No Place to Hide

March 29, 2026

Market Roundup & The Week in Review

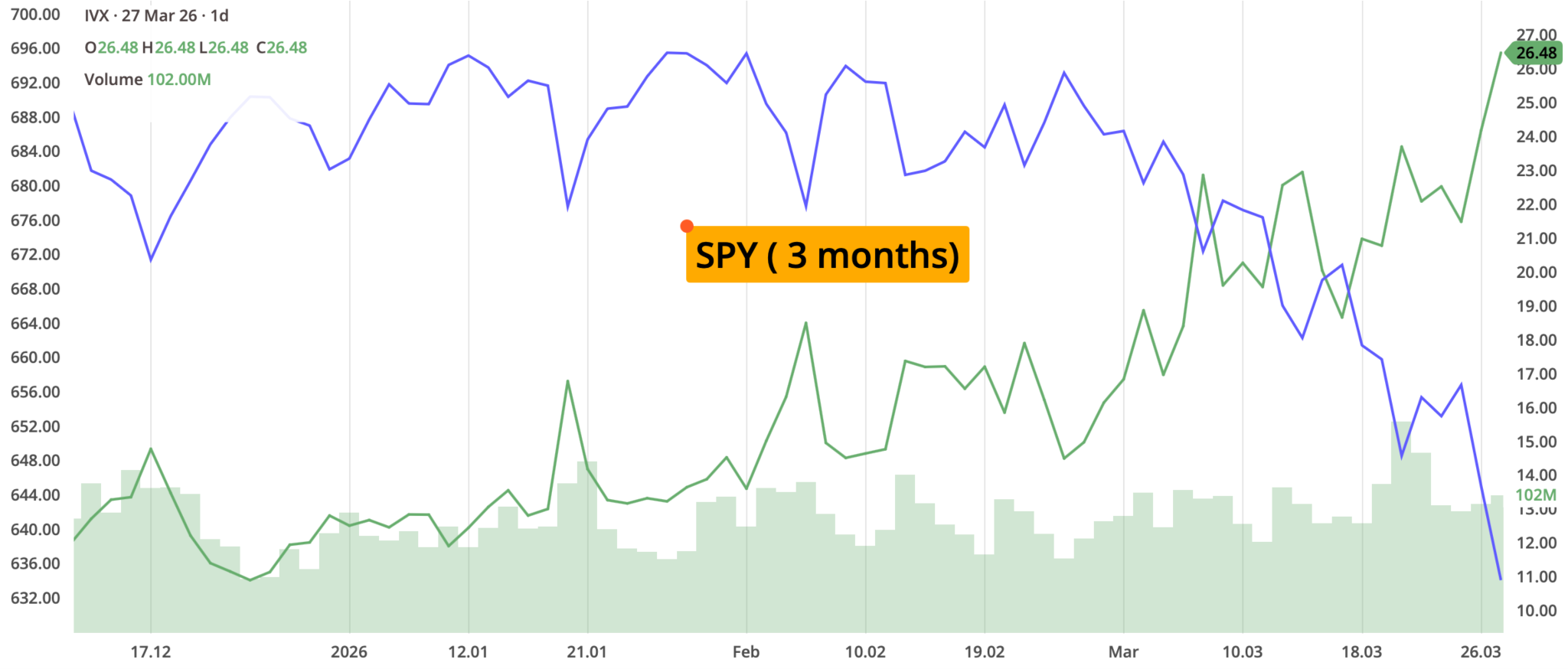

The final full trading week of Q1 2026 was defined by a decisive "Risk-Off" sentiment as the market collided with the stark realities of a prolonged Middle East conflict. The S&P 500 suffered a sharp technical breakdown, a decline that saw the index breach its 200-day moving average for the first time in over 200 sessions.

The "Forced Realism" narrative hardened this week as the Federal Reserve's "hawkish hold" (keeping rates between 3.50% – 3.75%) coupled with a spike in energy-driven inflation. With Brent Crude sustained in the triple digits and the Strait of Hormuz remaining a virtual "no-go" zone for commercial tankers, the market pivoted from betting on rate cuts to hedging against a potential "inflationary second wave."

This week was a volatile "roller coaster" driven by alternating headlines of diplomatic hope and military escalation in the Middle East. A fuller picture appears to be emerging of how the broader economy is faring amid the war with Iran, AI fears, and a slowing labor market...and it does not appear to please investors.

