Record Reconstitution Volumes Cloak a Sharp Sector Shakeout

By Fauzia Timberlake,

personal coach for trading options

June 29, 2026

Market Roundup & The Week in Review

The capital markets experienced a sharp architectural divergence during the final week of June, characterized by a pronounced "split-screen" performance across equity classes. While the broader market exhibited surprisingly robust underlying breadth, a significant valuation shakeout in the artificial intelligence and mega-cap technology ecosystem dragged the major capitalization-weighted benchmarks into negative territory.

The primary catalyst for the index-level pressure was a growing institutional anxiety surrounding AI capital expenditure and corporate valuation sustainability. After driving the broader market to historic heights throughout the first half of the year, premier technology and semiconductor names faced aggressive distribution as investors appeared to question whether near-term earnings growth could keep pace with parabolic stock trajectories. This pressure extended globally, sending shockwaves through Asian tech supply chains, with Softbank, SK Hynix, and Samsung experiencing large liquidations.

The Nasdaq Composite bore the absolute brunt of the weekly rotation while the S&P 500 showed greater structural resilience but still slipped 2.0%, marking just its second losing week in the past 13 cycles. In stark contrast, the Dow Jones Industrial Average gained while small-caps demonstrated persistent relative strength, with the Russell 2000 climbing to finish at 3,010.08.

In the commodity complex, energy markets completed a full round-trip as the geopolitical risk premiums stemming from the prior weeks' Middle Eastern friction entirely evaporated. International benchmark Brent crude plummeted to $72.60, effectively erasing the entirety of the price spike observed since the onset of regional hostiles. The capitulation in crude provided an immediate tailwind to transport and consumer-discretionary equities, offering a distinct structural relief valve for companies carrying heavy fuel overheads.

The fixed-income complex enjoyed a highly anticipated reprieve from the hawkish narrative introduced at Chair Warsh's maiden FOMC press conference. Treasury yields drifted lower across the curve, with the benchmark 10-Year Treasury Yield ($TNX) easing down to 4.37%. This bond market bid was amplified late in the week by a fresh macroeconomic reading showing that U.S. consumer one-year inflation expectations inched lower to 4.6% from 4.8% in May. While inflation expectations remain stubbornly elevated above the Fed's target, the minor downward trajectory offered a stabilizing anchor for domestic credit markets heading into the end of the quarter.

The core macroeconomic narrative of the week appeared to be crystal clear: a massive, sharp "split-screen" rotation out of premium-valuation tech/semis (QQQ -4.60%) to fund safe havens in blue-chip value, defensive healthcare, and small-caps (IWM +1.00%), all culminating in a record-shattering Russell reconstitution liquidity event.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

