Higher for Longer or High-Tech for Now?

May 4, 2026

Market Roundup & The Week in Review

The final week of April 2026 was defined by a high-stakes "tug-of-war" between cooling macroeconomic data and a powerhouse technology sector that continues to decouple from broader market fears. While the "higher for longer" narrative remains a background hum – sustained by the Federal Reserve's hawkish hold on interest rates – the market was buoyed by a robust earnings season, particularly from AI-centric infrastructure plays.

Early in the week, sentiment was weighed down by a "forced realism" as investors balanced persistent inflation concerns against a slowing labor market. However, the narrative shifted toward aggressive optimism by Friday. The primary catalyst was the PCE inflation report, which came in softer than many feared at 3.5%, providing the necessary "oxygen" for a massive late-week rally in risk assets.

This surge was most visible in the semiconductor space, where sector leaders reclaimed significant valuation milestones (notably Nvidia retaking $5 trillion), signaling that the AI "proof of work" trade has more runway than the skeptics suggest. As investors closed the month, the market appeared to have transitioned from fearing an oil-driven inflation spike to embracing a tech-driven growth cycle, though the "narrowness" of this rally remains a point of caution for the weeks ahead.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

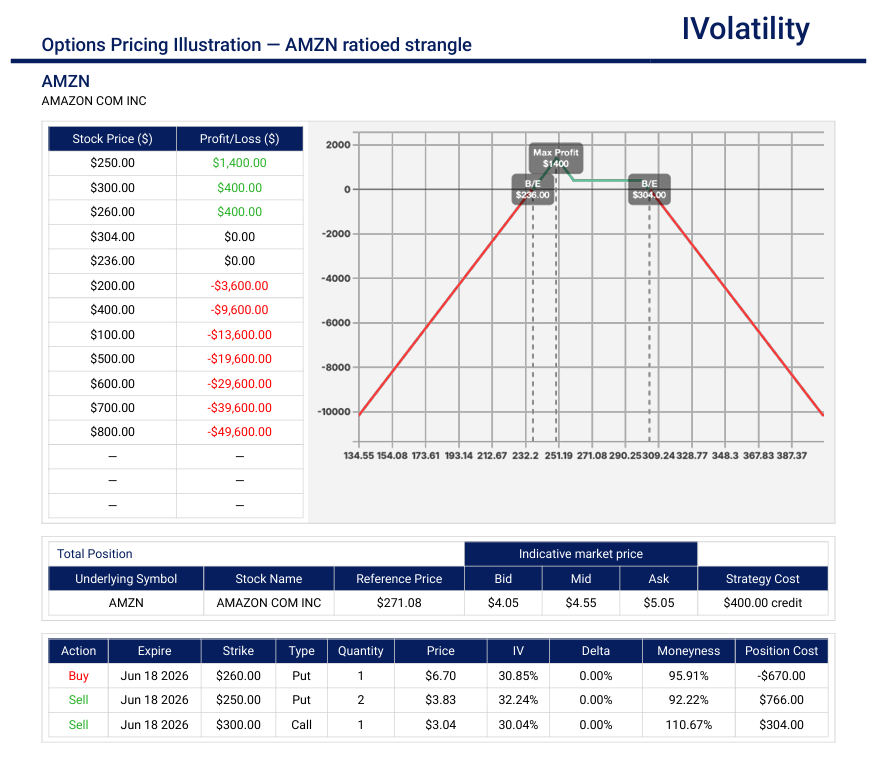

- AMZN (closed at 268.33 on Friday, May 1st)

Outlook: Following its recent earnings beat, AMZN showed significant relative strength during Friday's broad-market rally. While tailwinds are strong, the 45-day outlook could probably see a period of consolidation as the market digests these massive gains.

