Post-FOMC Sector Dispersion

By Fauzia Timberlake,

personal coach for trading options

June 22, 2026

Market Roundup & The Week in Review

The capital markets navigated a highly volatile, event-driven four-session week, bracketed by monumental shifts in both geopolitics and monetary policy. The primary narrative revolved around a stark tug-of-war between structural global relief and a newly aggressive domestic interest rate outlook, culminating in defensive rotations and an erratic risk-on bounce to round out the period.

The definitive market driver early in the week was the formal signing of a landmark diplomatic agreement between the United States and Iran. The historic deal should effectively bring an end to active regional hostiles and guarantee the secure, unhindered reopening of the critical Strait of Hormuz to global shipping traffic. This provided an immediate structural relief valve for global trade logistics.

The monetary landscape shifted dramatically on Wednesday, June 17th, during Kevin Warsh's maiden policy meeting as the newly appointed Chairman of the Federal Reserve. While the FOMC ultimately voted to leave the benchmark federal funds rate unchanged, the accompanying policy statement and Summary of Economic Projections (the "dot plot") delivered a decidedly hawkish shock to fixed-income markets. The committee eliminated its previous monetary easing bias, with updated projections signaling a rising probability of a final rate hike before the end of 2026 to firmly stamp out lingering core inflation.

Equity benchmarks experienced substantial intra-week churn, selling off sharply post-FOMC before staging an aggressive, short-covering relief rally on Thursday to reclaim the bulk of their weekly losses. Underneath the surface, the performance dispersion across equity sectors was extreme. Energy (XLE) bore the absolute brunt of the weekly downside, plunging nearly -4.73% as the geopolitical breakthrough prompted an immediate structural unwinding of the global risk premium in energy complex positions. Conversely, small-caps (IWM) and domestic value plays showed notable resilience against high-beta megacap software volatility, outperforming large-cap indexes over the course of the week.

The raw commodity space bore the primary burden of the geopolitical repricing. WTI Crude Oil plummeted over -5.7% across the four sessions to finish at $76.60, rendering a massive 8.3 million barrel weekly draw reported by the EIA completely irrelevant to price action. Concurrently, precious metals drifted south; GLD shed -1.04% as rising real yields and a structurally fortified U.S. dollar restricted gold's upside momentum.

The Treasury complex underwent violent, multi-directional swings. Yields surged dramatically on Wednesday afternoon following Chair Warsh's press conference as bonds priced out near-term cuts, before settling marginally flatter on Thursday afternoon with the 10-Year Treasury Yield ($TNX) stabilizing near the 4.46% mark.

Crypto liquidity felt the direct weight of a restrictive "higher-for-longer" monetary stance. Bitcoin (BTC/USD) broke down below key psychological support at the $65,000 handle ostensibly due to persistent capital outflows from spot exchange-traded products. Meanwhile, the Cboe Volatility Index (VIX) spiked toward the 18.50 level mid-week on macro uncertainty before collapsing back down over 11% on Thursday to finish the cycle virtually flat as automated option hedging programs smoothed out risk premiums ahead of the long holiday weekend.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

