The AI Airpocket: Spiking Yields Trigger a Violent Growth Reset

By Fauzia Timberlake,

professional options trading coach

June 8, 2026

Market Roundup & The Week in Review

The first week of June 2026 delivered a harsh reality check to the capital markets, culminating in a violent, macro-driven growth shakeout on Friday that fractured weeks of steady momentum. For months, equity markets have operated under a goldilocks assumption that cooling economic indicators would smoothly pave the way for Federal Reserve interest rate cuts. That narrative was shattered on Friday morning, forcing an aggressive structural repricing across all major asset classes.

The primary epicenter of the week's volatility was the May nonfarm payrolls report released on Friday, June 5th. The Bureau of Labor Statistics reported that the U.S. economy added 172,000 new jobs last month—roughly doubling Wall Street's consensus expectations of 88,000. Additionally, the previous two months of payroll data were revised higher by a combined 93,000 jobs. This report completely shifted the narrative. The numbers virtually erased hopes for near-term interest rate cuts. For growth tech, software, and highly leveraged consumer cyclicals, the prospect of "higher-for-longer" interest rates triggered an immediate, systematic exit.

While a resilient labor market points to robust underlying economic health, the bond market interpreted the blowout data through a singular lens: the Fed's inflation fight is far from over. Fixed-income assets experienced immediate, sharp selling pressure, sending the benchmark 10-year Treasury yield surging to 4.55%. Interest rate futures markets immediately adjusted, with odds increasing for a full 25-basis point Fed rate hike later this year rather than the long-anticipated cuts.

The macro yield shock collided directly with a growing sense of valuation exhaustion in the high-flying semiconductor sector. The PHLX Semiconductor Index (SOX) plummeted 8.5% on Friday alone, stripping more than $1 trillion in market value from the AI trade in a single session.

Despite the deep index-level point drops, the underlying market mechanics revealed a highly calculated internal sector rotation rather than blind, systemic panic. As capital fled long-duration growth and expensive tech multiples, it trickled straight into traditional, cash-flowing value, energy, and defensive spaces such as Healthcare and Hospitality Reits.

Outside of equities, speculative risk assets felt the immediate weight of higher risk-free yields, with the cryptocurrency complex sliding sharply as Bitcoin futures broke below the critical $60,000 psychological floor.

By Friday's closing bell, the tech-heavy benchmarks had borne the absolute brunt of a systematic risk-off liquidation, snapping the S&P 500's impressive nine-week winning streak.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