Strategy: Ratioed Strangle

In the June monthly expiration, buy one 260put / sell two 250puts / sell one 300call

Premium collected about $400

Net position delta is around 0 or essentially neutral

Probability of Profit about 73%

Maximum potential profit = $1400 (if AMZN pins at 250 at expiration)

Breakevens below 240 (16delta) and above 304 (12delta)

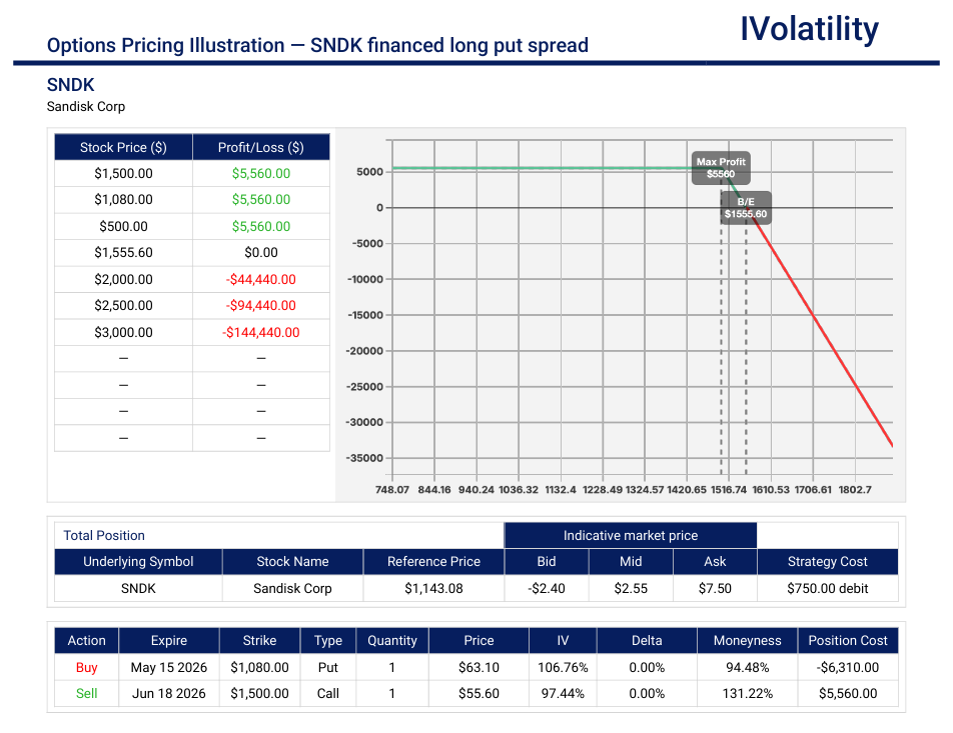

- SNDK (closed at 1188.15 on Friday, May 1st)

Outlook: SNDK has experienced an extraordinary run, recently hitting a record high near $1,195. Year-to-date, the stock is up significantly, and it has transitioned into a "high-beta" name that could be subject to some profit-taking.

Strategy: Financed long put spread

In the May monthly expiration, buy one ATM put spread (1100/1180)

Debit paid about $4000

In the June month expiration, sell a $1500 call

Credit collected about $6500

This short call finances the purchase of the long put spread

Net position delta about -44

No risk to the downside; upside breakeven around 1500

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | 0.78% | |

| QQQ | 0.91% | |

| IWM | 0.42% | |

| DIA | 0.67% | |

| GLD | 1.12% | |

| BTC/USD | 2.34% | |

| 10-year yield | -0.86% | |

| Crude Oil | -1.15% | |

| VIX | -3.10% |

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | 1.38% | |

| FINANCIALS (XL) | 0.45% | |

| INDUSTRIALS (XLI) | 0.32% | |

| ENERGY XLE | -1.15% | |

| HEALTHCARE (XLV) | 0.58% | |

| UTILITIES (XLU) | 0.82% | |

| MATERIALS (XLB) | 0.12% | |

| REAL ESTATE (XLRE) | 0.74% | |

| CONSUMER STAPLES (XLP) | 0.51% | |

| CONSUMER DISCRETIONARY (XLY) | 0.22% |

Notable gainers for the week of Apr 27th–May 1st:

While the broad indices managed to claw back territory late in the week, several specific names significantly outpaced the market. These gainers represent a shift in investor confidence toward companies that can prove "AI profitability" or demonstrate resilience in a high-rate environment. The late-week relief in Treasury yields provided the necessary backdrop for these leaders to extend their moves.