The Organization for Economic Coordination and Development said in its latest outlook that not only is the war with Iran kneecapping global economic growth, it's also reviving inflation. The OECD upped its forecast for the average headline inflation rate of the G20 economies in 2026 to 4%, higher than its prior projection of 2.8% back in December. The US-specific forecast was even bleaker: Domestic headline inflation will reach 4.2% this year, up 1.2% from the last forecast.

It's probably no coincidence that, at the same time, major Wall Street banks are recalibrating their recession odds. The magnitude and duration of flow disruptions through the Strait of Hormuz and the risk of growing damage to oil production, refining capacity, LNG fields, and liquefaction infrastructure appear to suggest a more persistent inflationary impulse, extending beyond a short-lived energy price spike.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

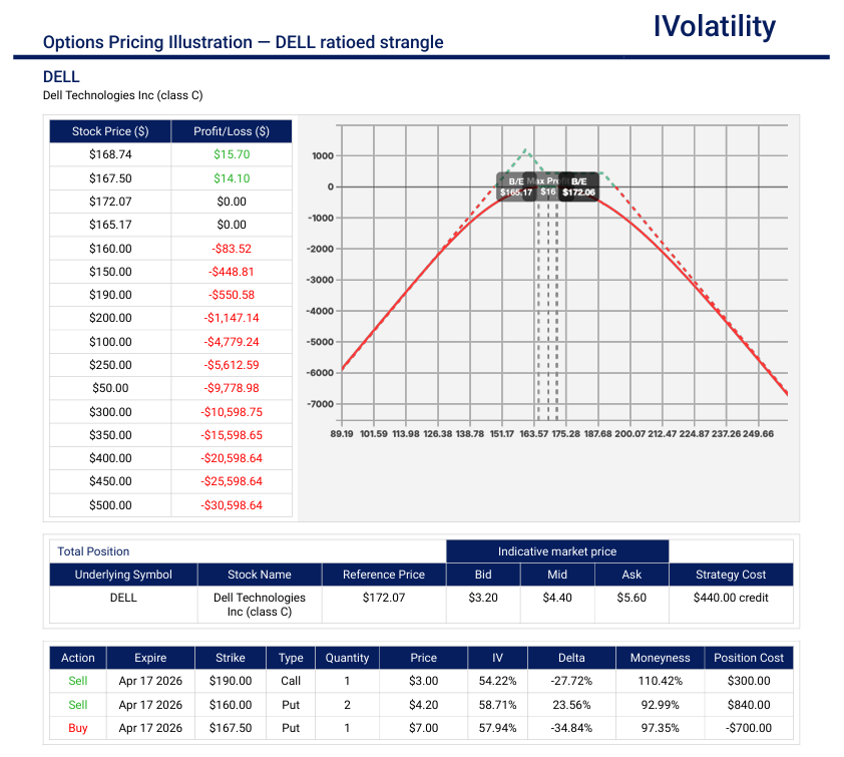

- Underlying: DELL (closed at 171.80 on Friday, March 27th)

Dell Technologies has established itself as a primary "flight to safety" within the technology sector, driven by a massive backlog for its AI-optimized servers and a dominant position in the high-end PC recovery cycle. While other high-beta AI names have faced extreme volatility, Dell's steady execution and relatively attractive valuation have turned it into a preferred institutional "safe haven" for exposure to enterprise hardware. - Strategy: Sell a ratioed strangle in Apr expiration