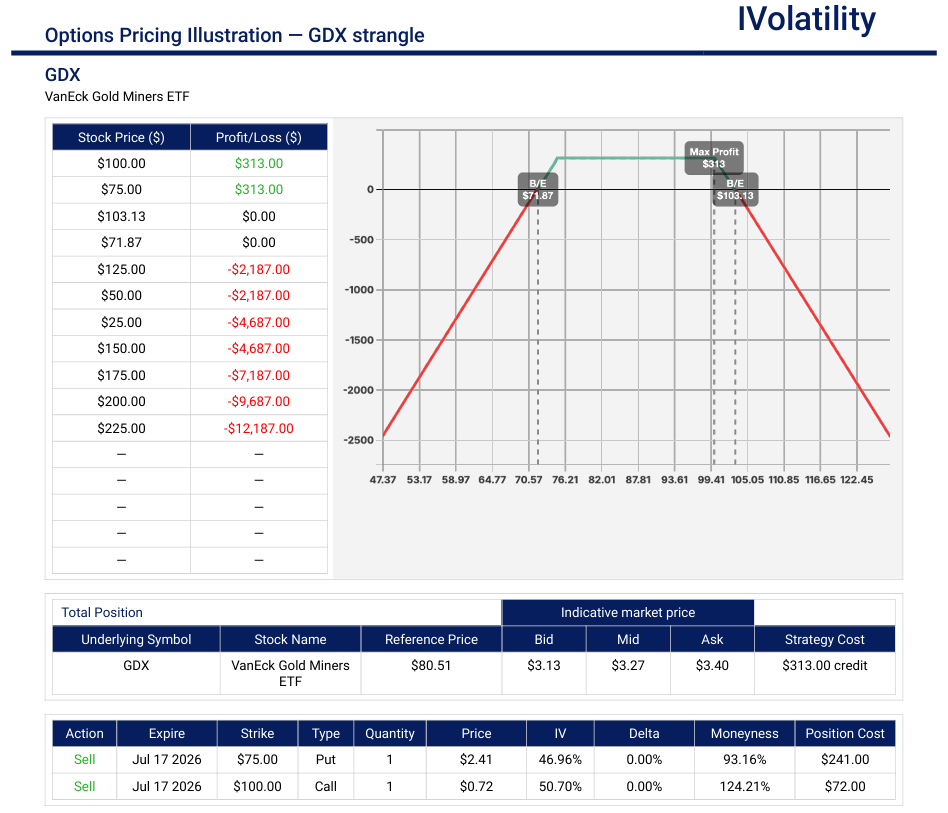

GDX (closed at 78.91 on Friday, June 5th)

Outlook: neutral, leaning bullish

This strategy could be a highly viable tactical approach. While Friday's blowout nonfarm payrolls report hammered the complex—sending spot gold down to the $4,320–$4,500 range and dropping GDX back to around $79–$84—this sharp flush has cleared out near-term speculative froth and re-established a highly compelling structural and technical foundation for premium sellers and buyers alike.

Strategy: Strangle

In the July monthly expiration, sell the 75/100 strangle

Premium collected: about $360/contract

Net Position Delta around +24

Breakevens around 72 and 103

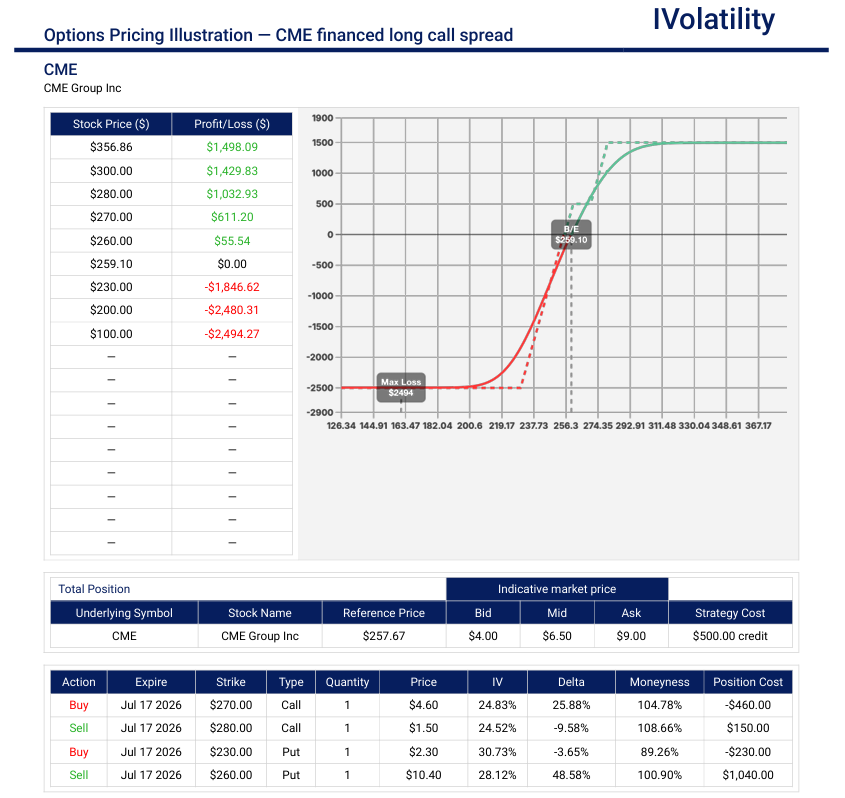

CME (closed at 257.47 on Friday, June 5th)

Outlook: bullish

CME Group is the ultimate "volatility house." While rising macroeconomic uncertainty, swinging interest rate expectations, and a sharp growth equity sell-off terrify traditional long-only stock managers, they act as high-octane fuel for CME's transaction-fee engine. The stock appears primed for an upward re-rating based on several immediate fundamental and volume-driven catalysts:

Strategy: Financed Long Call Spread

Buy the July 270/280 long call spread

Completely finance this purchase with the sale of the July 230/260 put spread

Premium collected: about $500/contract

Net position delta about +52

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | -2.36% | |

| QQQ | -4.95% | |

| IWM | -2.33% | |

| DIA | -0.03% | |

| GLD | -3.32% | |

| BTC/USD | -18% | |

| 10-year yield | 1.55% | |

| Crude Oil | 0.30% | |

| VIX | 40.40% |

The notable takeaway is that the Dow (DIA) was essentially flat, while tech (QQQ) absorbed most of the damage, and the VIX spike above 40% reflects a sharp increase in market fear by week's end.

