Markets Find Their Footing

By Fauzia Timberlake,

personal coach for trading options

July 5, 2026

Market Roundup & The Week in Review

The capital markets experienced a stabilizing, holiday-shortened consolidation during the week of June 29th through July 2nd, 2026. Following the previous week's volatile rotation, investors utilized the abbreviated schedule to re-evaluate equity valuations and interest rate trajectories ahead of the Fourth of July holiday.

The equity market saw a firming trend as participants looked past the prior week's tech-led distribution. While mega-cap technology remained sensitive to valuation concerns, broad indices managed to recoup some ground. The S&P 500 showed a resilient upward trajectory, up approximately 2.17% from the June 26th close. The Dow Jones Industrial Average likewise tracked higher, gaining 0.90% over the same period. Small-caps, represented by the Russell 2000 (IWM), remained tethered near the $297–$299 range, showing lower volatility compared to the deeper swings observed in the prior week.

Bond markets faced modest selling pressure as market participants recalibrated expectations following recent inflation data. The 10-Year Treasury yield, a key barometer for domestic credit, drifted higher throughout the week, climbing from an opening of 4.38% on Monday, June 29th, to close at 4.49% on Thursday, July 2nd. This shift suggests a degree of market skepticism regarding the pace of potential rate adjustments in the second half of the year.

WTI Crude extended its recent decline, falling from an opening of $70.75 on Monday to a Thursday close of $68.58. The market continued to digest the normalization of tanker traffic through the Strait of Hormuz, effectively removing the geopolitical risk premium that had supported prices earlier in the year.

Gold futures navigated a volatile week but ultimately found momentum toward the holiday. After a weak start on Monday (trading near $4,039), the metal staged a mid-week rally to finish the week at $4,135.15 on July 2nd. This represented a recovery of approximately 1.0% from the prior Friday's close, despite earlier pressures from a stronger dollar environment.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

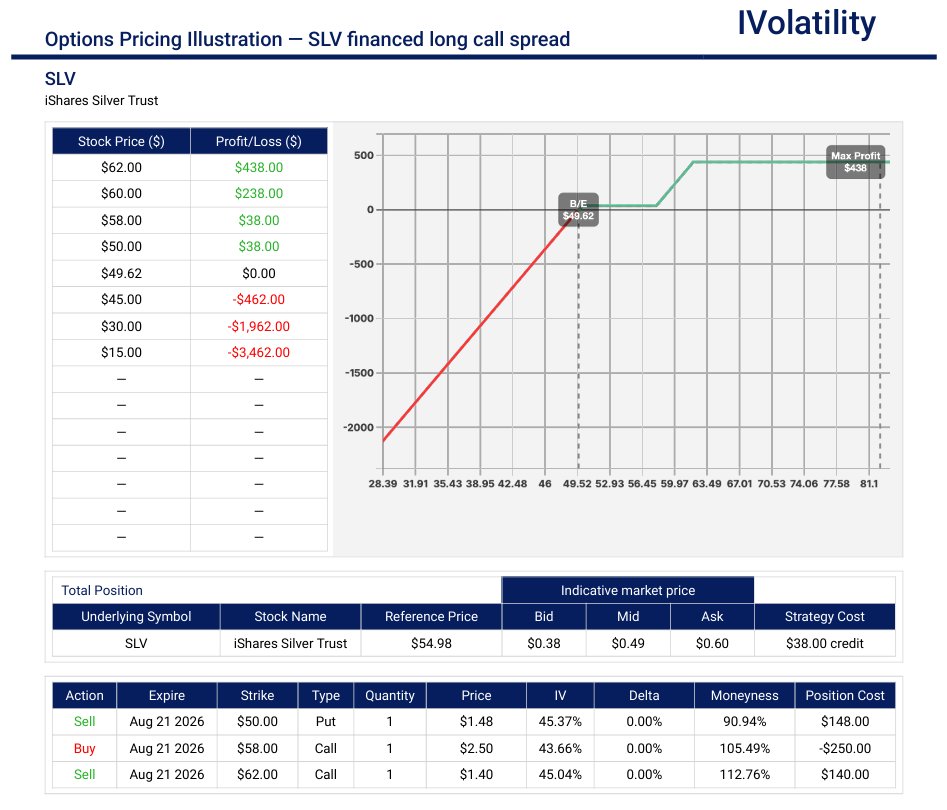

SLV (closed at 55.03 on Thursday, July 2nd)

While silver has endured significant volatility in the first half of 2026, the current environment offers a compelling case for a tactical rebound. The primary driver for a long-term bullish outlook is the structural imbalance in the global silver market. We are currently in the sixth consecutive year of a global supply deficit.