- Setup: Sell the 160/190 strangle and buy the 167.5/160 long put spread

- Credit collected: $440

- Max potential profit: $1190 if DELL expires at 160

- Breakevens: around 150 and 194

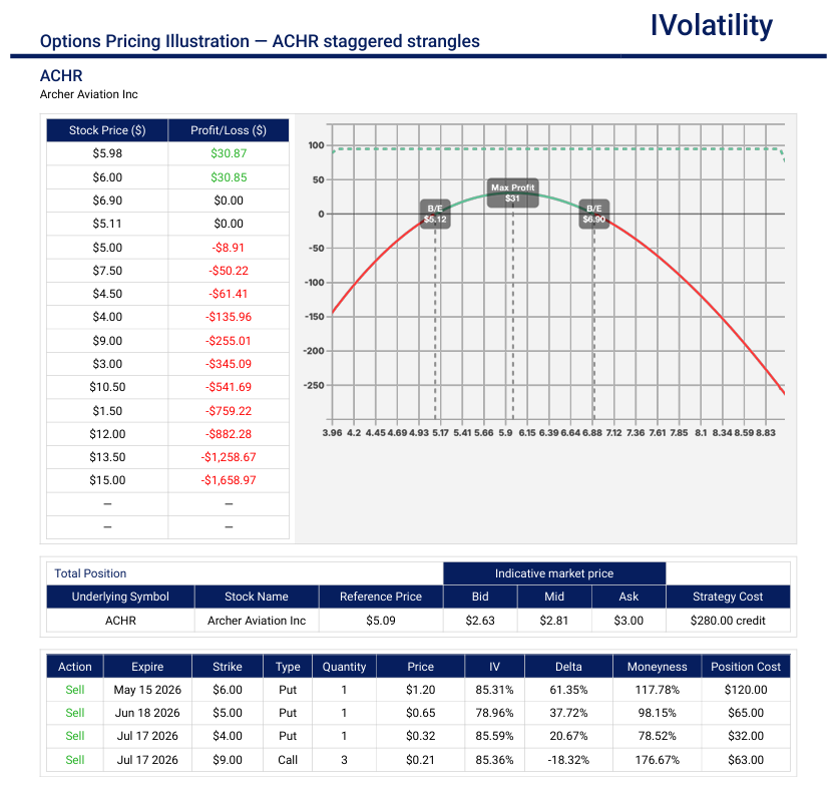

- Underlying: ACHR (closed at 5.09 on Friday, March 27th)

Archer Aviation (ACHR) is in the business of Urban Air Mobility (UAM). They are building a future where you can bypass gridlocked city traffic by taking an electric "air taxi" from a local vertiport. - Strategy: Staggered strangles

- Set up: Sell May15 6put / sell Jun18 5put / sell Jul17 4put / sell three Jul17 9calls

- Credit collected: $280

Movement of the Major Market Indices:

The final full week of March was characterized by a sharp "Risk-Off" correction. The technical damage was significant as the primary benchmarks breached key moving averages, driven by the "triple threat" of triple-digit Brent crude, a hawkish Fed hold, and the ongoing "flight to quality". The "Forced Realism" of triple-digit oil prices and a hawkish Federal Reserve combined to push volatility to its highest levels of the year.

| INDEX | UP | DOWN |

| SPY | -2.10% | |

| QQQ | -3.30% | |

| IWM | -2.90% | |

| DIA | -1.20% | |

| GLD | 1.15% | |

| BTC/USD | -4.15% | |

| TLT | 5.20% | |

| Crude Oil | 4.20% | |

| VIX | 14.80% |

The 10-Year Yield (+5.20%) surged to 4.39% this week, acting as the primary gravity for the QQQ (-3.30%). As the Fed holds firm on its "higher-for-longer" stance, the valuation expansion seen in early Q1 is being aggressively clawed back.

GLD (+1.15%) and Crude Oil (+4.20%) captured the geopolitical risk premium.

The VIX (+14.80%) closing at 28.30 signaled that the market is no longer "buying the dip" with confidence, but rather hedging for a sustained period of instability.

Movement of the Major Market Sectors:

The final week of Q1 saw a significant widening of the performance gap between "Risk" and "Refuge." While the broader indices struggled under the weight of rising yields, the "Crude Reality" of the energy crisis provided a massive tailwind to the inflationary sectors.

| SECTOR | UP | DOWN |

| TECH (XLK) | -3.85% | |

| FINANCIALS (XL) | -1.40% | |

| INDUSTRIALS (XLI) | -0.95% | |

| ENERGY XLE | 5.10% | |

| HEALTHCARE (XLV) | 0.45% | |

| UTILITIES (XLU) | -2.15% | |

| MATERIALS (XLB) | 1.20% | |

| REAL ESTATE (XLRE) | -4.30% | |

| CONSUMER STAPLES (XLP) | 0.80% | |

| CONSUMER DISCRETIONARY (XLY) | -3.10% |

- XLK (Technology): the "growth drain" was the week's primary casualty. The "AI Execution" theme faced its first real stress test as investors rotated out of high-multiple growth names and into "Quality" infrastructure. Despite the isolated strength in $DELL earlier in the week, the sector was hammered by the "Higher-for-Longer" interest rate narrative and a sharp rotation out of AI-growth multiples as the 10-year yield pushed toward 4.40%.