The striking feature of the week was that stocks fell, gold fell, and Bitcoin fell sharply at the same time while Treasury yields rose, which is characteristic of a broad deleveraging/risk-off move rather than a traditional flight-to-safety environment.

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | -6.25% | |

| FINANCIALS (XL) | 2.09% | |

| INDUSTRIALS (XLI) | -1.5% | |

| ENERGY XLE | 2.45% | |

| HEALTHCARE (XLV) | 3.02% | - |

| UTILITIES (XLU) | 1.03% | |

| MATERIALS (XLB) | -1.5% | |

| REAL ESTATE (XLRE) | 2.24% | |

| CONSUMER STAPLES (XLP) | 1.13% | |

| CONSUMER DISCRETIONARY (XLY) | -4.04% |

The standout theme for the week was a strong rotation into defensive sectors (Healthcare, Utilities, Staples, Real Estate) while Technology and Consumer Discretionary were hit hardest.

Notable gainers for the week of June 1st – June 5th

Despite the heavy index-level losses at the end of the week, there were still notable pockets of strength. The primary gainers for the week came from value sectors, specific corporate earnings catalysts, and defensive spaces.

While Tech and Consumer Cyclical sectors were slammed (down over 5% for the week), defensively positioned sectors managed to finish the week green.

MRVL (+28.50%): Massive early-week momentum kept it at the top of large-cap gainers, though it gave back 12% during Friday's chip rout.

TWLO (+18.54%): Strong enterprise software demand metrics insulated it from the hardware/semiconductor specific drop.

PK (+15.73%): a powerful mix of positive operational updates from the company and a wave of analyst price target upgrades, all supported by strong broader macro trends in the hotel industry.

HUM (+14.58%): driven by two powerful, compounding factors: a proactive guidance reaffirmation from management that triggered major Wall Street upgrades, followed by a sector-wide rotation into defensive, margin-improving value stocks.

HPE (+14.31%): The company delivered a significant "beat-and-raise" quarter that fundamentally changed how the market was pricing its growth, particularly regarding AI infrastructure and networking demand.

Notable losers for the week of June 1st – June 5th

The week of June 1st–5th ended in a dramatic split. While a few defensive and value pockets stayed green, the broader market suffered its worst single-day rout since October on Friday, June 5th. The primary culprit was a severe liquidation in technology—specifically semiconductors—paired with a hot jobs report that stoked interest rate fears.

Growth sectors and high-valuation tech took the brunt of the damage, wiping out over $1 trillion in market value from the chip sector alone in a single afternoon.

The notable observation is that MU held up roughly in line with AMD and significantly better than AVGO, while COIN essentially mirrored the sharp decline in Bitcoin, making it the weakest performer of the group.

AVGO (-14.30%): +Reported its fiscal Q2 earnings after the close on Wednesday, June 3rd. While it technically beat current revenue and EPS estimates, its Q3 AI chip sales guidance of $16 billion fell short of the $17.2 billion Wall Street expected. Management's refusal to lift full-year AI forecasts ignited severe valuation exhaustion across the entire semiconductor space.

INTC (-9.38%): Suffered heavy collateral damage following Broadcom's cautious AI outlook. Investors rapidly reassessed the near-term pace of enterprise and PC chip-refresh cycles, prompting a steep de-rating.

AMD (-6.75%): Caught directly in the semiconductor wake, high-multiple growth stocks were hammered doubly hard on Friday when a hot May jobs report pushed the 10-year Treasury yield up to 4.55%, making expensive AI multiples harder to justify.