Outlook: bullish

Strategy: a financed long call spread

In the August monthly expiration, buy the OTM 58/62 long call spread and sell the 50 put to finance this purchase.

Premium collected is about 50c

Buying power held is about $700

Max potential profit is $450

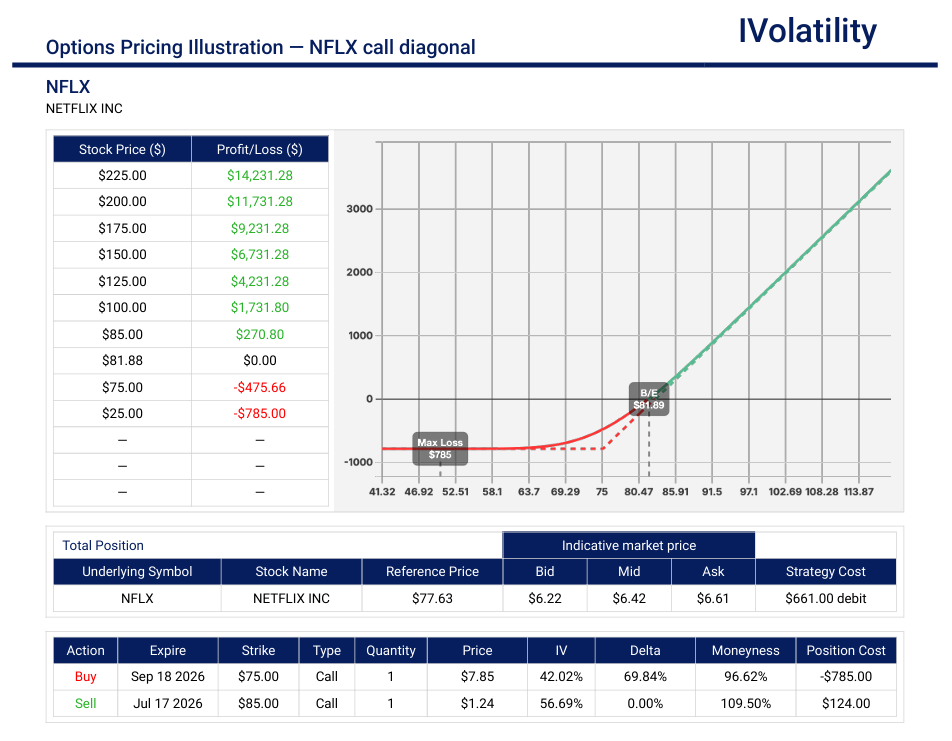

NFLX (closed at 77.61 on Thursday, July 2nd)

Netflix is no longer just a content library; it is a scaled advertising platform. With the ad-supported tier now reaching over 250 million monthly active users—representing nearly 45% of U.S. households—the company has effectively unlocked a high-margin revenue stream that is decoupled from pure subscriber acquisition.

Outlook: bullish

Strategy: Call diagonal

In the July 17th expiration, sell the 85 call

In the Sept 18th expiration, buy the 75 call

Debit paid is about $660

Maximum risk = debit paid

Maximum potential value about $1000

Movement of the Major Market Indices:

The major multi-asset benchmarks carved out a highly bifurcated path during the final week of June, exposing a massive structural drift beneath the index surface. Large-cap equity trackers faced intense distribution as an aggressive institutional profit-taking wave rippled through high-beta artificial intelligence and semiconductor structures. Traditional blue-chip value, defensive healthcare sectors, and small-cap assets caught a strong rotational bid, functioning as key capital sanctuaries.

| INDEX | UP | DOWN |

| SPY | 1.11% | |

| QQQ | -0.22% | |

| IWM | -0.28% | |

| DIA | 0.34% | |

| GLD | 2.04% | |

| BTC/USD | 3.41% | |

| 10-year yield | 2.51% | |

| Crude Oil | -3.07% | |

| VIX | -8.66% |

Movement of the Major Market Sectors:

The institutional positioning and calculated defense that anchored the market through the mid-June policy shifts accelerated into an aggressive, high-velocity capital redeployment campaign during the final full week of June.

| SECTOR | UP | DOWN |

| TECH (XLK) | -2.65% | |

| FINANCIALS (XL) | 3.58% | |

| INDUSTRIALS (XLI) | 1.25% | |

| ENERGY XLE | -1.46% | |

| HEALTHCARE (XLV) | 1.95% | |

| UTILITIES (XLU) | -1.02% | |

| MATERIALS (XLB) | -0.41% | |

| REAL ESTATE (XLRE) | -1.00% | |

| CONSUMER STAPLES (XLP) | 0.16% | |

| CONSUMER DISCRETIONARY (XLY) | 1.66% |

Notable Gainers Week of June 29th – July 2nd

Capital rotated aggressively into traditional value segments, defensive anchors, and major corporate restructuring stories.

- Comcast Corporation (CMCSA, +2.42%): Rocketed out of the gate on Monday morning after shocking the media landscape by announcing a strategic plan to completely spin off its NBCUniversal cable television networks and Sky broadband segments. The corporate streamlining effort sparked massive institutional accumulation with the stock closing the 4-day stretch as one of the top mega-cap performers.

- Apple Inc. (AAPL, +7.60%): Stood out as a major resilient anchor within the "Magnificent Seven" space. While chipmakers crumbled, Apple caught a strong, sustained institutional bid.

- Rivian Automotive (RIVN, +17.91%): Surged in the week after completely blindsiding short-sellers by raising its full-year 2026 delivery guidance to a range of 65,000 to 70,000 units, soundly outpacing the broader domestic EV market slowdown.

- Honeywell International (HON, +3.41%): Performed as a top industrial gainer during the quarter-end window-dressing pivot as institutional desks rotated capital into stable, high-quality industrial infrastructure.

Notable Losers Week of June 29th – July 2nd

The overriding narrative of the week was a harsh valuation reset across high-flying technology segments—particularly the semiconductor and artificial intelligence hardware space—alongside localized multi-month or 52-week lows hitting select telecom and fintech entities during intense end-of-quarter window dressing.

- Micron Technology (MU, -13.18%): Faced aggressive, multi-day distribution following its fiscal Q3 earnings report. Despite hitting robust baseline top-line metrics, macro desks aggressively treated the release as a "sell-the-news" signal. The selling intensified heavily into the holiday closure, with the stock plunging steeply.

- Lam Research (LRCX, -8.25%): the drop was sparked by a severe wave of automated and institutional liquidation, stretched valuations (trailing P/E exceeding 70x after a massive first-half surge) combined with warnings of slowing near-term system shipment growth and high-profile insider selling (Form 144 filings from the CEO and key executives).

- Teradyne (TER, -16.23%): Closely tied to the broader semiconductor equipment correction, this wide-moat semi-cap player experienced heavy profit-taking as capital migrated out of tech and into traditional value segments.

- T-Mobile US (TMUS, -2.46%): The largest mega-cap casualty of the telecom slide, falling 4.8% in a single session early in the week and printing a fresh 52-week low at $173.97

- Lumen Technologies (LUMN, -19.17%): Marked the worst overall performer of the week among heavily covered enterprise tech and telecom infrastructure entities.

Review selected market indices below:

Daily Notable Market Action

Market Summary for Monday, June 29th

Equity benchmarks started the final trading week of the first half of the year on a highly constructive note, staging a forceful relief rally to break a grueling five-day losing streak. The tech-heavy growth segments, which had borne the brunt of recent profit-taking, aggressively recaptured the driver's seat. Sentiment was majorly boosted by massive institutional capital commitment headlines out of Asia, where leading hardware players announced a combined $518 billion investment into a localized semiconductor manufacturing hub to satisfy the structural demands of generative AI. This immense infrastructure validation triggered a wave of short-covering and proactive accumulation across the semi-cap space, sending Applied Materials up more than 10% and driving mega-cap bellwether Nvidia back into positive territory. Despite a modest uptick in crude oil prices, fixed-income markets remained orderly, with the 10-year Treasury yield easing lower to provide a stable macro backdrop for equity desks. Under the surface, participation was healthily distributed as investors welcomed both the stabilization in high-flying growth segments and a media-sector shakeup from Comcast, pushing the S&P 500 to a clean percentage gain and setting an optimistic baseline for the upcoming quarter-end rebalancing window.

