Chip-Pocalypse Pivot

April 27, 2026

Market Roundup & The Week in Review

The week of April 20th–24th, 2026, will be remembered as the "Chip-pocalypse" Pivot. The market entered the week under a cloud of geopolitical tension and "risk-off" sentiment, as renewed friction in the Middle East sparked a sharp spike in energy prices and a retreat from historic highs. However, by week's end, those concerns were completely overshadowed by a tectonic shift in the technology sector.

While the early-week narrative was dominated by the Strait of Hormuz and a "war premium" on crude, the week ended in a landslide of bullish conviction. The catalyst was a massive surge in the semiconductor space, fueled by Intel (INTC) shattering expectations and reigniting the "AI proof of work" trade. This "Chip-pocalypse" of gains effectively wiped out the week's earlier losses, propelling the S&P 500 firmly above the 7,100 threshold and the Nasdaq to a fresh all-time record.

Markets transitioned from fearing an oil-driven inflation spike on Monday to embracing a tech-driven growth cycle by Friday's close. Despite the early-week jitters, the primary narrative remained centered on the AI-driven growth cycle and a highly anticipated earnings kickoff. Investors shifted their focus from geopolitical headlines to corporate fundamentals, with Tesla (TSLA) and Boeing (BA) leading the charge in a heavy reporting week. While crude oil prices fluctuated near $95/bbl, the broader market appeared resilient, supported by cooling core inflation data and strong early results from the financial sector.

The "Magnificent Seven" era continues to dominate, as investors front-ran next week's major tech releases by piling into semiconductor infrastructure.

Despite strong Retail Sales data suggesting a "hot" economy, Treasury yields compressed for the fourth straight week, with the 10-year finishing at 4.24%, clearing the path for growth stocks to soar.

As the indices push into uncharted territory, it's worth considering the "narrowness" of this rally. While it's easy to get swept up in the semiconductor euphoria—especially with Intel's 23% week—a distinct divergence might be spotted where sectors like Utilities and Consumer Discretionary are actually losing ground.

It could be argued that the most sustainable rallies are those that "lift all boats." When the market becomes overly reliant on a single narrative (in this case, AI infrastructure), it creates a high-stakes environment where any single miss from a heavyweight (like Microsoft or Amazon) next week could potentially ripple through the entire market. For self-directed investors, this is a time to celebrate the gains but also a time to re-examine the benefits of diversification.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