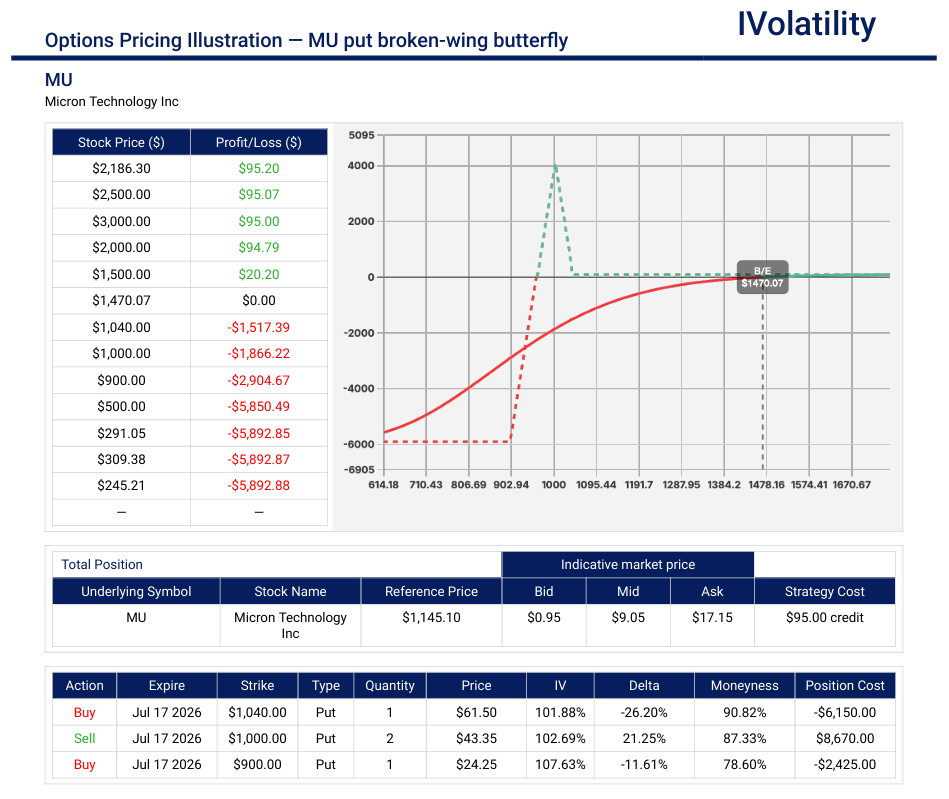

MU (closed at 1123.81 on Friday, June 26th)

Despite the broader tech-sector profit-taking that dragged the underlying stock down from its post-earnings highs, Micron's core fundamentals appear to be strong and structural demand for AI infrastructure remains insatiable. Traders could target a bullish entry near the $1,050 level which appears to be a critical support node.

Outlook: bullish

Strategy: Put Broken-wing Butterfly

In the July monthly expiration, buy ONE 1040put / sell TWO 1000puts / Buy ONE 1000put (to limit capital required)

Premium collected: about $900

No risk to the upside: downside breakeven around 1050

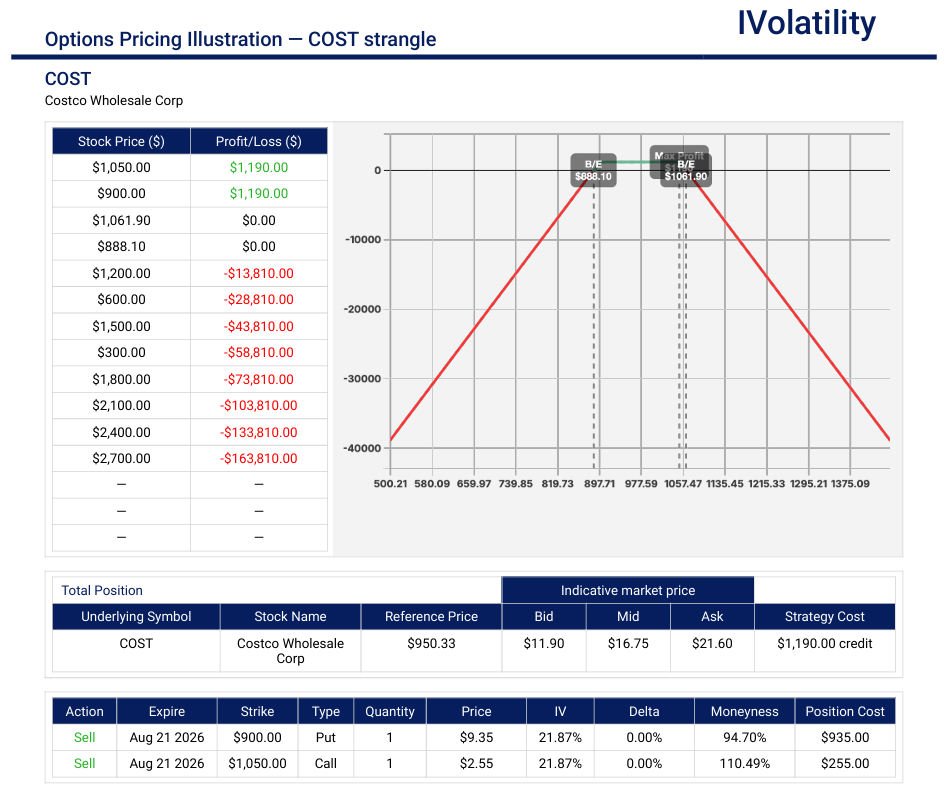

COST (closed at 950 on Friday, June 26th)

Costco continues to demonstrate immense fundamental insulation, making its consolidation around the $950 level a highly attractive accumulation zone for the near-term. As persistent inflationary pressures force a growing, younger demographic of budget-conscious consumers to seek maximum relative value, Costco's sticky 92.2% North American membership renewal rate and a robust 21.5% climb in digital sales provide incredible cash-flow visibility. Leaning bullish over the next 54 days may allow options traders to capture a premium, ultra-defensive market leader right as the broader tape rotates away from high-beta tech volatility into safe-haven corporate stalwarts with structural, recession-resistant demand.