- XLF (Financials): While the "Higher-for-Longer" rate environment supports Net Interest Margins, fears of an energy-led recession began to weigh on the credit outlook for regional lenders.

- XLI (Industrials): Showed relative resilience. Defense contractors and domestic manufacturing continue to act as a hedge against global supply chain instability, though transport and logistics sub-sectors were hit by surging fuel costs.

- XLE (Energy): the "war premium", was the clear standout. As the "Hormuz Chokepoint" became a structural reality this week, Brent Crude's jump over $110/bbl drove the Energy sector to a massive decoupling from the broader S&P 500.

- XLV (Health Care): Remained the "Defensive Flight-to-Safety" of choice. While the broader market tumbled, Health Care saw steady institutional inflows as a capital preservation play.

- XLU (Utilities): Faced a dual-edged sword. While the sector benefits from the massive energy demands of AI data centers, it was punished this week by the spike in the 10-year Treasury yield, which hit 4.39%.

- XLB (Materials): Spike in volatility. Supply chain disruptions in the Middle East have sent copper and rare-earth prices higher, providing a floor for materials even as global growth forecasts are trimmed.

- XLRE (Real Estate): The week's biggest laggard. The combination of sticky inflation and rising borrowing costs has frozen the mortgage market, sending the sector to its lowest levels of the year.

- XLP (Consumer Staples): Outperformed on a relative basis. Large-cap staples with high pricing power are being used as "inflation sponges" by fund managers looking to hide from discretionary exposure.

- XLY (Consumer Discretionary): Under significant pressure. As national average gas prices surged over 30% this month, the "Consumer Fatigue" narrative is finally hitting the earnings of retailers and travel-related stocks.

Notable gainers for the week of March 23rd–27th:

While the S&P 500 struggled with its 200-day moving average, these names capitalized on the specific themes of Energy Scarcity and the Flight to Quality within the AI infrastructure space. In a week where the QQQ (-3.30%) and XLK (-3.85%) were under heavy fire, the gainers' list was dominated by companies with "Physical Moats" and proven execution in the AI server market.

- DELL rose nearly 9.5% and reached all-time highs as institutional capital fled $SMCI. The "AI Factory" backlog and strong Copilot+ PC projections made it the primary safe haven in Tech. Its move is particularly notable because it decoupled from its "AI peers." While others were sold off due to high multiples and rising yields, Dell was bought for its relative value and supply chain stability.

- XOM saw an increase of over 6% as the primary beneficiary of the $114 Brent Crude spike. XOM's upstream strength and Guyana production growth are acting as the market's favorite geopolitical hedge.

- VLO jumped nearly 6% as refining margins ("Crack Spreads") widened significantly with growing Middle East supply disruptions and subsequent increase in the premium on domestic U.S. refined products.

- LMT rose over 4% as defense contractors saw a renewed bid as the "Hormuz Chokepoint" shifted from a temporary skirmish to a structural military reality.

- NEM saw an increase of over 3.25%. As the VIX spiked to 28.30, NEM moved in tandem with GLD as investors sought hard-asset protection against currency volatility.

Notable losers for the week of February 23rd–27th:

The primary themes driving the "Losers" list were interest rate sensitivity and the contagion stemming from the accounting and regulatory crisis in the AI server space. In a week where the 10-Year Yield surged to 4.39%, any asset class dependent on cheap "long-duration" capital was aggressively repriced. Additionally, a "cleansing of the stables" in the technology sector appeared to occur as investors exited names with perceived governance risks.

- SMCI dropped over 22% serving as the "epicenter" of the week's tech volatility. Following the arrest of a co-founder and expanding DOJ probes, the stock faced forced liquidations from several major growth funds.

- PLTR shed over 8%. Despite strong government contracts, the high-multiple "AI Darling" was hit by the valuation squeeze as the QQQ breached its 50-day moving average.

- DLR dropped 7% making it the worst performer in the XLRE sector. This Data Center REIT was crushed by the dual-threat of rising interest rates and cooling sentiment in "speculative" AI infrastructure.

- NKE shed nearly 7% as part of the weakness in the XLY sector. As gas prices hit the "pain threshold" for the average consumer, discretionary spending forecasts for Q2 were slashed across the board.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

Stocks popped as hopes of a TACO trade roared back after President Trump halted attacks on Iranian energy infrastructure for the next five days. The President also touted "productive conversations" between the US and Iran, but Iran's Foreign Ministry denied any talks taking place.