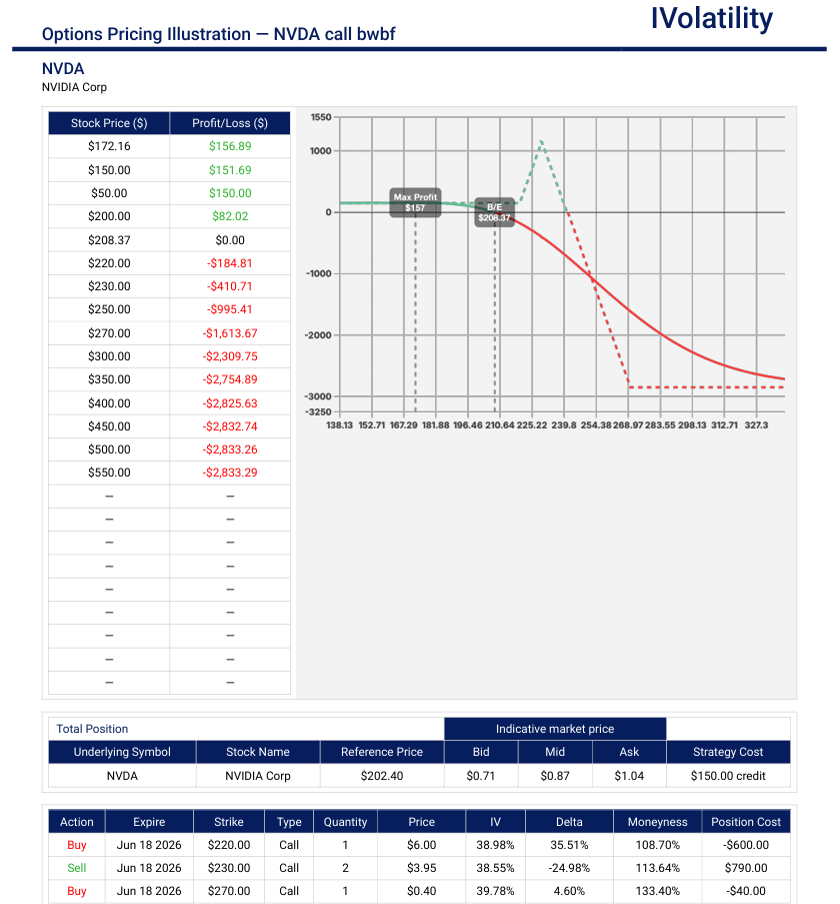

- NVDA (closed at 208.17 on Friday, Apr 24th)

After a record-breaking earnings report and reclaiming its $5 trillion market cap, NVDA is showing immense momentum. If an investor would like to enjoy further upside but hedge a bit, the following position could be considered. - Strategy: Broken-wing Call Butterfly

In the June monthly expiration, buy one 220call / sell two 230calls / buy one 270call

Premium collected about $1.60

Upside breakeven around 240 (20delta)

No risk to the downside

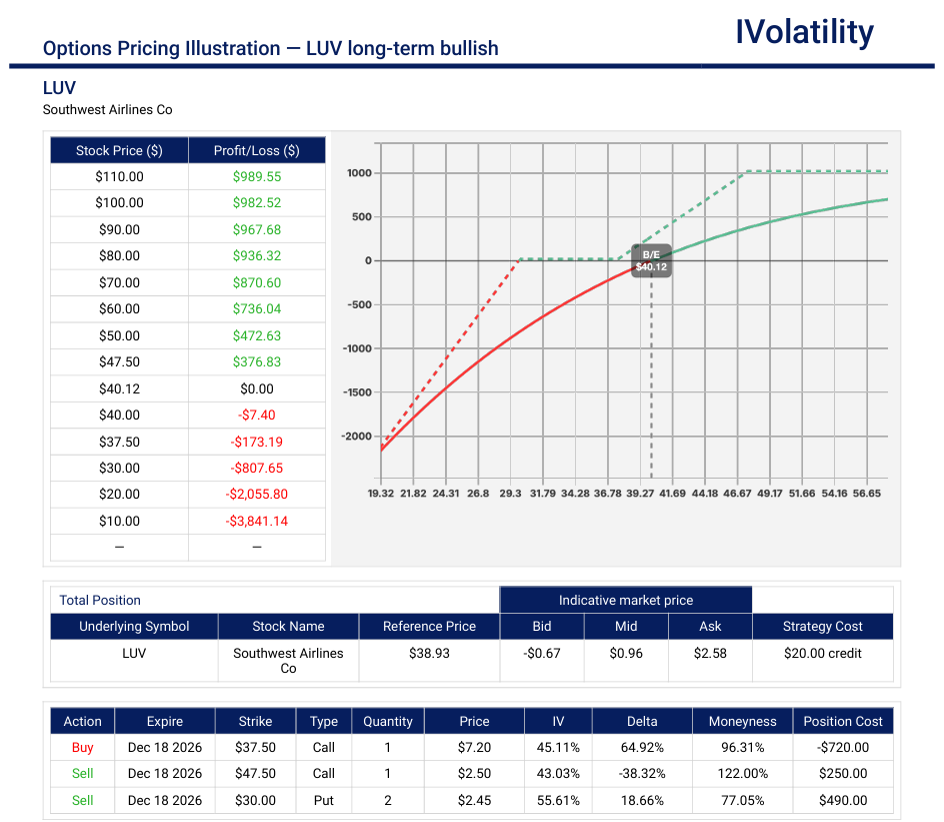

- LUV (closed at 39.43 on Friday, Apr 24th)

Transitioning to a long-term bullish stance on this underlying marks a significant pivot, especially given the carrier's recent historic shift in its business model. While the airline has faced pressure from activist investors and operational hurdles, the data from the first half of 2026 suggests the "New Southwest" is beginning to find its stride. - Strategy: Long term custom bullish position

In the December monthly expiration, buy one ATM call (37.5strike) and sell one OTM call (47.5strike) for about ½ the cost of the long call. Now sell TWO puts (30 strike) to cover the cost of the long call spread for a small credit.