MU (-6.40%): Swept up in the chip rout and compounded by growing analyst notes warning of short-term pricing pressure and a deepening near-term memory chip inventory digestion phase.

COIN (-18.40%): Slumped aggressively over the week as digital assets retreated. High-yielding Treasury yields took the wind out of speculative assets, driving capital into traditional cash-flowing defensives.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

Equities began June on a strong note, with the major indexes closing at fresh record highs. The dominant theme was continued enthusiasm for artificial intelligence and technology spending. Semiconductor and software stocks led the advance, helped by new AI-related announcements from Nvidia and optimism surrounding the broader AI ecosystem. Energy stocks also performed well as oil prices surged. Despite geopolitical tensions involving Iran, investors largely focused on earnings strength, economic resilience, and AI-driven growth.

Market breadth was somewhat narrow, however, with leadership concentrated in technology and energy while sectors such as utilities and consumer discretionary lagged.

Treasury prices fell and yields rose as investors reacted to a sharp increase in oil prices and renewed concerns about Middle East tensions. Higher energy prices revived inflation concerns, reducing demand for Treasuries. The 10-year Treasury yield climbed to roughly 4.48%, up a few basis points from the prior session.

Oil was the biggest story of the day. Crude prices surged after reports that U.S.-Iran negotiations had deteriorated and concerns grew about potential disruptions to oil flows through the Strait of Hormuz. WTI crude briefly traded around $90 per barrel and ultimately finished the session more than 5% higher, while Brent crude rose over 4%. Although prices pulled back somewhat from their intraday highs, energy markets clearly shifted into risk-premium mode.

Gold declined despite the geopolitical uncertainty. Normally a safe-haven asset, gold came under pressure because rising oil prices increased inflation expectations and reinforced the possibility of a more hawkish Federal Reserve. Investors instead favored equities and the U.S. dollar. Gold futures fell by more than 1% during the session.

- S&P 500: 7600.25 (+0.27%)

- Nasdaq Composite: 27086.81 (+0.42%)

The key takeaway for the day was that AI optimism and technology leadership outweighed rising oil prices and geopolitical risks, allowing both the S&P 500 and Nasdaq to notch new record closes.

Tuesday's Markets and News:

Equities continued their march to new record highs, although gains were much more modest than on Monday. The primary driver remained enthusiasm surrounding artificial intelligence spending and infrastructure investment. Semiconductor stocks were particularly strong after positive comments from Nvidia CEO Jensen Huang about the future of AI hardware and networking, helping lift names such as Marvell and the broader chip sector. Strong earnings from Hewlett Packard Enterprise also supported sentiment.

The market digested news that Alphabet planned to raise $80 billion to fund AI infrastructure expansion. While Alphabet shares fell on dilution concerns, investors largely interpreted the announcement as further evidence that the AI investment cycle remains in full force. Small-cap stocks outperformed, with the Russell 2000 gaining nearly 1%.

Despite the record highs, leadership remained concentrated in AI-related sectors, and market participants were increasingly watching whether the rally could broaden beyond technology and semiconductors.

Treasury yields eased slightly during the session despite stronger-than-expected JOLTS job openings data. The 10-year Treasury yield finished near 4.50%, suggesting bond investors were not yet pricing in a significant shift toward tighter Federal Reserve policy. The modest decline in yields provided a supportive backdrop for equities.

Oil remained elevated as traders continued to assess the risk of supply disruptions tied to tensions involving Iran and the Strait of Hormuz. After an early decline, crude recovered during the U.S. session and finished higher. WTI crude settled around the low-$90s per barrel, maintaining much of the geopolitical risk premium that had developed the previous day.

The market appeared unconvinced that a diplomatic resolution was imminent, keeping energy prices firm despite intermittent reports of ongoing negotiations.

Gold traded in both directions during the day but ultimately finished little changed to slightly higher. Early buying was driven by geopolitical uncertainty and safe-haven demand, while stronger-than-expected labor-market data later in the session limited gains. The result was a relatively quiet day for gold compared with the moves in equities and oil.

- S&P 500: 7609.78 (+0.13%)

- Nasdaq Composite: 27093.90 (+0.03%)

This day was another example of the market's willingness to look past geopolitical risks and focus on the AI growth story. Oil remained elevated, Treasury yields were stable, and stocks reached fresh records as investors continued to reward companies positioned to benefit from the ongoing AI spending boom.