- SPY (+1.45%): Rallied as the "inflation tax" fear subsided on the back of falling energy prices.

- QQQ (+1.82%): Led the large-caps as yields softened, providing a reprieve for high-multiple tech.

- IWM (+2.30%): The day's leader; small caps surged as lower fuel cost expectations brightened the domestic outlook.

- DIA (+1.33%): Strong gains driven by cyclical heavyweights like Goldman Sachs and Caterpillar.

- GLD (-1.10%): Sold off as safe-haven demand evaporated following the diplomatic headlines.

- BTC/USD (+3.40%): Traded as a "high-beta" risk asset, rallying in lockstep with the Nasdaq.

- 10-Year Yield (-1.30%): Yields fell to 4.33%, snapping a three-day rising streak.

- CRUDE OIL (-9.85%): Suffered its largest one-day drop of the year on the "5-day strike pause" news.

- VIX (-8.20%): Volatility crushed as the immediate threat of escalation appeared to wane.

Monday's Movers to the Upside:

- Palantir climbed 6.78% on news the Pentagon will adopt its Maven AI system as a core platform for weapons targeting.

- Synopsys gained 2.89% after Elliott Investment Management revealed a multibillion-dollar stake in the chip-design software company.

- Amazon rose 2.38% thanks to Project Hail Mary delivering an $80.5 million debut, marking a record opening for Amazon MGM Studios.

- DoorDash added 2.13% as it rolled out gas relief payments for drivers to offset rising fuel costs.

- Apogee Therapeutics surged 19.99% following positive Phase 2 results for its atopic dermatitis treatment.

- Norwegian jumped 6.17%, Royal Caribbean popped 5.81%, and Carnival moved 5.51% higher as easing tensions in Iran improved travel outlook.

- Super Micro Computer rose 5.16%, rebounding from recent losses tied to its cofounder's indictment.

- Tesla rallied 3.5% after Elon Musk unveiled a joint venture with xAI and SpaceX to build an AI-chip manufacturing plant.

Monday's Movers to the Downside:

- FuboTV fell 2.65% after disclosing plans for a 1-for-12 reverse stock split.

- Estée Lauder dropped 7.71% on reports of a potential deal with Spanish beauty firm Puig Brands.

Tuesday's Markets and News:

The Monday rally stalled as Iranian officials denied negotiations were taking place, reigniting stagflation fears as military operations continued.

- SPY (-0.35%): Drifted lower as the "peace rally" was questioned by market participants.

- QQQ (-0.80%): Underperformed as the tech sector reacted to the resumption of the yield climb.

- IWM (+0.54%): Remained resilient, holding onto Monday's gains better than large-cap tech.

- DIA (-0.17%): Modest pullback as energy prices began to creep back up.

- GLD (+0.45%): Bounced back as the "fog of war" returned to the headlines.

- BTC/USD (-2.15%): Surrendered gains as the "risk-on" sentiment from Monday proved short-lived.

- 10-Year Yield (+1.30%): Yields climbed back toward 4.39% on sticky inflation expectations.

- CRUDE OIL (+1.80%): Rebounded above $92/bbl as the strike-pause narrative weakened.

- VIX (+3.10%): Edged higher as uncertainty returned to the floor.

Tuesday's Movers to the Upside:

- Gap rose 3.24% after it partnered with Google's Gemini to let shoppers check out directly inside the AI platform, becoming the first major fashion brand to push into agentic commerce.

- Jefferies jumped 2.6% on reports that Japan's SMFG is exploring a potential takeover of the US investment bank.

- Applied Optoelectronics surged 18.94% on a new order for 800G data center transceivers from a major hyperscale customer, pulling optical peers Corning 8.43% and Lumentum 10.02% higher as well.

- US-based Netgear rose 10.88% following an FCC ban on imports of foreign-made consumer routers.

- CVS climbed 2.12% after reaching a settlement with the FTC over insulin pricing.

Tuesday's Movers to the Downside:

- Estée Lauder fell 9.85% after confirming merger discussions with Spanish fashion company Puig Brands.

- ImmunityBio dropped 21.12% after the FDA issued a warning over misleading promotions tied to its cancer therapy.

- Concentrix slipped 19.81% as an earnings miss overshadowed a revenue beat.