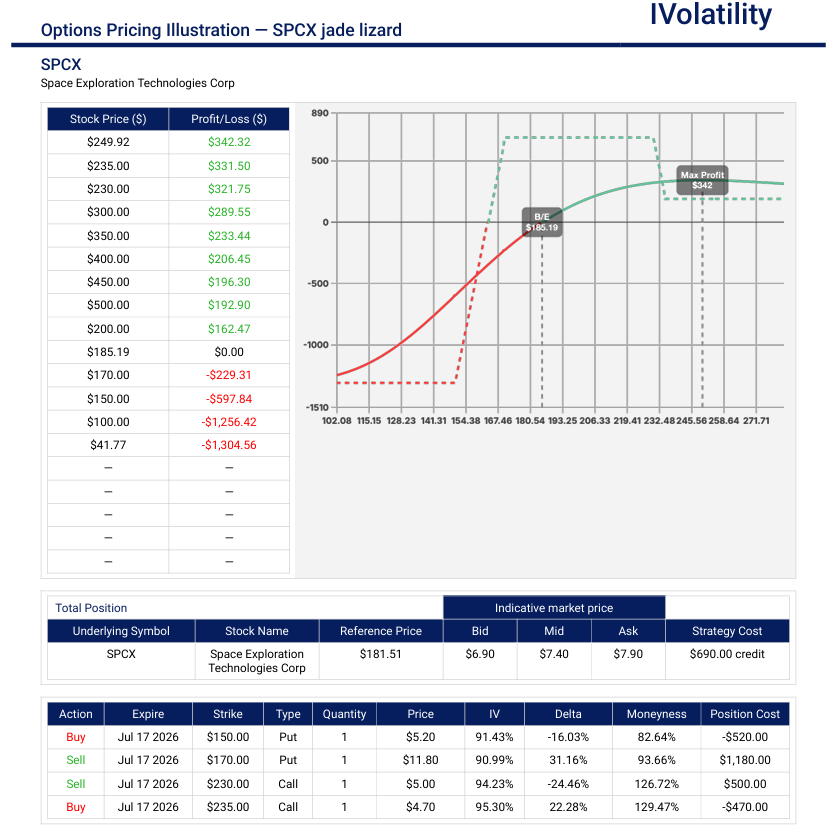

SPCX (closed at 184.98 on Thursday, June 18th)

After a highly volatile debut week that saw shares peak near $201 before compressing back to a Thursday close of $185.00, the underlying asset is stabilizing into a distinct, high-conviction entry window.

Outlook: bullish

Strategy: Jade Lizard

In the July monthly expiration, SELL the 150/170 put spread and SELL the 230/235 call spread

Premium collected: about $700 /contract

Net Position Delta around +14

No risk to the upside (because the $5 wide call spread is covered by the total credit received); downside BE is around 163

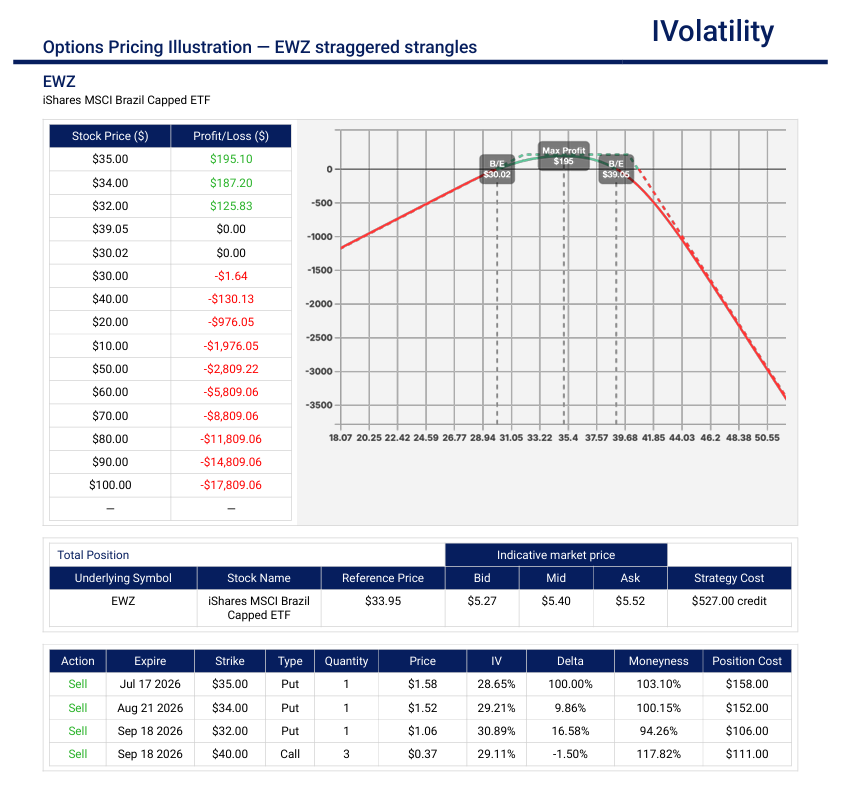

EWZ (closed at 33.73 on Thursday, June 18th)

With the broader equity landscape grappling with peak valuations in domestic tech, the emerging market complex—specifically EWZ—presents a highly compelling asymmetric risk-reward profile for the next 90 days. Following a steep multi-week liquidation that pulled the ETF down to a Thursday close of $33.73, the selling could have exhausted weak retail hands and driven the underlying into an oversold technical value zone.