Credit collected about 22c

Position delta about 63

Buying power needed about $1000

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | 0.55% | |

| QQQ | 1.50% | |

| IWM | 0.36% | |

| DIA | -0.44% | |

| GLD | 1.00% | |

| BTC/USD | -2.50% | |

| 10-year yield | -4.62% | |

| Crude Oil | 4.50% | |

| VIX | -1.91% |

The week of April 20–24, 2026, showcased a market grappling with technical resistance at all-time highs and shifting sentiment in the crypto and commodity spaces. While the tech-heavy QQQ led the charge, broader indices like the DIA showed signs of fatigue.

QQQ was the clear standout winner as growth regained its footing. DIA was the weak link, finishing the week down slightly, reflecting a rotation out of blue-chip value. IWM moved largely sideways, posting a modest gain.

GLD acted as a true hedge this week, rising 1.00% as geopolitical headlines drove a flight to safety and BTC/USD faced profit-taking to finish near the $86,200 level.

The 10-Year Yield continued its descent which provided the necessary oxygen for the Friday tech rally. The VIX remains compressed below 14, suggesting that despite the headlines, the "fear gauge" is not yet signaling a broad market panic.

Crude Oil saw the most dramatic move of the week, surging to close at $94.03 following supply concerns in the Middle East.

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | 2.12% | |

| FINANCIALS (XL) | 5.03% | |

| INDUSTRIALS (XLI) | -0.06% | |

| ENERGY XLE | 4.54% | |

| HEALTHCARE (XLV) | -2.88% | |

| UTILITIES (XLU) | -2.12% | |

| MATERIALS (XLB) | 4.65% | |

| REAL ESTATE (XLRE) | -0.30% | |

| CONSUMER STAPLES (XLP) | -0.81% | |

| CONSUMER DISCRETIONARY (XLY) | -2.22% |

The market experienced a sharp divide between "old economy" cyclical strength and defensive retreat. The sector story this week was one of distinct rotation. Growth-oriented sectors surged on late-week earnings optimism, while defensive and interest-rate-sensitive sectors faced significant pressure.

Financials (XLF) were the standout performers this week, surging over 5% as major banks continued to report robust earnings and improved net interest margins. Materials (XLB) and Energy (XLE) followed closely, buoyed by stabilizing commodity prices and the mid-week "war premium" in oil. Technology (XLK) regained its footing by Friday, finishing the week up 2.12% as investors front-ran next week's mega-cap tech earnings.

Health Care (XLV) took a significant hit, falling nearly 3% on disappointing guidance from several managed care providers. Consumer Discretionary (XLY) also struggled, dropping over 2% as specific heavyweights in the retail and automotive space weighed on the sector.

Interest-rate-sensitive sectors like Utilities (XLU) and Real Estate (XLRE) remained under pressure. Utilities, in particular, shed over 2% as the "higher for longer" narrative regarding interest rates kept investors cautious about high-dividend, capital-intensive plays.

Notable gainers for the week of Apr 20th–Apr 24th:

The market's "risk-on" appetite was on full display as the AI and semiconductor rally reached a fever pitch. While mega-cap tech provided the foundation, the standout performance came from the chip sector following a massive earnings-driven catalyst.

- Intel (INTC) surged 23% and was the undisputed star of the week. Shares skyrocketed after the company delivered an earnings report that shattered its "dot-com-era ceiling." The results showed a massive acceleration in its foundry business and a surprise surge in AI-PC chip demand, igniting a sector-wide rally in semiconductors.

- Mega Fortune Company (MGRT), the Hong Kong-based technology firm, continued its explosive April run, up another 21.4%. While much of the move is driven by momentum and high-frequency trading in the Asian markets, the stock has become a favorite for traders looking for high-volatility tech plays outside the U.S.

- Texas Instruments (TXN) popped 18.5%, riding the coattails of the chip boom. Analysts pointed to a significant rebound in industrial and automotive demand, coupled with strong data center performance, as key drivers for the renewed investor confidence.

- Bloom Energy (BE) popped nearly 13%, benefiting from the "energy for AI" theme. As tech giants scramble to secure power for new data centers, clean-energy solution providers like BE are increasingly seen as the essential infrastructure play for the AI decade.