- S&P 500: 7,440.43 (+1.20%)

- Nasdaq Composite: 25,820.14 (+2.10%)

Market Summary for Tuesday, June 30th

Equity benchmarks closed out the final trading session of the first half of 2026 with a solid, broad-based advancement, as institutional window dressing and portfolio rebalancing provided a structural lift across the major averages. Volatility remained compressed throughout the day as macro desks actively finalized their quarter-end allocations, solidifying what has been a remarkably robust six-month campaign for equities. Tech-heavy growth segments found a steady bid, allowing the Nasdaq Composite to comfortably secure its best quarterly performance in six years, driven by the persistent institutional capital expenditures pouring into artificial intelligence infrastructure and advanced data centers. Underneath the surface, the broader market participation was notably constructive; seven out of the eleven primary S&P 500 sectors wrapped up the month in positive territory, with traditional value segments and industrials leading the charge. While fixed-income markets saw modest adjustments as participants evaluated the Federal Reserve's evolving monetary timeline, the equity landscape remained firmly resilient, logging an optimistic finish to the second quarter before the holiday-shortened July trading cycle officially gets underway.

- S&P 500: 7,499.36 (+0.22%)

- Nasdaq Composite: 26,213.11 (+0.67%)

Market Summary for Wednesday, July 1st

The market's mid-week session was characterized by a distinct tug-of-war, with broad-based gains in value and consumer-facing segments clashing with heavy, persistent selling pressure in high-valuation technology names. Investors reacted favorably to a cooling report on U.S. manufacturing from the Institute for Supply Management, which showed a deceleration in growth and a welcome easing in price pressures; this combination sparked a bond market rally as Treasury yields retreated from their morning peaks, providing a structural lift to the broader market. Despite this tailwind, the index-heavy AI and semiconductor cohort faced another wave of aggressive liquidation, with high-flyers like Micron Technology and Advanced Micro Devices suffering double-digit percentage drops as traders continued to unwind overextended valuations. Ultimately, the rotation into defensive and consumer-staples sectors was insufficient to offset the tech-led drag, leaving the major benchmarks to post a fractional retreat on the day.

- S&P 500: 7,483.23 (-0.22%)

- Nasdaq Composite: 26,040.03 (-0.66%)

Market Summary for Thursday, July 2nd

Equity benchmarks delivered a highly fragmented, mixed performance to close out the holiday-shortened trading week, as a stark divergence emerged between mega-cap technology names and the broader market. The session opened to a wave of buying fueled by the June Non-Farm Payrolls report, which revealed cooler-than-expected hiring. Macro desks immediately interpreted the softer labor data as a "bad news is good news" signal, pushing CME FedWatch odds for a rate hike at the upcoming July meeting down significantly and sending the Dow Jones Industrial Average rallying nearly 600 points to a fresh record high. Under the surface, market breadth was exceptionally robust, with roughly 70% of S&P 500 components finishing the day in positive territory. However, the tech-heavy Nasdaq Composite faced severe, persistent distribution as the artificial intelligence momentum trade experienced another round of heavy profit-taking. Semiconductor bellwethers led the decline, with Micron Technology sliding another 5.5% and Lam Research plunging over 10% on intensifying concerns over near-term sector valuations. This localized semi-cap drag managed to completely cap the early gains for the broader indexes, pulling the Nasdaq into deep negative territory while pinning the S&P 500 to a flat-line finish ahead of Friday's Independence Day exchange closures.

- S&P 500: 7,483.24 (+0.00%)

- Nasdaq Composite: 25,382.67 (-0.81%)

Market Summary for Friday, July 3rd

US Capital Markets were closed on this day in observance of the Independence Day holiday.