Wednesday's Markets and News:

Equities experienced the first meaningful pullback after a series of record highs. Investors shifted into a more cautious posture as tensions in the Middle East intensified and oil prices moved sharply higher. The prospect of prolonged disruptions around the Strait of Hormuz raised concerns that higher energy costs could rekindle inflation pressures and complicate the Federal Reserve's path.

Technology and financial stocks led the decline. Much of the market's recent leadership came under pressure as investors took profits after the strong AI-driven rally. However, semiconductor stocks showed relative resilience, with some chipmakers advancing despite the broader market weakness, suggesting that enthusiasm for AI infrastructure spending remained intact.

Market breadth deteriorated noticeably, with declining stocks outnumbering advancing stocks across both the NYSE and Nasdaq. Small caps also underperformed, reflecting a broader reduction in risk appetite.

Treasury yields moved higher during the session as investors weighed stronger economic data and the inflationary implications of rising oil prices. A solid ISM Services report reinforced the view that the economy remained resilient, while energy-driven inflation concerns reduced demand for longer-dated Treasuries. Markets also modestly increased expectations that the Fed could maintain restrictive policy for longer than previously anticipated.

Oil was again at the center of market attention. Crude prices surged after renewed military activity involving Iran and U.S. forces heightened fears of supply disruptions in the Persian Gulf. Brent crude rose above $97 per barrel, while WTI crude approached $96. The market began pricing in a larger geopolitical risk premium amid concerns that shipping through the Strait of Hormuz could be affected. The oil rally was significant because investors viewed it not merely as a geopolitical event but as a potential inflation shock that could ripple through the broader economy.

Gold declined despite the increase in geopolitical tensions. Normally a beneficiary of safe-haven flows, gold instead faced pressure from a stronger U.S. dollar and rising interest-rate expectations. Investors worried that higher oil prices could keep inflation elevated and force central banks to remain restrictive, reducing the appeal of non-yielding assets such as gold. Gold futures fell roughly 1% on the day.

- S&P 500: 7553.68 (-0.74%)

- Nasdaq Composite: 26,853.98 (-0.89%)

The day signified a shift from the AI-fueled optimism that had driven markets to record highs earlier in the week. Rising oil prices and escalating Middle East tensions brought inflation concerns back to the forefront, triggering profit-taking across equities. While the AI theme remained intact, macroeconomic and geopolitical risks temporarily took control of the tape.

Thursday's Markets and News:

Equities experienced a decidedly risk-off session, with stocks suffering their sharpest decline of the week. The catalyst was a disappointing earnings report and outlook from Broadcom, which raised concerns that the pace of AI-related spending might not be sufficient to justify the lofty valuations across the semiconductor sector.

Chip stocks were hit hard, and the selling quickly spread beyond semiconductors into the broader technology complex. Investors who had driven the market to record highs earlier in the week began reducing exposure to many of the market's biggest winners. The Nasdaq led the decline as growth and AI-related stocks came under heavy pressure. Financials and cyclicals also weakened as risk appetite deteriorated. News that several major AI infrastructure projects could face delays added to the cautious tone. Market breadth was broadly negative, with decliners significantly outnumbering advancers across major exchanges.

Treasury yields rallied as investors sought safety amid the equity selloff. The resulting demand pushed yields lower across much of the curve. The move suggested that investors were becoming more concerned about growth risks than inflation risks, at least for the day.

The bond market also reacted to softer-than-expected economic data released during the week, reinforcing expectations that the Federal Reserve might have room to ease policy later in the year if economic momentum slows.

Oil prices retreated after several days of strong gains. Traders took profits following the sharp geopolitical-driven rally earlier in the week, and some reports suggested diplomatic efforts involving Iran had not completely broken down.

WTI crude remained elevated relative to prior weeks, but the pace of the advance slowed considerably. The pullback in oil helped reduce some of the inflation fears that had weighed on markets the previous day.

Gold stabilized and moved modestly higher as investors sought defensive assets during the technology-led equity selloff. Falling Treasury yields also provided support for precious metals.