- Circle Internet Group tanked 20.11% and Coinbase fell 9.76% thanks to reports that a proposed crypto bill could ban rewards on stablecoin balances.

- SAP fell 4.03% following a JPMorgan downgrade, citing slowing cloud backlog growth and limited visibility into reacceleration.

- Software companies tumbled as Anthropic and AWS ramped up AI automation efforts. Salesforce fell 6.23%, Datadog dropped 5.15%, Microsoft slipped 2.73%, and CrowdStrike declined 4.92%.

Wednesday's Markets and News:

Choppy trading favored the upside on reports of a 15-point U.S. peace proposal and a potential one-month ceasefire.

- SPY (+0.60%): Gained as cyclical and value sectors found buyers mid-week.

- QQQ (+0.45%): Supported by a +10% surge in Intel, though capped by rising treasury yields.

- IWM (+1.22%): Outperformed the S&P 500 as investors rotated into "cheap" domestic value.

- DIA (+0.64%): Mirroring the broader Dow's gains on industrial and financial strength.

- GLD (-0.10%): Traded sideways as the Dollar remained the preferred "safe" harbor.

- BTC/USD (-0.04%): Remained pinned near $70k as retail demand showed signs of fatigue.

- 10-Year Yield (+0.15%): Yields remained "sticky" despite the equity rally, signaling bond market skepticism.

- CRUDE OIL (+0.75%): Drifted higher; energy traders remained wary of the "ceasefire" rumors.

- VIX (-2.50%): Volatility dipped slightly as the "peace bid" kept the bears at bay.

Wednesday's Movers to the Upside:

- Merck agreed to acquire Terns Pharmaceuticals in a $6.7 billion deal, marking its third multibillion-dollar acquisition in the past year, sending Merck up 2.59% and Terns 5.72% higher.

- Robinhood climbed 5.01% on news it approved a new $1.5 billion stock buybackprogram.

- Alibaba rallied 3.51% after China's regulatory administration signaled a crackdownon the country's food-delivery price war.

- Arm gained 16.38% after CEO Rene Haas projected its new chip could generate $15 billion in annual revenue by 2031.

- Intel rose 7.08% and AMD gained 7.26% as investors welcomed improving signalsaround CPU pricing and demand trends.

- Chewy jumped 13.26% after reporting strong earnings and upbeat 2026 sales guidance that topped expectations.

- Sarepta Therapeutics soared 34.98% after early clinical data from two new muscular dystrophy drug candidates showed encouraging results.

- JetBlue Airways rose 13.37% on reports it's exploring a potential sale to a rival.

Wednesday's Movers to the Downside:

- Pop Mart fell 22.14% as concerns over the sustainability of its Labubu-fueled growth overshadowed otherwise strong annual results.

- KB Home dropped 1.55% after cutting its 2026 home delivery outlook, with high mortgage rates and geopolitical uncertainty weighing on buyer demand.

- On Holding sank 11.19% on the news that its CEO will be replaced as the Swiss shoemaker tries to mount a turnaround.

Thursday's Markets and News:

Sentiment broke down as Iran rejected the peace proposal and the U.S. issued a stern warning, pushing the Nasdaq into a 10% correction.

- SPY (-1.75%): Cracked below its critical 200-day moving average as sell-programs triggered.

- QQQ (-2.30%): Heavily sold as $SMCI (-15%) accounting fears spread across the AI sector.

- IWM (-1.74%): Surrendered its weekly outperformance as recession probabilities climbed.

- DIA (-0.48%): Proved the most resilient but still finished in the red.

- GLD (+1.25%): Spiked as the "war premium" was aggressively re-priced back in.

- BTC/USD (-4.80%): Broke support at $65k, failing to serve as a digital gold substitute.

- 10-Year Yield (+1.20%): Surged as investors priced in an "inflationary second wave."

- CRUDE OIL (+3.10%): Jumped back above $100/bbl on the collapse of peace talks.

- VIX (+12.40%): Surged as the "Fear Gauge" reacted to the breakdown of technical supports.

Thursday's Movers to the Upside:

- Olaplex surged 51.13% after Germany's Henkel agreed to acquire the beauty company in a $1.4 billion deal.

- Jack Daniel's maker Brown-Forman climbed 9.75% on reports Pernod Ricard is exploring a potential takeover.

- Best Buy gained 4.65% amid speculation GameStop could acquire the big box retailer.