Outlook: leaning bullish

Strategy: Short strangle

In the August monthly expiration, sell the 900/1050 strangle

Premium collected: about $900

Downside risk around 890 and upside risk around 1060

Movement of the Major Market Indices:

The major multi-asset benchmarks carved out a highly bifurcated path during the final week of June, exposing a massive structural drift beneath the index surface. Large-cap equity trackers faced intense distribution as an aggressive institutional profit-taking wave rippled through high-beta artificial intelligence and semiconductor structures. Traditional blue-chip value, defensive healthcare sectors, and small-cap assets caught a strong rotational bid, functioning as key capital sanctuaries.

| INDEX | UP | DOWN |

| SPY | -1.96% | |

| QQQ | -4.62% | |

| IWM | 0.59% | |

| DIA | 0.18% | |

| GLD | -3.43% | |

| BTC/USD | -4.77% | |

| 10-year yield | -2.89% | |

| Crude Oil | -7.88% | |

| VIX | 8.40% |

Movement of the Major Market Sectors:

The institutional positioning and calculated defense that anchored the market through the mid-June policy shifts accelerated into an aggressive, high-velocity capital redeployment campaign during the final full week of June.

| SECTOR | UP | DOWN |

| TECH (XLK) | -6.25% | |

| FINANCIALS (XL) | -0.09% | |

| INDUSTRIALS (XLI) | 0.23% | |

| ENERGY XLE | 0.64% | |

| HEALTHCARE (XLV) | 7.37% | |

| UTILITIES (XLU) | 3.87% | |

| MATERIALS (XLB) | 0.82% | |

| REAL ESTATE (XLRE) | 3.60% | |

| CONSUMER STAPLES (XLP) | 2.47% | |

| CONSUMER DISCRETIONARY (XLY) | -1.40% |

Notable Gainers Week of June 22nd – June 26th

While the broader market benchmarks reeled under a severe re-evaluation of high-multiple technology architectures, institutional capital aggressively uncovered pockets of profound fundamental strength. The week's primary capital inflows concentrated in deep value, healthcare, and software-alternative structures carrying highly predictable corporate earnings streams. As managers executed their risk-mitigation blueprints, select large-cap value players and defensive behemoths experienced explosive accumulation, completely decoupling from the tech-heavy index drag.

The notable gainers this week highlighted this concentrated accumulation across the value and healthcare landscapes:

- BLACKBERRY (BB, +35.50%): The cybersecurity and automotive software specialist experienced an extraordinary surge in institutional buying. Emerging as a major alternative safety valve for managers de-risking out of premium-valuation enterprise AI structures, BB triggered a massive technical breakout on volume that far exceeded its historical averages.

- BAYER AG (BAYRY, +25.92%): The international pharmaceutical and life sciences group drew an intense defensive bid as capital aggressively sought refuge inside classic low-beta cohorts. Driven by macro sector rotation into the global healthcare complex, the stock broke structurally higher to lock in its strongest single-week performance of the cycle.

- ELI LILLY & CO. (LLY, +7.10% on Friday): The pharmaceutical giant spearheaded the broader healthcare breakout late in the week. LLY witnessed sharp institutional accumulation following a highly favorable regulatory update out of the European Medicines Agency, demonstrating how dominant, cash-flow-rich defensive names could carry an otherwise flat-to-red tape on Friday.

Notable Losers Week of June 22nd – June 26th

The notable losers this week reflected the aggressive profit-taking and thematic rotation:

- SPACEX (SPCX, -16.40%): The high-profile market newcomer faced severe institutional distribution, marking its third consecutive decline. Following a massive post-debut retail frenzy, the stock succumbed to intense macro gravity as risk sentiment soured across the broader AI ecosystem, especially following institutional rumors that OpenAI might delay its own public debut.

- MICRON TECHNOLOGY (MU, -6.69%): Despite delivering record-breaking Q3 fiscal 2026 earnings and guidance mid-week that initially sparked a brief short-covering bounce, the memory giant was hammered by intense post-earnings profit-taking to close the cycle sharply lower.

- BROADCOM (AVGO, -4.50%): The semiconductor and networking heavyweight felt the direct weight of the large-scale rotation out of large-cap hyperscaler vendors.

Review selected market indices below:

Daily Notable Market Action

Market Summary for Monday, June 22nd

U.S. equity markets drifted through a highly fragmented, "split-screen" session as an aggressive rotational wave out of mega-cap technology and semiconductor heavyweights masked substantial underlying strength across the rest of the tape. Investors locked in profits on premium-valuation tech structures following a massive rebalance of the Nasdaq-100, treating high-multiple tech names as a source of cash. The unlocked capital aggressively flooded into traditional blue-chip value and small-cap assets, pushing the Russell 2000 and the Dow sharply into positive territory.