Outlook: bullish

Strategy: Staggered strangles

Sell staggered puts over time, with the near-term being more aggressive than the far term

Sell the July17 35put AND the Aug24 34put AND the Sep18 32put AND 3 of the Sep18 40calls.

Premium collected: about $600 for these contracts

Breakevens around 30 and 42

Movement of the Major Market Indices:

The major multi-asset benchmarks carved out a highly volatile but ultimately constructive path during the four-session holiday week. Equities caught a massive global tailwind early on as a major geopolitical breakthrough sent energy costs plunging, though those gains were fiercely tested midweek by a surprisingly hawkish Summary of Economic Projections (SEP) from the Federal Reserve. Ultimately, institutional buyers stepped back in on Thursday, lifting the large-cap equity trackers to a green finish for the week, while commodity and fixed-income spaces underwent massive structural repricings.

| INDEX | UP | DOWN |

| SPY | -0.22% | |

| QQQ | 0.38% | |

| IWM | -0.09% | |

| DIA | -0.71% | |

| GLD | -1.26% | |

| BTC/USD | -3.52% | |

| 10-year yield | -0.22% | |

| Crude Oil | -7.36% | |

| VIX | -2.21% |

Movement of the Major Market Sectors:

The institutional positioning and calculated defense that anchored the market through the early June inflation shocks shifted into a highly dynamic, two-speed execution process during the holiday-shortened trading week. Rather than navigating a singular macro narrative, institutional desks spent the four-session week actively balancing an extraordinary dual-axis clearing event: an immense geopolitical relief rally triggered by a tentative U.S.-Iran ceasefire, directly cross-cut by an aggressively hawkish structural surprise from newly-appointed Fed Chair Kevin Warsh's maiden FOMC meeting.

The resulting capital flows revealed a disciplined, highly targeted approach to sector exposure. Instead of a uniform risk-on or risk-off sequence, managers aggressively rewarded structural beneficiaries of the sudden plunge in crude oil—which saw Brent slide back below $80 per barrel—while simultaneously punishing high-multiple, long-duration equity structures that face valuation compression under the Fed's updated "higher-for-longer" projection of potential future hikes. Performance across the major sector trackers followed a precise pattern of macro repricing, characterized by heavy liquidation in enterprise software and robust, value-oriented accumulation across global transport, cyclicals, and select hardware nodes.

| SECTOR | UP | DOWN |

| TECH (XLK) | 0.56% | |

| FINANCIALS (XL) | -0.35% | |

| INDUSTRIALS (XLI) | 1.18% | |

| ENERGY XLE | -2.59% | |

| HEALTHCARE (XLV) | -2.80% | |

| UTILITIES (XLU) | 0.63% | |

| MATERIALS (XLB) | -2.00% | |

| REAL ESTATE (XLRE) | -3.22% | |

| CONSUMER STAPLES (XLP) | -2.54% | |

| CONSUMER DISCRETIONARY (XLY) | -1.22% |

Notable gainers for the week of June 15th – June 19th

While the Federal Reserve's hawkish stance forced a severe re-evaluation of high-multiple software architectures, the broader market uncovered substantial areas of strength. The primary capital inflows concentrated in companies benefiting directly from structural macroeconomic relief and massive capital deployment. As geopolitical breakthrough negotiations drove energy costs sharply lower, institutional managers rotated aggressively into heavy cyclical transportation lines and advanced hardware manufacturers that stand to thrive in a resilient, high-growth economic environment.

The notable gainers last week highlighted concentrated accumulation across global logistics and tech-hardware networks:

- CARNIVAL CORPORATION (CCL, +14.25%): The cruise line operator experienced explosive institutional accumulation following the dramatic slide in global crude prices. With Brent crude plunging back below the $80-per-barrel mark, the street rapidly modeled massive fuel cost savings and expanding operating margins, triggering a major technical breakout on high volume.

- KLA CORPORATION (KLAC, +12.60%): The semiconductor equipment heavyweight defied the broader software sector liquidation to lead tech hardware higher. Capital desks heavily favored direct infrastructure and inspection nodes, identifying processing-layer hardware as a vital, defensive beneficiary of the ongoing semiconductor manufacturing expansion.