- Atlassian (TEAM) popped over 5% following quarterly reports that highlighted a massive surge in enterprise adoption for its AI-integrated software tools.

- Nvidia (NVDA) bumped up 3.4% and reclaimed a $5 trillion valuation milestone as global demand for sovereign AI infrastructure appeared to be reaching a new fever pitch.

- Intel (INTC) rose 2.8%, benefitting from a rotation back into domestic chip manufacturing as investors speculated that localized supply chains might be the primary winners of the next decade.

- Domino's Pizza (DPZ) popped over 2% and outperformed after reporting surprisingly strong order counts, suggesting the consumer remains more resilient than macro data implies.

- Alphabet (GOOGL) rose nearly 2% seeing continued strength as markets reacted to the integration of generative search features, which can be credited for stabilizing its long-term advertising moat.

Notable losers for the week of Apr 27th–May 1st:

Conversely, the week's laggards were largely defined by cautious forward-looking guidance. Companies tied to traditional discretionary spending or those facing specific commodity headwinds found it difficult to participate in the Friday rally. This divergence might suggest that the market is becoming increasingly selective, rewarding growth while punishing anything that hints at a "consumer slowdown."

- Tractor Supply (TSCO) dropped 4.1% and faced heavy selling pressure following a cautious spending outlook, signaling that the rural consumer could finally be feeling the pinch of sustained inflation.

- Exxon Mobil (XOM) slid 2.3%, dragged down by the broader pullback in the energy sector as crude oil prices softened throughout the week.

- Tesla (TSLA) shed 1.8% and remained under pressure as concerns over global EV demand and pricing competition weighed on investor sentiment despite the broader tech rally.

- Chevron (CVX) lost 1.5%. Similar to its peers in the Energy Sector, it struggled as the "inflation hedge" trade took a back seat to the technology-driven growth narrative.

- Meta Platforms (META) lost 1.2% and underperformed relative to its Big Tech peers as investors paused to digest the massive capital expenditure requirements for its future infrastructure projects.

Review selected market indices below:

Monday's Markets and News:

Markets opened the week on a positive note as the S&P 500 reached its ninth all-time closing high of the year. Sentiment was bolstered by a massive 24% surge in Intel following strong earnings, which ignited a broad-based rally in the semiconductor space. Despite ongoing geopolitical tensions keeping oil prices elevated, the focus remained on the heavy "Mag-7" earnings calendar ahead.

- SPY: +0.12%

- QQQ: +0.08%

Tuesday's Markets and News:

The rally hit a speed bump as tech-heavy indices pulled back from record levels. The Nasdaq led losses with a 1.2% drop as doubts regarding OpenAI's internal targets weighed on AI-linked software stocks. Inflation fears were also renewed as crude oil prices pushed back above $100 per barrel while the Strait of Hormuz remained closed, causing Treasury yields to climb as the Fed's two-day meeting began.

- SPY: -0.21%

- QQQ: -0.34%

Wednesday's Markets and News:

Trading was largely muted and characterized by "watchful waiting" as investors digested the Federal Reserve's decision to leave interest rates unchanged. While the S&P 500 and Nasdaq were nearly flat, the real movement occurred after the bell; a flurry of earnings from Alphabet and Amazon beat expectations and surged in late trading, while Meta and Microsoft tumbled due to concerns over high capital expenditure in the AI race.

- SPY: +0.05%

- QQQ: +0.11%

Thursday's Markets and News:

Markets surged as the Dow gained over 790 points, powered almost single-handedly by a 10% jump in Caterpillar following robust earnings. The S&P 500 and Nasdaq were buoyed by a 10% spike in Alphabet, which reassured investors that its massive AI investments were yielding significant cloud revenue growth. This cyclical rotation helped the Dow outpace tech as investors sought value outside of the overextended AI software names.

- SPY: +0.82%

- QQQ: +1.14%

Friday's Markets and News:

The week closed with the S&P 500 and Nasdaq reaching fresh record highs, driven by a 3.3% rise in Apple after a significant earnings beat and upbeat guidance. Sentiment was further supported by a mild retreat in oil prices and a softer-than-feared PCE inflation print. While the Dow slipped slightly as value stocks took a backseat, the broader market celebrated a "Goldilocks" scenario of strong earnings and stabilizing inflation data.

