A Fractured Market

May 18, 2026

Market Roundup & The Week in Review

The trading week ending May 15th exposed a stark and broadening divergence across the capital markets. While headline indices gave the illusion of a quiet, consolidated tape—headlined by the Dow Jones Industrial Average crossing the historic 50,000 milestone for the first time ever on Thursday—a look under the hood revealed severe structural fragmentation. Mega-cap equities and select blue-chips successfully acted as a defensive shield for the major benchmarks, but smaller, rate-sensitive companies, alternative stores of value, and fixed-income assets felt the full weight of a punishing macro shift.

The primary catalyst for this fracture arrived early Tuesday morning with a scorching April Consumer Price Index (CPI) report. Headline inflation accelerated sharply to 3.8% year-over-year, marking its highest level since mid-2023, driven by a 17.9% spike in energy costs stemming from ongoing geopolitical conflict. Crucially for the Federal Reserve's path, monthly core CPI jumped by 0.4%, proving that sticky price pressures are aggressively bleeding into the broader service economy.

This hot data triggered an immediate repricing in the bond market. The 10-Year Treasury Yield surged by 17 basis points on the week to finish at 4.59%, throwing cold water on near-term rate cut expectations and prompting a sharp capital flight from areas reliant on easy financing conditions. This dual pressure cooker of accelerating inflation and a renewed energy shock forced an aggressive defensive rebalancing—lifting Consumer Staples (XLP) and Financials (XLF) while severely depressing long-duration, highly leveraged plays like Real Estate (XLRE, -3.10%) and small-caps (IWM, -2.57%).

The hotter-than-expected inflation print caught a heavily leveraged market off guard, immediately halting the broader market's momentum and sparking a rapid intraday rotation away from risk-sensitive assets.

Despite the underlying inflation rot, an explosive corporate earnings report from Cisco Systems and a massive wave of enterprise spending on AI infrastructure propelled the Dow Jones Industrial Average to a historic, first-time close of 50,063.46 on Thursday.

The celebration was short-lived though. On Friday, the reality of a global bond market selloff and WTI Crude oil cementing its position above $102 forced a sharp 1.1% retreat in the blue-chip index, pulling the Dow right back under the milestone to finish the week at 49,526.17.

Cash-rich, defensive mega-caps absorbed the shock waves of the hot inflation data, keeping the primary capitalization-weighted benchmarks anchored remarkably close to unchanged over the five-day stretch.

While the heavyweights hid the damage, small-caps bore the brunt of the pain. The reality of a "higher-for-longer" Fed policy environment directly threatened the Russell 2000, signaling that the broader corporate landscape is far more fragile than headline index records suggest.

Non-yielding and speculative assets suffered aggressively under the competitive pressure of higher nominal rates. Gold fell significantly to close at $417.29, while Bitcoin broke down below its key $80,000 baseline to finish the week at $79,105.75 as macro liquidity constricted.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

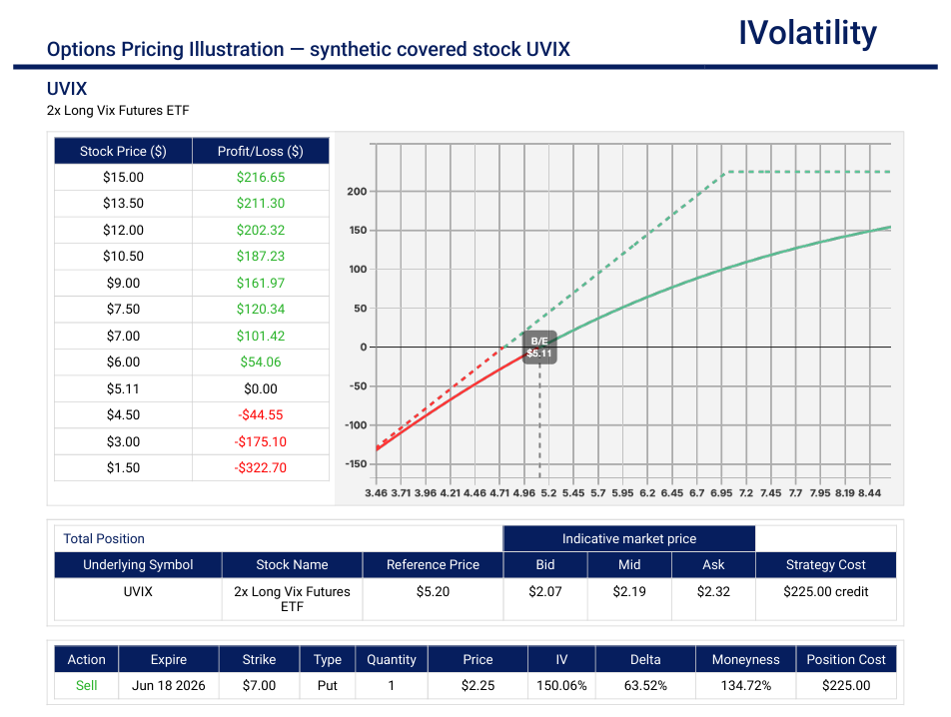

UVIX (closed at 5.17 on Friday, May 15th)