Concurrently, international energy benchmarks fell roughly 3% as oil supplies continued to normalize through the Strait of Hormuz, providing a structural relief valve for transport and fuel-sensitive cyclical networks.

S&P 500: 7,472.79 (-0.37%)

Nasdaq Composite: 26,166.60 (-1.33%)

Market Summary for Tuesday, June 23rd

The global technology sell-off intensified dramatically, roaring back from a bloodbath in Asian markets to trigger aggressive liquidation across Wall Street. A massive tech correction in international chip supply chains—which saw South Korea's Kospi index plunge 10% intraday to trigger emergency circuit breakers—spilled directly into domestic AI heavyweights. Investors, increasingly anxious over high interest-rate projections and whether massive AI-related capital expenditure can justify current multiples, aggressively dumped high-beta semiconductor architectures. Conversely, blue-chip value and consumer staples served as primary capital sanctuaries, with defensive giants like Walmart and Procter & Gamble capping losses in the Dow to finish virtually unchanged.

S&P 500: 7,365.46 (-1.43%)

Nasdaq Composite: 25,587.04 (-2.22%)

Market Summary for Wednesday, June 24th

Wall Street wavered to a highly bifurcated, mixed close as heavy institutional distribution in several mega-cap technology and semiconductor components masked an overwhelmingly positive day of internal market breadth. Nearly two out of every three S&P 500 stocks advanced, yet the broader index finished slightly in the red due to its heavy capitalization weighting in tech titans like Microsoft (-2.3%) and Oracle (-4.6%). De-risking intensified ahead of Micron Technology's highly anticipated earnings report after the bell, causing Micron to shed another 6% during active trading.

Meanwhile, crude oil plummeted over 3%—with domestic benchmark WTI briefly dipping below the psychological $70 handle for the first time since early March—putting intense downward pressure on energy heavyweights like Exxon Mobil and Chevron. However, the drop in oil acted as an immediate inflation relief valve, dragging Treasury yields lower and supercharging interest-rate-sensitive homebuilders, with KB Home surging 16.7%.

S&P 500: 7,358.22 (-0.10%)

Nasdaq Composite: 25,476.64 (-0.40%)

Market Summary for Thursday, June 25th

Equity benchmarks spent the session locked in a grinding, flat-line consolidation as the market thoroughly digested Micron Technology's highly anticipated fiscal Q3 earnings report. Despite Micron delivering blowout top-line revenue of $41.46 billion and robust forward guidance, the stock suffered immediate post-earnings distribution, sliding roughly 2% as macro desks aggressively took profits on the news. The technology space remained highly sensitive, dragging the Nasdaq Composite into its fourth consecutive losing session—its longest negative streak since mid-February. Underneath the surface, market breadth remained remarkably healthy; small-caps and mid-caps heavily outpaced large-cap growth entities as capital continued to churn actively into traditional value segments. Fixed-income securities saw a steady influx of buyers, helping to cap any significant broader index downside ahead of Friday's core inflation data.

S&P 500: 7,357.49 (-0.01%)

Nasdaq Composite: 25,358.60 (-0.46%)

Market Summary for Friday, June 26th

Wall Street closed out the final session of June with a quiet, fractional decline at the index level, hiding massive underlying transaction volume and highly positive market breadth under the surface. The day was defined by the semi-annual Russell US Index reconstitution at the closing bell, which triggered the largest liquidity event in Nasdaq's history.

While the heavy capitalization-weighted benchmarks dipped slightly due to lingering pockets of technology and AI software distribution, more individual stocks rose than fell across the broader tape. Defensive healthcare sectors led the advancing cohorts, supercharged by a 7.1% surge in Eli Lilly following positive regulatory updates from the European Medicines Agency. Concurrently, Treasury yields and international oil prices continued to ease back to their baseline pre-friction levels, providing a long-term economic cushion as institutional desks successfully finalized their end-of-quarter portfolio rebalancings.