- FEDEX CORPORATION (FDX, +9.15%): The global logistics giant saw strong buying pressure ahead of its upcoming earnings release. The sudden de-escalation of maritime bottlenecks along international shipping lanes, paired with resilient domestic economic output, prompted managers to aggressively accumulate the stock as a primary vehicle for broad cyclical growth.

Notable losers for the week of June 15th – June 19th

While the broader indices attempted to digest the Federal Reserve's hawkish structural shift, underlying market mechanics exposed pockets of acute distribution. The primary downside damage was concentrated in high-multiple enterprise software, cloud platforms, and specific semiconductor heavyweights undergoing intense valuation checks. As institutional desks aggressively repriced risk in response to higher-for-longer interest rate commentary, growth architectures with premium valuations faced a sudden, disciplined liquidation from managers defending corporate margin exposure.

The notable losers last week revealed concentrated distribution across large-cap tech and enterprise growth structures:

- ADOBE INC. (ADBE, -18.85%): The creative software giant faced intense institutional selling pressure, leading large-cap software decliners. Capital flows turned sharply negative as participants grew highly sensitive to premium valuations in enterprise software, favoring immediate hardware nodes over high-multiple application layers.

- PTC INC. (PTC, -17.02%): The industrial software and IoT platform provider experienced significant liquidation throughout the week. Institutional desks actively de-risked companies tied to corporate capital expenditure budgets, triggering a sharp technical breakdown below key moving averages.

- ORACLE CORPORATION (ORCL, -13.83%): Despite recent cloud momentum, the database and enterprise software heavyweight suffered a notable pullback. The hawkish shift from the FOMC forced a rapid macro repricing of long-duration growth assets, prompting managers to lock in profits and rotate out of core tech positions.

Review selected market indices below:

Daily Notable Market Action

Market Summary for Monday, June 15th

Global equity markets staged a massive worldwide rally as oil prices plummeted following news that the United States and Iran reached a tentative ceasefire agreement to reopen the critical Strait of Hormuz. The steep decline in energy costs, with Brent crude dropping 4.8% back to early March levels, significantly eased global inflation and corporate margin concerns. The news sparked a powerful surge in mega-cap technology and semiconductor companies, overshadowing previous geopolitical friction and prompting intense institutional buying across risk assets.

S&P 500: 7,554.29 (+1.68%)

Nasdaq Composite: 26,683.94 (+3.07%)

Market Summary for Tuesday, June 16th

Wall Street delivered a mixed performance near all-time highs as a rotation out of mega-cap artificial intelligence winners offset continuing optimism over energy prices. While Brent crude slid below $80 per barrel for the first time since March, triggering strong gains in financial and industrial sectors that pushed the Dow to a record close, localized profit-taking in heavyweights like Nvidia and Advanced Micro Devices dragged down the tech benchmarks. Meanwhile, macro traders stayed on the sidelines ahead of the upcoming mid-week Federal Reserve policy announcement.

S&P 500: 7,511.35 (-0.57%)

Nasdaq Composite: 26,376.34 (-1.16%)

Market Summary for Wednesday, June 17th

Stocks suffered a broad-based, sharp decline following the conclusion of the highly anticipated Federal Reserve policy meeting. While the central bank left the benchmark interest rate unchanged as expected, the newly updated Summary of Economic Projections (SEP) delivered a hawkish surprise, revealing that half of the committee now projects at least one additional interest rate hike before the end of the year. This restrictive forward guidance sent Treasury yields higher and triggered a widespread liquidation across high-multiple growth and technology sectors.

S&P 500: 7,420.10 (-1.21%)

Nasdaq Composite: 26,021.66 (-1.34%)

Market Summary for Thursday, June 18th

Equity benchmarks rebounded dynamically, recovering the vast majority of the prior session's losses as geopolitical relief countered interest-rate anxieties. Sentiment turned highly positive following news that the U.S. and Iran officially signed the formal accord to end their conflict and permanently restore commercial shipping traffic through the Strait of Hormuz. Fixed-income pressures eased alongside a stabilization in crude prices, encouraging institutional managers to aggressively buy the dip in tech, growth, and small-cap indexes ahead of a long holiday weekend.

S&P 500: 7,500.58 (+1.08%)

Nasdaq Composite: 26,517.93 (+1.91%)

Market Summary for Friday, June 19th

US financial markets were closed in observance of the federal JuneTeenth holiday.