Outlook: with markets so high and volatility at record lows, this UL is 2 times the long VIX futures. A market correction and subsequent increase in the VIX should be beneficial for this strategy.

Strategy: Synthetic covered stock

In the June monthly expiration, sell the ITM 7 put. This is synthetically the same as buying the stock and selling the 7 call

Premium collected about $225

Net position delta is around +66

Maximum potential profit = $225

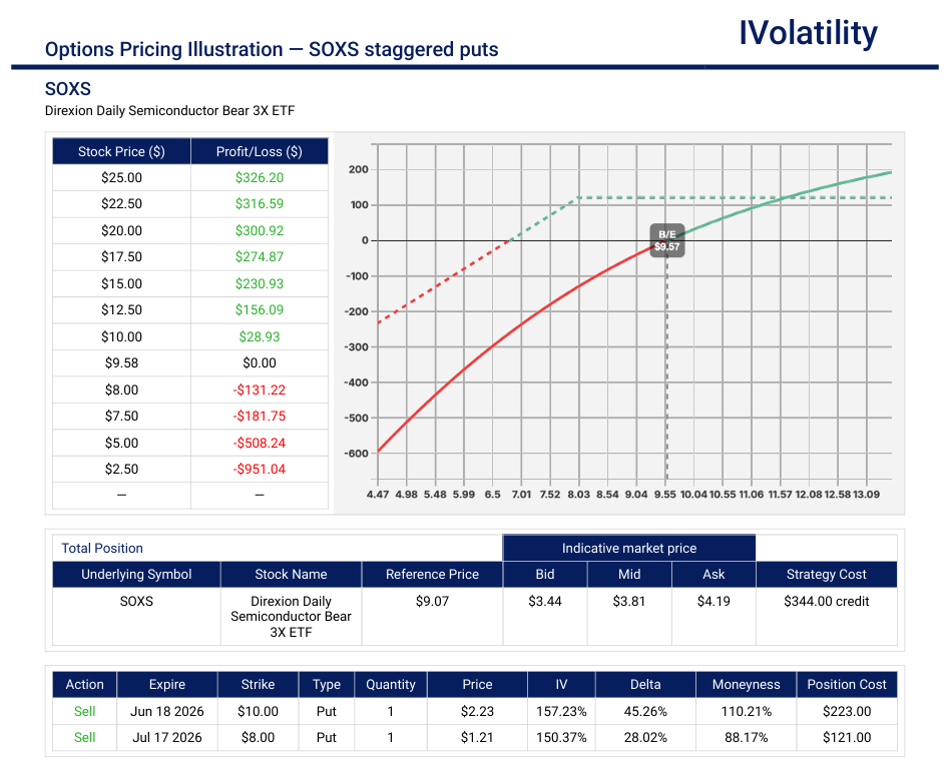

SOXS (closed at 9.25 on Friday, May 15th)

Outlook: This UL represents a highly leveraged bet against the semiconductor (chip) sector. This sector has experienced an outsize move to the upside and this strategy is getting short the sector using SOXS

Strategy: staggered short puts

In the June monthly expiration, sell the 10put and in the July expiration sell the 8put

Debit paid about $380

Net position delta about +75 (bullish here = bearish the semis)

No risk to the upside; downside risk just above 7

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | 0.37% | |

| QQQ | -0.20% | |

| IWM | -2.57% | |

| DIA | -0.09% | |

| GLD | -3.89% | |

| BTC/USD | -2.96% | |

| 10-year yield | 0.17% | |

| Crude Oil | 3.96% | |

| VIX | 1.99% |

The major equity ETFs experienced a clear risk-off divergence this week, as large-caps remained relatively flat while small-caps (IWM) collapsed by over 2.50% under the weight of surging interest rates. Across the broader macro landscape, a multi-decade breakout in the 10-year Treasury yield and a geopolitical spike in Crude Oil above $100 heavily pressured alternative assets, dragging down both Gold (GLD) and Bitcoin (BTC/USD) by roughly 3% to 4%.