S&P 500: 7,354.02 (-0.05%)

Nasdaq Composite: 25,297.62 (-0.24%)

Notable Earnings (June 29th – July 3rd)

While the broader corporate earnings season won't begin in earnest until mid-July, next week features a highly influential micro-slate of reports that will serve as critical crosscurrents for specific industry sectors. Headlining the docket are key indicators for global consumer discretionary spending, defensive corporate staples, and specialized aerospace manufacturing.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, June 29th: AVAV / CNXC

Tuesday, June 30th: NKE / STZ / PRGS

Wednesday, July 1st: GIS / FDS / MSM

Thursday, July 2nd: LNN

Friday, July 3rd: US markets are closed (Independence Day)

Economic Calendar (June 29th – July 3rd)

Following a highly fragmented week defined by a violent rotational shakeout in mega-cap technology and a broad-based pivot into defensive havens, the macroeconomic spotlight intensifies. Volatility expectations remain elevated as the market cross-cuts into a new month, a new quarter, and the second half of 2026.

The absolute climax of the macro week arrives on a highly unusual timeline. Because domestic stock exchanges and banking systems are closed on Friday, July 3rd, in observance of the Independence Day holiday, the Bureau of Labor Statistics (BLS) will compress its schedule and unleash the June Non-Farm Payrolls employment report on Thursday morning.

Monday, June 29 – No major economic reports are scheduled to be released

Tuesday, June 30 – June S&P Global Final US PMI / China NBS PMIs

The final day of the second quarter brings the definitive reading on domestic business activity, mapping out production and services trajectories. Overnight, market participants will parse China's official manufacturing and non-manufacturing PMI prints, providing vital fundamental clues regarding global logistics flow and structural factory demand following the normalization of the Strait of Hormuz shipping lanes.

Wednesday, July 1 – ADP Employment Change & ISM Manufacturing PMI (June)

The institutional labor-market runway begins in earnest with the ADP private payroll print, offering a directional prelude to the official government data. Shortly after the opening bell, the Institute for Supply Management (ISM) drops its manufacturing report; after May's print showed the strongest factory expansion since 2022 at 54.0

Thursday, July 2 – May JOLTs Job Openings, Weekly Jobless Claims, & June Non-Farm Payrolls (NFP)

A true data gauntlet. The BLS drops the headline June Jobs Report twenty-four hours early, packing Non-Farm Payrolls, the national unemployment rate, and average hourly wage metrics into a singular pre-market shock wave. This will be running concurrently with May JOLTs job openings and weekly initial claims, testing broader market structure and interest rate expectations in a highly condensed, pre-holiday liquidity environment.

Friday, July 3 – Independence Day Holiday (U.S. Markets Closed)

Blue Sky Horizons

Blue Sky Horizons: Biocomputing & The DNA Data Revolution (Part II)

To appreciate how a tech stack becomes organic, we have to look past DNA's raw storage density and look at the actual workflow. In a traditional data center, files are saved by trapping electrons in silicon or shifting magnetic plates. In a biocomputer, digital data is literally grown.

The process bridges two worlds through a straightforward pipeline:

- Encoding: Software translates a file's binary code (1s and 0s) into the four-letter genetic alphabet: Adenine (A), Cytosine (C), Guanine (G), and Thymine (T).

- Writing: Specialized bio-printers use engineered enzymes—the same proteins nature uses to replicate cells—to assemble custom, data-carrying DNA strands on demand.

- Reading: When a file is requested, high-speed genetic sequencing machines read the chemical strands and decode them back into a clean digital format.

The primary challenge holding this technology back from replacing traditional server racks has always been retrieval speed. If an enterprise needs a single file, it shouldn't have to decode an entire pool of liquid to find it.

Engineers are solving this through molecular random access. By attaching unique chemical "barcodes" to the ends of specific data strands, the system can use standard laboratory amplification techniques to locate a file. When a user requests a document, matching chemical primers search the pool, bind only to that specific barcode, and replicate it millions of times within minutes. This forces the target data to float to the surface for instant reading while leaving the rest of the archive untouched.

The investable universe for this paradigm shift is moving rapidly out of academic labs and into corporate infrastructure. Long-term value is consolidating around the automated infrastructure bottlenecks: the firms holding the intellectual property for enzymatic printing, the developers of fluidic microchips that manage liquid logic gates, and the specialized data centers designing hybrid silicon-organic arrays.

As the cost of printing custom DNA continues its steady decline, the threshold for archiving permanent data is poised to shift from power-hungry silicon arrays to cold-storage molecular cells.

Thank you for reading. Until next week's close,

Have a safe and productive Trading week !

Fauzia Timberlake

About the Author: Fauzia Timberlake is a professional options coach and financial strategist specializing in risk management and portfolio architecture for self-directed investors. She is Founder and Managing Partner of Option Engines.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to consider and/or analyze, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the Trade Ideas tab on our website.