provides the first look at March manufacturing health; a surprise drop might heighten recession fears.

- Industrial Production Tracks real output; a miss here might suggest high energy costs are already choking factory activity.

- NAHB Housing Market Data Gauges homebuilder confidence; essential for tracking the impact of stagnant 7% mortgage rates on supply.

Tuesday: March 17

- Retail Sales The "consumer pulse" check; weakness here combined with high inflation could signal a stagflationary environment.

- Business Inventories Reflects the balance between production and sales; high levels may indicate slowing demand and future production cuts.

Wednesday: March 18

- Producer Price Index (PPI) The "pre-game" for the Fed; a hot number here surely guarantees a hawkish tone from Powell later in the day.

- FOMC Interest Rate Decision The market expects a "Hold," but any shift in the "Dot Plot" toward fewer cuts in 2026 will likely trigger a bond sell-off.

- Fed Chair Powell Press Conference Every word will be scrutinized for how the Fed plans to handle the Middle East-driven oil spike and its inflationary impact.

Thursday: March 19

- Initial Jobless Claims The weekly health check of the labor market; any spike over 230k would be a major "risk-off" signal for equities.

- Philadelphia Fed Manufacturing Another regional health check; will confirm whether the Empire State (NY) data from Monday was an outlier or part of a broader trend.

- Existing Home Sales will show if buyers are returning to the secondary market; critical for mortgage and banking sector sentiment.

Friday: March 20

- No releases announced

Closing Thoughts

The "Red Queen" Markets: Running to Stand Still

In Lewis Carroll's Through the Looking-Glass, the Red Queen tells Alice: "Now, here, you see, it takes all the running you can do, to keep in the same place." Evolutionary biologists call this the Red Queen Hypothesis—the idea that organisms must constantly adapt and evolve just to survive against ever-evolving opposing systems.

As we wrap up this week, the market feels like it is trapped in a Red Queen race.

Despite the "breakneck" speed of AI infrastructure spend and the $55 billion allocated to emerging tech this year, the broader economy is "running to stand still." We see this in the 0.7% GDP print—a sluggish pace that persists even as corporate capital expenditures hit record highs. The "opposing system" here is inflationary friction: the $100 barrel of oil and the 4.28% yield are the evolutionary hurdles that are forcing the market to "run" faster just to maintain its current valuation.

In a Red Queen market, the winners aren't necessarily the ones running the fastest (the high-beta "AI dream" stocks that took a hit this week); they are the ones with the most metabolic efficiency.

In biology, metabolic efficiency is the measure of how well an organism converts fuel (food) into usable energy (ATP) with minimal waste (heat).

In the context of the markets, it is a metaphor for corporate survival in a high-cost, low-growth environment. When oil is at $100 and interest rates are high, a company's "metabolism" is under stress.

When the macro environment becomes "hostile" (rising yields and slowing GDP), the market stops rewarding speed and starts rewarding efficiency.

Speed translates to running faster (revenue growth) but burning more cash.

Efficiency translates to maintaining your position (market share) while using fewer resources.

In a Red Queen scenario, the companies that thrive aren't the ones trying to outrun the inflation; they are the ones built efficiently enough that inflation doesn't exhaust them.

Historically, when growth slows but costs rise, the "efficient" survivors have been those with pricing power and tangible assets. This week's rotation into Energy and Staples suggests the market is starting to value "survival efficiency" over "top-speed growth."

In the coming weeks, we may potentially see if the "Red Queen" forces the Fed to change the rules of the race entirely.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.