- NVIDIA (NVDA) reclaimed its $5 trillion market cap in the final hours of Friday's trading by pushing up over 8.4% for the week. Despite its already massive valuation, investors piled back into the stock ahead of next month's anticipated pipeline updates.

Notable losers for the week of Apr 20th–Apr 24th:

While the tech heavyweights powered the indices to new heights, several prominent names in the communications and consumer sectors faced a harsh reality check this week. Earnings misses and shifting guidance weighed heavily on these laggards.

- Charter Communications (CHTR) tumbled nearly 24% and took the top spot for the worst performer after reporting a staggering loss of broadband subscribers. The "cord-cutting" narrative accelerated more than analysts anticipated, as investors re-evaluated the long-term growth prospects for traditional cable providers.

- Medpace Holdings (MEDP), the clinical research organization saw its stock price crater by over 21%. Despite a strong run earlier in the year, management's updated guidance suggested a significant slowdown in biotech funding and project starts, causing a massive de-risking event for the stock.

- Tractor Supply (TSCO) shares were hammered after the company warned that inflationary pressures are finally starting to curb spending among its core rural consumer base. The 18% drop reflects growing concerns that even "resilient" retail sectors are beginning to feel the macro-economic pinch.

- CRISPR Therapeutics (CRSP) fell nearly 16%. Despite groundbreaking advances in gene editing, the stock suffered from a "sell the news" reaction following a regulatory update. While no specific clinical failure was reported, investors appeared to rotate capital out of speculative pre-profit biotech and into the surging semiconductor sector.

- Comcast (CMCSA) fell nearly 13% with news that the company shed over 711,000 broadband subscribers over the last year, and the latest quarterly data confirmed that competitive pressure from 5G home internet providers continues to eat into its core market share.

Review selected market indices below:

Daily Notable Market Action

The week of April 20–24 was a roller coaster of record highs, geopolitical scares, and a spectacular semiconductor-led finish. While the threat of a widening conflict in the Middle East initially spooked investors, a landslide of positive earnings—particularly in the AI and chip sectors—ultimately carried the S&P 500 and Nasdaq to new highs.

Monday's Markets and News:

Markets took a breather from their historic rally as geopolitical tensions in the Middle East flared. Oil prices reclaimed the spotlight, with Brent crude topping $95 per barrel following reports of rising U.S.-Iran friction. The "risk-off" mood led to a slight retreat from all-time highs for the major indices, though the Russell 2000 bucked the trend to finish in the green.

- S&P 500: -0.2%

- Nasdaq: -0.3%

- Notable: The muted pullback suggested investors were still holding out hope for a diplomatic resolution to the Strait of Hormuz blockade.

Tuesday's Markets and News:

Volatility spiked as headlines regarding ceasefire talks flip-flopped throughout the day. Markets erased early gains of 400 points on the Dow after news surfaced that key negotiators had called off a high-level trip to Pakistan. On the economic front, Retail Sales surprised to the upside (+1.7%), marking the highest jump since early 2023, which briefly stoked "higher for longer" interest rate fears before the geopolitical headlines took over.

- S&P 500: -0.6%

- Dow Jones: -0.6%

- Notable: The 10-year yield rose as the strong retail data highlighted the resilience of the U.S. consumer despite inflationary pressures.

Wednesday's Markets and News:

Sentiment shifted back to "risk-on" after President Trump announced an indefinite extension of the U.S. ceasefire with Iran. This diplomatic reprieve allowed investors to pivot back to a heavy earnings slate. GE Vernova and Boston Scientific delivered blowout results, while Tesla (TSLA) reported a revenue miss but a surprise beat on free cash flow, sending its shares higher in the after-hours session.

- S&P 500: +0.8% (Record Close)

- Nasdaq: +1.3% (Record Close)

- Notable: The S&P 500 marked its 13th gain in 16 days, closing at a record 7,137.90.

Thursday's Markets and News:

The mid-week rally hit a speed bump as oil prices briefly spiked to $107 amid renewed uncertainty about the Strait of Hormuz. Markets pulled back from their record heights, with Tesla acting as a drag on the tech sector due to concerns over its aggressive capital expenditure on AI data centers. However, the mood shifted again after the bell when Intel (INTC) reported massive earnings, jumping 15% in late trading.