- Travel agency Navan jumped 43.28% following strong earnings and upbeat 2027 revenue guidance.

- Kodiak Sciences soared 74.77% after the biotech company revealed strong trial results for its diabetic retinopathy treatment.

- Avis Budget Group popped 12.97% and Hertz Global gained 9.15% as disgruntled customers are canceling their flights and just renting a car to travel instead.

Thursday's Movers to the Downside:

- Meta Platforms fell 7.92% and Alphabet sank 3.06% after the Mag 7 giants lost some major legal cases this week.

- AppLovin dropped 10.41% as weakening e-commerce spending and client churn weighed on growth.

- Pony AI declined 14.66% with revenue down 18% year over year, reflecting mixed quarterly results.

- Snap slid 10.69% after the EU opened an investigation into child safety and illegal activity on the platform.

- Furniture maker MillerKnoll sank 22.37% after issuing a weak outlook tied to fuel costs and Middle East shipping challenges.

- Worthington Steel fell 14.91% despite solid revenue growth, as margins came under pressure from tariffs and macro headwinds.

- Microsoft fell 1.37% as UBS cut its price target on weak 365 Copilot adoption, putting shares on pace for their worst six-month stretch since 2009.

Friday's Markets and News:

Total "de-risking" to end the week as bleak Consumer Sentiment data and surging gas prices fueled stagflation fears. The Nasdaq sank into correction territory yesterday, the Dow joined it there today, and the S&P 500 (down more than 8% from its all-time closing high in January) isn't too far behind, as traders come to terms with the idea of a longer-than-expected conflict with Iran.

- SPY (-1.40%): Closed at weekly lows; the technical breakdown from Thursday was confirmed.

- QQQ (-1.95%): Continued its slide as institutional "quarter-end" rebalancing hit growth stocks.

- IWM (-1.75%): Capped a fifth consecutive weekly loss, its longest losing streak in four years.

- DIA (-1.20%): Blue chips succumbed to the selling pressure in the final hour of trade.

- GLD (+0.85%): Reached $4,500/oz spot as investors fled "paper assets."

- BTC/USD (-3.25%): Faced heavy liquidations as part of the broader "risk-off" capitulation.

- 10-Year Yield (+1.10%): Finished at 4.44%, the highest level since July 2025.

- CRUDE OIL (+1.90%): Brent crude held above $104/bbl as energy security topped the agenda.

- VIX (+7.77%): Finished the week at 29.27, signaling a high-volatility regime for Q2.

Friday's Movers to the Upside:

- Brown-Forman rose another 5.79% as it entered merger talks with Pernod Ricard, while JPMorgan upgraded the stock to Neutral.

- Britain's most valuable company AstraZeneca climbed 2.8% after its experimental lung disease drug met targets in two late-stage trials.

- Entergy gained 6.82% on a deal with Meta to support a hyperscale data center in Northeast Louisiana.

- Tripadvisor jumped 1.61% as Bank of America upgraded the stock to Buy, pointing to activist momentum and strategic optionality.

- Construction company Argan surged 37.91% on a fourth-quarter earnings and revenue beat, with guidance topping expectations.

Friday's Movers to the Downside:

- Meta Platforms sank 4.02%, extending losses after losing two key court cases and announcing layoffs across multiple divisions this week.

- Carnival fell 4.31% despite strong earnings and record bookings, as unhedged fuel costs remain a key investor concern.

- Palo Alto Networks dropped 5.97%, CrowdStrike slid 5.87%, Datadog declined 7.9%, and SentinelOne fell 6.12% as Anthropic tested a new AI model with strong cybersecurity capabilities.

- Coinbase fell 7.06%, Strategy dropped 5.21%, and Robinhood declined 6.15% as bitcoin slid to a two-week low.

- Clear Secure declined 11.31% as the Senate moved to fund most of DHS, easing shutdown-driven travel disruptions.

Notable Earnings to be announced March 30th – April 3rd:

The earnings calendar is relatively light—a "quiet before the storm" as investors wait for the big banks to kick off the Q1 cycle in mid-April. However, there are several key movers that will provide critical data points on consumer health and enterprise spending. Investors may be looking specifically for how "sticky" inflation and high energy prices are impacting margins for discretionary leaders.