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | -0.43% | |

| FINANCIALS (XL) | 1.04% | |

| INDUSTRIALS (XLI) | -0.79% | |

| ENERGY XLE | 3.94% | |

| HEALTHCARE (XLV) | -0.35% | |

| UTILITIES (XLU) | -1.78% | |

| MATERIALS (XLB) | -1.54% | |

| REAL ESTATE (XLRE) | -3.10% | |

| CONSUMER STAPLES (XLP) | 0.60% | |

| CONSUMER DISCRETIONARY (XLY) | -0.95% |

The defensive rotation was a mixed bag this week—Staples (XLP) managed a slight gain, but rate-sensitive Real Estate (XLRE) and Utilities (XLU) caught the worst of it, likely weighed down by that 17-basis-point surge we saw in the 10-year yield.

Notable gainers for the week of May 11th – May 15th

This list highlights the specific corporate catalysts that fueled the market's record-breaking moments before the Friday macro pullback:

- Cisco Systems (CSCO) finished the week up nearly 30% over a 5-day winning streak to hit an all-time high of $119.36. The company delivered a massive fiscal Q3 "beat-and-raise" blowout report. Driven by an explosive surge in Big Tech AI data center spending, management revealed that hyperscaler product orders jumped by a triple-digit percentage, prompting them to raise their full-year guidance by a massive $1 billion. This single-handedly propelled the Dow over 50,000 on Thursday.

- Rocket Lab USA (RKLB) shot up over 58%. The aerospace momentum stock extended its massive monthly run following a spectacular quarterly earnings report, key new defense contract wins, and intense retail/institutional space-sector hype ahead of the upcoming SpaceX IPO.

- Arista Networks (ANET) finished the week up over 7.2% after catching a massive sympathetic institutional bid directly following Cisco's earnings results. The triple-digit growth in enterprise networking orders confirmed to the Street that the broader data center infrastructure buildout still has immense fundamental momentum.

- Bitcoin Mining Equities (RIOT / MARA / CLSK) were each up 11%, 8% and 9%. While spot Bitcoin (BTC/USD) suffered later in the week under the weight of the 10-year yield, mining equities decoupled aggressively early on. Wall Street heavily rewarded companies transitioning their infrastructure into high-performance computing (HPC) and AI hosting cloud services, highlighted by institutional filings showing massive Q1 position increases from entities like Abu Dhabi's sovereign wealth fund (Mubadala).

Notable losers for the week of May 11th – May 15th

This selection highlights how rising yield pressure, growth-deceleration fears, and corporate restructurings drove heavy selling across multiple sectors.

- Boeing (BA) dropped over 7% after the aerospace giant faced renewed structural selling as lingering supply chain delays and regulatory scrutiny over production caps continued to bottleneck their commercial delivery schedule. Investors aggressively rotated out of capital-heavy industries as borrowing costs hit new multi-month highs.

- Home Depot (HD) dropped over 6% as housing market bellwethers took a direct hit from Tuesday’s hot CPI print and the subsequent surge in the 10-year Treasury yield to 4.59%. Wall Street quickly priced in a tighter, "higher-for-longer" mortgage rate environment, which severely dampens near-term expectations for home improvement and broader residential construction spending.

- Wix.com (WIX) collapsed nearly 32% marking one of the sharpest software cap capitulations on the tape. The web development platform plummeted following a combination of soft forward-looking guidance and growing market anxieties surrounding direct AI disruption to its core product line, prompting heavy institutional distribution.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

Monday set a cautious but resilient tone for the week. While the "Physical AI" narrative (chips and power) continued to drive record highs, the shadow of geopolitical tension and energy costs kept the Dow essentially flat.

The market opened the week with a "tug-of-war" dynamic. While the S&P 500 and Nasdaq edged higher to fresh record territory, the Dow struggled to find footing as surging oil prices acted as a lead weight on the broader economy.

Semiconductor and memory leaders (NVDA, INTC, MU) continued their relentless march upward. Analysts are increasingly discussing a "sector supercycle" driven by AI memory demand. Qualcomm (QCOM) also surged following a significant analyst upgrade.

WTI Crude oil jumped nearly 4%, approaching the $99/barrel mark. Fears are mounting as hopes for a swift reopening of the Strait of Hormuz fade, directly pressuring airlines and reigniting fears that inflation may remain "sticky" for longer.

Stalled peace talks and escalating tensions in the Middle East weighed on sentiment early in the day, though the "tech-as-a-safe-haven" trade seemed to absorb much of the shock.