While gold did not experience a dramatic surge, it attracted safe-haven flows that had been largely absent earlier in the week when rising yields had pressured the metal.

- S&P 500: 7584.31 (+0.41%)

- Nasdaq Composite: 26,830.96.21 (-0.09%)

This day marked the point where the market's AI-driven optimism encountered a significant reality check. A sharp selloff in semiconductor stocks—particularly following Broadcom's earnings—triggered broader weakness across technology shares. Investors rotated toward Treasuries and defensive assets, while oil cooled after its earlier geopolitical surge. The day reinforced how dependent market leadership had become on continued confidence in the AI investment theme.

Friday's Markets and News:

Equities ended the week with a decisive risk-off finish, selling off broadly as the market finally absorbed the cumulative impact of the week's volatility. After Thursday's rebound, sentiment reversed as investors focused on tightening financial conditions, elevated oil prices, and signs that the AI-driven rally may have become stretched in the short term.

Technology led the decline, with semiconductor and high-momentum AI-related names under pressure again. The prior week's leadership group continued to see profit-taking, and breadth weakened noticeably as defensive positioning increased into the weekend. Cyclical sectors such as industrials and consumer discretionary also lagged, while only defensive pockets such as utilities and staples showed relative resilience.

Treasury bonds caught a bid as equities sold off, with yields drifting lower across the curve. The move reflected a classic flight-to-quality response, as investors rotated into government bonds amid renewed equity volatility.

However, inflation concerns tied to elevated energy prices continued to limit the size of the rally in bonds. The market remained caught between slower-growth signals from equities and inflation pressure from crude oil.

Oil remained one of the dominant macro drivers of the week. Prices stayed elevated despite some intraday volatility, as traders continued to price in geopolitical risk premiums tied to Middle East tensions and potential supply disruptions. While there were no major new escalations on Friday, crude remained at levels high enough to keep inflation expectations elevated and to weigh on risk assets broadly.

Gold traded higher on the day as investors sought safety amid the equity selloff and ongoing macro uncertainty. Softer Treasury yields provided additional support, and gold benefited from renewed demand for hedges against both geopolitical and inflation risks.

The metal continued to behave more like a traditional safe-haven asset again after earlier mixed signals earlier in the week.

- S&P 500: 7383.74 (-2.64%)

- Nasdaq Composite: 25709.43 (-4.18%)

Today's market action can be best characterized as a violent, macro-driven growth shakeout and valuation reset, marking the worst single-day rout for the broader markets since October.

It was a classic "good economic news is bad news for stocks" setup, where a red-hot labor report triggered systematic de-risking across expensive growth multiples, while defensive and value-oriented sectors acted as shock absorbers.

Notable Earnings (June 8th – 12th)

While the primary market catalysts this week are structural macroeconomic releases, the corporate earnings calendar features several highly anticipated reports capable of driving significant single-stock implied volatility. Software infrastructure and artificial intelligence spending will take center stage mid-week, acting as an important fundamental health check for corporate technology budgets. Additionally, critical reports out of the consumer retail, home building, and consumer staples sectors will provide direct insights into the resilience of discretionary spending under persistent monetary constraints.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, June 8th: CPB / MTN / AVO

Tuesday, June 9th: SJM / CASY / GME / ASO / CBRL / SFIX / PLAY

Wednesday, June 10th: ORCL / CHWY / OXM

Thursday, June 11th: ADBE / LEN / RH

Friday, June 12th: No noteworthy corporate earnings reports scheduled.

Economic Calendar (June 8th – 12th)

Following a stronger-than-expected May Employment Report (Non-Farm Payrolls expanding by 172,000 versus the 85,000 baseline expectation), the macroeconomic spotlight shifts entirely to inflation data and central bank policy. Volatility expectations remain elevated heading into mid-week as the market continues to recalibrate the probability and timing of potential interest rate adjustments.

The primary domestic catalysts will be the back-to-back releases of May consumer and producer price data, which will serve as crucial inputs ahead of the upcoming mid-June FOMC policy decision. Internationally, options traders must also keep an eye on interest rate decisions coming out of both Canada and Europe, which are poised to shift global currency and fixed-income dynamics.