The actual date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday: nothing of note

Tuesday: BYND / PRGS / MKC

Wednesday: LW

Thursday: NKE

Friday: nothing of note

According to earningswhisper.com, the expectations are :

Beat: NKE / PRGS / MKC

Miss: BYND / LW

Economic Calendar for Week of March 30th – April 3rd:

As the turn of the month approaches, the economic calendar is loaded with "top-tier" data that may either confirm the stagflation narrative or offer the market a much-needed cooling-off period.

Notably, Good Friday (April 3rd) will see the U.S. Stock and Bond markets closed, but the Labor Department will still release the Non-Farm Payrolls report. This may create a high-risk scenario where the market can only react to the jobs data through thin overnight futures or the following Monday's open. All eyes will be on the Fed's commentary and the "Jobs Friday" data to determine if the high interest rates and energy shock are finally starting to crack the labor market.

The daily schedule of notable economic data releases is:

Monday: March 30th

- Fed Chair Powell speaks

As the market's primary "North Star" for interest rates, Powell's tone will be interpreted to signal whether the Fed is more worried about war-driven inflation or the recent cooling in the labor market. - Dallas Fed Manufacturing Index

This provides a real-time pulse on the Texas "Oil Patch"; a rising index here may suggest that the energy sector is expanding despite the broader manufacturing malaise. - NY Fed President speaks As a key architect of the Fed's current "Ample Reserves" framework, Williams' remarks may be scanned for hints on how the Fed plans to stabilize bond markets if yields hit the 4.50% "pain threshold."

Tuesday: March 31st

- CB Consumer Confidence

This index reflects the "Main Street" mood. With gas prices surging past, a significant drop here could signal that consumer spending—the engine of 70% of GDP—is starting to stall.

Wednesday: April 1st

- ADP Employment Change

Acting as the "litmus test" for private hiring, this report will show if small and medium-sized businesses are freezing headcount in response to higher borrowing costs. - ISM Manufacturing PMI

This is the definitive gauge of industrial health; a reading below 50 could signal a manufacturing recession, putting massive pressure on cyclical "Old Economy" stocks.

Thursday: April 2nd

- Initial Jobless Claims

This is the market's "High-Frequency" early warning system; any jump above the 210K level could suggest that the "cooling" labor market is turning into a "cracking" one.

Friday: March 20

- Non-Farm payrolls

Released while the stock market is closed for Good Friday, this "spectacularly" important number could decide the market's trajectory for the entire month of April. - Unemployment Rate

Currently sitting at 4.4%, this figure is being watched for the "Sahm Rule" trigger—if it drifts toward 4.6% or 4.7%, the "Recession" narrative will become the consensus view.

Something to think about...

At its core, a prediction market is an exchange where people trade "event contracts" based on the outcome of future events. Unlike a traditional stock market where a piece of an underlying is bought, in a predictive market a participant is essentially "buying" a probability.

These markets function as a "Truth Machine" by incentivizing accuracy. If you believe there is an 80% chance of a specific event—say, a ceasefire in Iran by May—you would be willing to pay up to $0.80 for a contract that pays out $1.00 if you're right.

If a contract is trading at $0.65, the market is collectively signaling a 65% probability that the event will occur. Because participants stand to lose real money if they are wrong, they are motivated to find the most accurate data possible, often outperforming traditional polls or "expert" pundits who face no financial penalty for being incorrect.

As investors navigate the "fog of war" in the Middle East and a fractured domestic political landscape, traditional polling and mainstream financial analysis are increasingly being sidelined by the obvious efficiency of predictive markets. Unlike pundits, who face little consequence for being wrong, participants in platforms like Kalshi and Polymarket have "skin in the game," creating a real-time, incentivized truth machine. These markets aren't just betting on sports; they are currently pricing the probability of a formal ceasefire in Iran, the specific timing of the Fed's next pivot, and even the outcome of the 2026 midterm primaries with startling accuracy. They often move minutes or even hours before the headlines hit the Bloomberg terminal, acting as a leading indicator for the VIX and the 10-year yield.

The real question for traders is whether these markets are truly prophetic or merely a sophisticated echo chamber of the most capitalized participants. When a prediction market shows a 70% chance of a "Suez-style" closure of the Strait of Hormuz while Crude Oil is only trading at $104, a massive "Information Gap" exists. For the disciplined investor, this gap is where the opportunity lies. Are you watching the charts, or are you watching the "crowd" that is betting on the outcome of those charts? In a world of deepfakes and geopolitical misinformation, the most honest data might just be the one that has a dollar sign attached to it.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.