- S&P 500: +0.19% to 7,412.94 (New Record)

- Nasdaq Composite: +0.10% to 26,274.13 (New Record)

- Dow Jones: +0.19% to 49,704.47

Tuesday's Markets and News:

Tuesday was dominated by the highly anticipated CPI data, which served as a major reality check for the "soft landing" narrative. The reaction in the bond market immediately rippled through the equities sectors, particularly those sensitive to interest rates.

The narrative shifted from growth momentum to inflation persistence following the release of the April Consumer Price Index. The data came in "hotter" than the consensus estimate, sparking an immediate repricing of Fed rate-cut expectations for the remainder of 2026.

The headline CPI rose 0.4% for the month, keeping the annual rate stubbornly above the Fed’s target. The "sticky" nature of shelter and services costs took center stage, cooling the recent rally.

The 10-year Treasury yield spiked above 4.5%, its highest level in months. This move put immediate pressure on high-growth tech and the Real Estate (XLRE) sector, as the "higher-for-longer" mantra returned to the forefront of the conversation.

Despite the broader market sell-off, Energy (XLE) remained a relative bright spot as oil prices held their gains near $98-$99/barrel.

- S&P 500: -0.46% to 7,378.85

- Nasdaq Composite: -0.32% to 26,190.11

Wednesday's Markets and News:

Following Tuesday's "hot" inflation shock, the market spent Wednesday searching for a base, while Thursday saw a massive resurgence driven by a high-stakes diplomatic summit and fresh "Physical AI" momentum.

The narrative of "sticky" inflation was reinforced Wednesday by the Producer Price Index (PPI), which mirrored Tuesday's consumer data by coming in higher than expected. However, the equity markets showed signs of digestion, with a tech rebound helping to offset the drag from the Dow.

Wholesale inflation accelerated more sharply than anticipated in April. This confirmed that price pressures are originating at the supply level, complicating the Fed's path toward rate normalization.

Despite the macro headwinds, Nvidia (NVDA) and Micron (MU) rallied. Investors pivoted back to high-margin AI names as a "quality" hedge. News that CEO Jensen Huang would join the U.S. presidential delegation to China began to circulate, sparking trade-related optimism.

Treasury yields remained elevated near 4.47%, keeping the cap on Small Caps (IWM) and Real Estate (XLRE).

- S&P 500: +0.58% to 7,444.25 (New Record Close)

- Nasdaq Composite: +0.20% to 26,242.15

Thursday's Markets and News:

The market largely ignored the inflation data from earlier in the week, fueled instead by positive developments from the U.S.-China summit in Beijing and a major restructuring "beat" from a networking giant. Thursday's action was a textbook "Risk-On" reversal. The VIX cooled to its weekly low (around 17.7), and the Dow finally broke through the psychological 50,000 barrier.

Sentiment exploded after reports surfaced that the U.S. cleared several Chinese firms to purchase Nvidia's H200 AI chips. NVDA surged nearly 4%, pushing its market valuation toward $5.6 trillion.

Cisco (CSCO) jumped over 10% after announcing a restructuring plan and raising its revenue forecast. Their AI infrastructure order book growing from $5B to $9B provided tangible proof of the "Physical AI" supercycle we've been tracking.

The AI hardware upstart Cerebras (CBRS) made its market debut, with shares doubling intraday before closing up 68%. This added fresh fuel to the semiconductor "arms race" narrative.

April retail sales showed a 4.87% year-over-year jump, proving that despite inflation, the American consumer remains an active engine of growth.

- S&P 500: +0.77% to 7,501.24 (18th Record Close of the Year)

- Nasdaq Composite: +0.88% to 26,473.10 (New Record)

Friday's Markets and News:

The equity market faced a sharp reality check as macroeconomic pressures intensified, triggering a broad-based afternoon selloff. A global bond market rout drove the 10-Year Treasury Yield to a striking 4.59%, while geopolitical supply concerns cemented WTI Crude oil's positioning firmly above $102 a barrel. This toxic combination of accelerating borrowing costs and renewed energy shock waves completely stalled the market's momentum, completely wiping out Thursday's optimism and forcing a sharp 1.1% drop in the Dow Jones Industrial Average to pull it back below the historic 50,000 threshold.

The defensive rotation on the floor became highly pronounced as the closing bell approached. Rate-sensitive sectors like Real Estate and Utilities capitulated to the highest yields seen since early last year, while traditional inflation hedges like Energy caught a late-session bid. Meanwhile, cash-rich mega-cap technology leaders experienced targeted institutional distribution, signaling that even the market's most resilient shields are showing vulnerability under a "higher-for-longer" monetary backdrop.