- SPY: +1.02%

- QQQ: +1.45%

Notable Earnings (May 4th – May 8th)

The focus for next week's earnings will probably shift from hardware infrastructure to the health of the digital economy and consumer software. With reports from Palantir (PLTR), Shopify (SHOP), and Arm Holdings (ARM), the market could get a clearer picture of how AI integration is translating into actual revenue growth beyond just the chipmakers. Additionally, the results from Disney (DIS) and Uber (UBER) could serve as a critical litmus test for the resilience of discretionary spending in this "higher for longer" interest rate environment.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, May 4th: PLTR / TSN / PLD

Tuesday, May 5th: DIS / FERR / BP / UBS

Wednesday, May 6th: SHOP / ARM / UBER / RIVN

Thursday, May 7th: ABNB / DASH / MSTR / UNITY

Friday, May 8th: ENB / TELUS / AMC

Economic Calendar (May 4th – May 8th)

While the market continues to digest the "higher for longer" stance from the Fed, the upcoming week shifts the spotlight to the strength of the American labor market. The primary event is Friday's Non-Farm Payrolls report, which could serve as a definitive signal for whether the economy is cooling enough to warrant a potential pivot later this year. Additionally, several Federal Reserve officials are scheduled to speak throughout the week, and their commentary might probably provide further clarity on the central bank's tolerance for current inflation levels.

The daily schedule of notable economic data releases is:

Monday, May 4th: No major U.S. economic data scheduled.

Tuesday, May 5th: ISM Services PMI / JOLTS Job Openings.

Wednesday, May 6th: ADP Employment Report / EIA Crude Oil Inventories.

Thursday, May 7th: Initial Jobless Claims / Productivity and Costs (Q1).

Friday, May 8th: Non-Farm Payrolls / Unemployment Rate / Average Hourly Earnings.

Blue Sky Horizons

The current market cycle has been dominated by the frantic build-out of centralized data centers, but the next phase could probably be defined by the rise of Sovereign AI. We are beginning to see a shift where nations are no longer content to rely solely on external technology providers; instead, they are investing in localized computing power to ensure data privacy and national security. This trend might provide a second wind for infrastructure and cybersecurity stocks as global governments race to secure their own digital borders.

While hardware remains the foundational layer, the "blue sky" potential lies in how these sovereign networks could lead to a fragmented but highly specialized AI ecosystem. This shift might probably create unique opportunities for investors to move beyond the usual mega-cap tech names and find value in companies that facilitate localized, secure implementation of large language models. As we look toward the horizon, the transition from "AI for everyone" to "AI for us" could be the primary narrative that sustains market momentum into the latter half of the year.

The rise of Sovereign AI has already moved beyond theory, with several major tech players positioning themselves as the primary "architects" for nations looking to build their own digital walls. These companies are shifting their focus from selling general-purpose cloud space to providing the specific hardware and software stacks required for national autonomy.

Here are a few companies that could probably be the leaders in this emerging landscape:

- Nvidia (NVDA): As the primary provider of the H100 and Blackwell chips, Nvidia is essentially the "foundry" for Sovereign AI. They are actively partnering with governments in regions like Singapore, Japan, and France to build national AI clouds.

- Oracle (ORCL): Oracle has carved out a niche in "Sovereign Cloud" regions, specifically designed to meet the strict data residency and security requirements of the European Union and individual governments.

- Arm Holdings (ARM): Since sovereign networks often require highly specialized, energy-efficient chips, Arm’s architecture might become the standard for nations wanting to design their own domestic silicon.

- Palantir (PLTR): With its deep roots in government and defense, Palantir provides the "operating system" that allows nations to integrate AI into their specific sovereign data sets while maintaining strict security protocols.

- Alphabet (GOOGL): Through Google Cloud's "Air-Gapped" and sovereign solutions, they are enabling public sector entities to use AI tools without their data ever leaving the country's physical borders.

This trend might probably lead to a more fragmented market where these "Sovereign Service Providers" see sustained growth as nations prioritize digital self-reliance over centralized efficiency.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.