- S&P 500: -0.4%

- Nasdaq: -0.9%

- Notable: Despite the dip, the semiconductor index (SOX) extended its winning streak to 17 consecutive sessions.

Friday's Markets and News:

A "Chip-pocalypse" of gains defined the week's end. Intel surged over 23%, leading a broader semiconductor rally that saw AMD, ARM, and Qualcomm all post double-digit gains. Strong University of Michigan Consumer Sentiment data further boosted confidence, allowing the Nasdaq and S&P 500 to erase their Thursday losses and power to fresh all-time highs.

- Nasdaq: +1.63%

- S&P 500: +0.55%

- Notable: The Dow lagged behind (-0.16%) as high oil prices and a rotation out of cyclicals weighed on the blue-chip average.

Notable Earnings (Apr 27th–May 1st)

The true weight of the Q1 earnings season arrives in the final week of April. This upcoming stretch is the busiest and most critical period for the markets, featuring five of the "Magnificent Seven" tech giants alongside major players in energy, pharmaceuticals, and consumer staples. With nearly 40% of the S&P 500's total market capitalization reporting, these results will either validate the current record-high valuations or provide the catalyst for a cooling-off period. All eyes are on AI infrastructure spending and cloud growth as investors search for "proof of work" behind the recent tech rally.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, Apr 27th: VZ / PHG / CNQ

Tuesday, Apr 28st: KO / GM / SPOT / BKNG / MDLZ / HOOD / SBUX / V

Wednesday, Apr 29th: MSFT / AMZN / GOOGL / META / QCOM / ABBV / ADP / F

Thursday, Apr 30th: AAPL / LLY / CAT / MA / MRK / COP / AMGN / RIVN

Friday, May 1st: CVX / XOM / MRNA / EL / AON

Economic Calendar (April 27th – May 1st)

While earnings will dominate the headlines, the economic calendar for the final week of April is equally significant. The main event is the Federal Reserve's FOMC meeting, where the market expects interest rates to remain unchanged at 3.50%–3.75%. However, the focus will be entirely on Chairman Powell's tone and any hints regarding the timing of future cuts. An advance estimate for Q1 GDP will also be available, which could be an indicator of whether the economy's "hot start" to the year is sustainable.

The daily schedule of notable economic data releases is:

Monday: No major U.S. data scheduled.

Tuesday: U.S. Consumer Confidence (CB); S&P/Case-Shiller Home Price Index

Wednesday: FOMC Interest Rate Decision (2:00 PM ET); Fed Press Conference (2:30 PM ET); ADP Employment Report

Thursday: Advance Q1 GDP Data; Personal Consumption Expenditures (PCE); Initial Jobless Claims

Friday: ISM Manufacturing PMI; Construction Spending; University of Michigan Consumer Sentiment (Final)

Blue Sky Horizons

Last week, THE LITHIUM LOOP was explored in the circular economy of battery recycling. This week, a deeper look—literally—at the next frontier of firm, 24/7 carbon-free energy: The Geothermal Renaissance.

For decades, geothermal energy was the "neglected middle child" of renewables, restricted to specific geographic hotspots like Iceland or Northern California. However, a "blue sky" breakthrough is currently unfolding that could transform the Earth itself into a universal battery.

The transition that is apparent is the move from Traditional Geothermal (which requires finding rare natural underground steam vents) to Next-Gen Geothermal (which uses advanced drilling techniques to create radiators miles underground).

Data center energy demand is skyrocketing. Tech giants like Meta and Google are no longer just looking for intermittent wind and solar; they need "firm" power that never turns off. This month, next-gen leader Fervo Energy filed for its IPO and partnered with major industrial players to standardize "GeoBlocks"—modular, 50MW power plants that can be deployed almost anywhere there is hot rock.

Just as solid-state batteries aim to remove the volatile liquids from our cars, next-gen geothermal aims to remove the "geographical volatility" from our grid. Companies like XGS Energy are now using closed-loop systems to harvest heat without consuming water or requiring fracking, effectively turning the Earth's crust into a constant, reliable heat exchanger.

We are moving from an era of extracting fuel from the earth to an era of harvesting heat from it. The companies that bridge the gap between oil-and-gas drilling expertise and clean energy production are the ones that will likely define the "Blue Sky" winners of the late 2020s.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.