- S&P 500: -1.24% to 7,408.50 (Pulling back from Thursday's records)

- Nasdaq Composite: -1.54% to 26,225.14

Notable Earnings (May 18th – May 22nd)

This is a massive week for the retail and tech sectors, with heavy hitters like HD, WMT, and the big one—NVDA—reporting. The "Wednesday Night Lights" with NVDA will probably be the primary catalyst for the entire semi-conductor space and the broader tech sector. Given the 3.8% CPI announced this week, the market could be looking at WMT and TGT numbers very closely to gauge if the consumer is finally starting to buckle under inflationary pressure.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, May 18th: BIDU

Tuesday, May 19th: HD

Wednesday, May 20th: NVDA / TGT / ADI / CSCO

Thursday, May 21st: WMT / DE / INTU / TTWO

Friday, May 22nd: no noteworthy announcements scheduled

Economic Calendar (May 18th – May 22nd)

This week is particularly data-heavy regarding the housing market and consumer sentiment, which should provide a significant backdrop to the retail earnings from WMT and TGT. High volatility is a potential occurrence as the market looks for clues on the Fed's reaction to the recent 3.8% CPI print.

The release of the FOMC Minutes on Wednesday afternoon could create a "collision course" with the NVDA earnings report scheduled for that same evening. If the minutes suggest a more hawkish tone due to persistent inflation, the market probably sees some defensive posturing in XLK and XLY before the big tech numbers hit.

- Monday, May 18th:

Empire State Manufacturing Index

NAHB Housing Market Index - Tuesday, May 19th:

Building Permits & Housing Starts - Wednesday, May 20th:

FOMC Meeting Minutes - Thursday, May 21st:

Initial Jobless Claims (8:30 AM)

Philadelphia Fed Manufacturing Index (8:30 AM)

Existing Home Sales - Friday, May 22nd:

U. of Michigan Consumer Sentiment - Final

Blue Sky Horizons

For the past year, the market has been obsessed with the "brains" of AI—the large language models and the GPUs that train them. But this week, the narrative shifted toward the "body"—the physical infrastructure required to move, power, and house that intelligence. We are entering the era of Physical AI.

The "software-only" phase of AI is maturing. The next leap forward isn't just about better chatbots; it's about intelligence embedded in the physical world—smart power grids, autonomous logistics, and massive-scale networking. Thursday's market action provided two "smoking guns" for this supercycle:

- The Networking Surge: Cisco (CSCO) shocked the Street by revealing its AI infrastructure order book nearly doubled—jumping from $5 billion to $9 billion. This tells us that enterprise companies are no longer just "testing" AI; they are rebuilding their physical nervous systems to support it.

- The Hardware Frontier: The blockbuster IPO of Cerebras (CBRS)—the largest tech listing since 2023—proves there is an insatiable institutional appetite for hardware that solves the "power and speed" bottlenecks of traditional chips.

Traders often look for the "pick and shovel" plays. But Physical AI is a capital expenditure supercycle that mirrors the industrial scale of the 1950s highway build-out.

While the "Magnificent 7" get the headlines, the real alpha may be migrating toward the Industrials (XLI) and Utilities (XLU) sectors that provide the power and the "physicality" AI needs to function.

While 2024 and 2025 was spent marveling at large language models (LLMs), 2026 is becoming the year that AI grows "hands." We are moving from the digital workflow into Physical AI—where agentic software meets humanoid robotics and autonomous systems at scale.

The transition from experimentation to execution is triggering a "Dual Mandate" for the XLU (Utilities) and XLI (Industrials) sectors. Data centers are no longer just tech assets; they are becoming strategic national infrastructure.

Global electricity demand is accelerating at its fastest pace in decades. This could lead to a decade-long re-rating of companies that provide grid stability and energy modularity (SMRs and advanced LNG).

Beyond the atmosphere, the space economy is projected to hit nearly $470 billion this year. With reusable rocket cadence reaching "routine" status, the future appears to be where orbital manufacturing and satellite-based broadband aren't just concepts—they are becoming line items in diversified portfolios.

Long-term investors may want to look past the weekly "noise" of CPI prints and FOMC minutes to see the secular shift. The convergence of AI, energy needs, and space-based utility is creating asymmetric opportunities that most traditional investors are still pricing as "alternative."

"The horizon is only the limit of our sight. For the sophisticated trader, the horizon is where the next structure begins."

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.