Notable Earnings (June 22nd – 26th)

While the broader corporate earnings season won't begin in earnest until mid-July, next week features a highly influential micro-slate of reports that will serve as critical crosscurrents for specific industry sectors. Headlining the docket are key indicators for global logistics, tech-infrastructure demand, and consumer discretionary spending. Options desks will be looking closely at forward-looking guidance to gauge input cost pressures and consumer resilience heading into the second half of the year.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, June 22nd: FDS

Tuesday, June 23rd: FDX / CCL / KBH

Wednesday, June 24th: MU / PAYX

Thursday, June 25th: DRI / MKC / NKE

Friday, June 26th: No noteworthy reports are scheduled

Economic Calendar (June 22nd – 26th)

Following a turbulent week defined by the Federal Reserve's hawkish shift under new Chair Kevin Warsh, the spotlight pivots from central banking to hard data. Volatility expectations remain elevated as the final trading week of the quarter prompts significant institutional portfolio rebalancing. Market participants will focus heavily on incoming gauges of inflation, economic output, and consumer resilience to judge how well the economy is absorbing a higher-for-longer rate regime.

The focal point arrives Thursday with a massive data dump from the Bureau of Economic Analysis (BEA), headlining the final Q1 GDP estimate alongside May's Personal Consumption Expenditures (PCE) Price Index—the Fed’s preferred inflation metric. With the June FOMC dot plot revealing that half of the committee now projects at least one rate hike before year-end, options desks will parse these prints to see if sticky consumer demand or core pressures validate that hawkish outlook.

- Monday, June 22 – Fed Gov. Waller Speech / PBOC Rate Decision:

Governor Christopher Waller offers the first official commentary following last week's dramatic FOMC meeting.

Overnight, China announces its benchmark rate decision, providing critical context for global manufacturing health. - Tuesday, June 23 – S&P Global Flash US PMI (June):

Serves as the market's earliest look at domestic economic activity for the current month, mapping both manufacturing and services output for signs of stagflationary pressures. - Wednesday, June 24 U.S. Retail Sales (May):

Weekly housing data tracks the direct impact of elevated borrow rates, while Australia's CPI print will be closely watched for broader global inflationary trends. - Thursday, June 25 – May PCE Price Index, Q1 GDP (Final), & Jobless Claims:

This dual release of PCE inflation and final economic growth, paired with weekly labor metrics, will test equity and fixed-income valuations. - Friday, June 26 – Mid-Year Portfolio Rebalancing:

With no major economic releases scheduled, market action will be dominated by heavy institutional volume as managers close out books for the second quarter and position for the second half of 2026.

Blue Sky Horizons

Biocomputing & The DNA Data Revolution

While the market remains hyper-focused on silicon scarcity, power grid constraints, and the soaring costs of traditional data centers, a quiet revolution is taking place at the intersection of synthetic biology and computer science: Biocomputing.

As silicon nears its physical limits under the relentless demands of massive AI models, researchers are successfully utilizing synthetic DNA and living biological systems to process and store information. The efficiency metrics are staggering: a single gram of DNA can theoretically store up to 215 petabytes (215 million gigabytes) of data, capable of lasting thousands of years without degradation or power requirements. Simultaneously, biocomputers using lab-grown neurons are demonstrating the ability to perform basic computational tasks and pattern recognition at a microscopic fraction of the wattage consumed by today's advanced GPUs.

Discussions are moving past pure academic theory and entering the early stages of commercial viability. Tech giants and specialized biotech startups are actively funding research into DNA data storage to solve the enterprise archiving crisis. For forward-looking investors, this shifts the long-term paradigm. The future infrastructure bottleneck may not be resolved by mining more copper or building larger nuclear plants for silicon factories, but rather by the scalability of molecular biology, DNA synthesis companies, and bio-foundries. It is a frontier where the tech stack ultimately becomes organic.

Thank you for reading. Until next week's close,

Have a safe and productive Trading week !

Fauzia Timberlake

About the Author: Fauzia Timberlake is a professional options coach and financial strategist specializing in risk management and portfolio architecture for self-directed investors. She is Founder and Managing Partner of Option Engines.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to consider and/or analyze, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the Trade Ideas tab on our website.