Monday, June 8th:

- NY Fed Consumer Inflation Expectations (May): Tracks public sentiment regarding short-term inflation paths, a key forward-looking variable monitored closely by the Federal Reserve.

Tuesday, June 9th:

- U.S. Balance of Trade (April): Expected to show a minor widening of the trade deficit to approximately -$57.9B from -$55.5B previously.

- NFIB Business Optimism Index (May): Provides critical insight into small business spending intentions, hiring trends, and general sentiment.

- Existing Home Sales (May): Anticipated to hold steady at a seasonally adjusted annualized rate near 4.04M units, acting as a direct gauge of housing market liquidity under current rate constraints.

Wednesday, June 10th:

- U.S. Consumer Price Index (May) Key Event of the Week: The headline inflation metric. Markets are bracing for a year-over-year CPI reading near 4.0%, while Core CPI (excluding food and energy) is forecasted to show a minor monthly deceleration to 0.3% growth versus 0.4% in the prior month. Expect significant broad-market velocity upon release.

Thursday, June 11th:

- U.S. Producer Price Index (May): Wholesale inflation data. This serves as the underlying input for corporate margins and acts as a leading indicator for subsequent consumer-side price pressures.

- Weekly Initial Jobless Claims: Standard weekly labor market liquidity update to track if the low-layoff trend established in May carries forward.

Friday, June 12th:

- Preliminary University of Michigan Consumer Sentiment Index: Measures early June consumer spending confidence, alongside critical metrics tracking long-term inflation expectations.

Blue Sky Horizons

The 2026 Tipping Point

The biggest macro structural shift happening right now is the massive operational pivot from Cloud AI to Agentic Edge AI, driven by a new technological symbiosis: Small Language Models (SLMs) running on specialized local hardware.

For the last several years, the tech narrative was dominated by massive, centralized cloud data centers running gargantuan Large Language Models (LLMs). But that playbook is hitting a hard wall due to a simple law of physics: latency.

The industry has largely completed the massive, capital-intensive "training" phase of AI in the cloud. Now, the focus has shifted to inference—the actual real-time execution of AI models where the users and data live.

Centralized cloud processing incurs a round-trip network latency of roughly 100 to 300 milliseconds. For emerging agentic AI systems (autonomous software tools that must continuously sense, reason, and act in real time), that delay is unacceptable. Real-time industrial automation, computer vision defect tracking, and collaborative robotics require localized decision-making in under 5 milliseconds.

This shift is being enabled by two simultaneous breakthroughs:

- Model Optimization (The Software): Engineers are successfully shrinking multi-billion parameter models down to a fraction of their size using techniques like quantization (using lower-precision numbers) and knowledge distillation (transferring large-model intelligence into compact ones). These "Micro LLMs" or SLMs fit directly onto localized devices without significant losses in operational accuracy.

- Specialized Silicon (The Hardware): Major semiconductor companies are now shipping standard Neural Processing Units (NPUs) inside everyday edge devices, enterprise gateways, and industrial machinery. These chips process neural network tasks up to 10 to 20 times more energy-efficiently than traditional CPUs or mainstream GPUs, drawing as little as 2.5 watts.

For enterprises and self-directed investors tracking long-term structural trends, the move to the Edge solves the two biggest headaches of the cloud era:

- Exploding API Costs: Constantly pinging cloud APIs for thousands of local data streams is financially unsustainable at scale. Shifting inference workloads to the edge is yielding documented cloud cost reductions of 30% to 50%.

- Absolute Data Sovereignty: Processing data entirely on-site means sensitive operational code, financial parameters, or proprietary manufacturing recipes never cross a public network, providing an airtight security layer.

The future of infrastructure is no longer about building bigger centralized warehouses of data; it's about connecting a highly distributed network of intelligent, self-contained endpoints that operate entirely at the edge.

The Edge AI Transformation explains how the deployment of autonomous, agentic AI directly into billions of edge devices is fundamentally rewriting global digital infrastructure and security.

Thank you for reading. Until next week's close,

Safe Trading!

Fauzia Timberlake

About the Author: Fauzia Timberlake is a professional options coach and financial strategist specializing in risk management and portfolio architecture for self-directed investors. She is Founder and Managing Partner of Option Engines.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the Trade Ideas tab on our website.