Notable Earnings (July 6th – July 10th)

We are lingering in the quiet "calm before the storm" phase of the corporate earnings cycle. While the major technology bellwethers and money-center financial institutions won't begin revealing their second-quarter scorecards until mid-month, this interim week provides critical early test cases for structural margins and corporate spending trends. Traders will be looking closely at early reporters in consumer staples and niche industrials to see if firms are successfully passing persistent input costs down to a stretching consumer base.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, July 6th: No notable earnings reports are scheduled

Tuesday, July 7th: STZ / GIS / MSM

Wednesday, July 8th: No notable earnings reports are scheduled

Thursday, July 9th: WDFC / PSMT

Friday, July 10th: No notable earnings reports are scheduled

Economic Calendar (July 6th – July 10th)

The holiday-shortened trading schedule resets to a standard five-day rhythm. With the compressed frenzy of the June payroll report now behind us, the macro narrative shifts its focus to monetary policy transparency and the health of the consumer engine. The climax of the upcoming macro week arrives on Wednesday afternoon with the release of the June FOMC meeting minutes. Traders will be dissecting every syllable for policy clues, especially following the recent dot plot shift under Chairman Warsh that signaled a lone, final 25-basis-point hike left on the 2026 horizon.

Monday, July 6th

- Eurozone Retail Sales (9:00 AM GMT): A key early-morning gauge of European consumer health.

- ISM Services PMI (10:00 AM ET): The premier domestic data point of the day, tracking the critical services sector which commands roughly 80% of US GDP.

Tuesday, July 7th

- No Major Domestic Releases Scheduled

Wednesday, July 8th

- MBA Mortgage Applications (7:00 AM ET): Weekly gauge of residential lending and housing demand.

- EIA Petroleum Status Report (10:30 AM ET): Weekly crude inventories data.

- FOMC Meeting Minutes (2:00 PM ET): The week's premier event. The street will look for deeper insight into the Fed's newfound focus on structural price stability and the internal debate over removing prior rate-cut language.

Thursday, July 9th

- Initial Jobless Claims (8:30 AM ET): The standard weekly health check on labor market layoffs.

- China Consumer Price Index (CPI) (9:30 PM ET): A late-night look at global deflationary or inflationary undercurrents from the world's second-largest economy.

Friday, July 10th

- German Final CPI (2:00 AM ET): Finalized June inflation tracking for Europe's economic core.

- Canadian Unemployment Rate (8:30 AM ET): June labor market data from our northern neighbor, providing cross-border economic context.

Blue Sky Horizons

Blue Sky Horizons: Biocomputing & The DNA Data Revolution (Part 3)

Last week, we explored the theoretical power of DNA data storage—how a single gram of synthetic DNA can house 215 petabytes of data, condensing an enterprise data center into a single drop of water. This week, the narrative shifts from biological concepts to functional engineering. Biocomputing is officially crossing the chasm into a deployable, programmable execution layer integrated with digital infrastructure.

The core hurdles holding back DNA computing have always been physical. Traditional molecular DNA circuits were historically single-use, consuming themselves during biochemical processing. Furthermore, biological material was considered too fragile to withstand the harsh thermal and electronic environments of enterprise computing.

Two massive breakthroughs published in April 2026 have completely shattered these structural limits, reshaping how we think about future AI infrastructure.

A research team at the Korea Advanced Institute of Science and Technology built a reset-free DNA logic circuit capable of real-time input processing and persistent memory. By designing synthetic DNA molecules that alter their physical binding configurations without destroying themselves, they created the molecular analogue of a semiconductor transistor. Operating at a base-pair distance of just 0.34 nanometers, this engineering bypasses the upcoming physical scale limits of 2-nanometer silicon.

Researchers at Penn State engineered a bio-hybrid platform bridging synthetic biology with electronic hardware. By doping silver-ion-infused DNA sequences directly into a crystalline perovskite semiconductor, they manufactured "memristors" (memory resistors) that mimic human synaptic plasticity. This hybrid structure survives extreme operational thresholds up to 121°C and processes logic and memory on the exact same substrate at ultra-low voltages (less than 0.1V), cutting energy overhead by 90% to 100x compared to standard electronic memory.

The institutional money trail is forming rapidly. Market data released this quarter projects the global DNA data storage market to explode from $272.8 million in 2026 to $80.2 billion by 2035—a compounding annual growth rate (CAGR) of 88%.

We are seeing the early formation of a standardized biocomputing tech stack, where advanced biofoundries handle the biological orchestration while next-generation ASICs and nano-scale electrochemical cell arrays scale up synthesis throughput. As traditional data centers approach a hard thermodynamic wall under the crushing power demands of generative AI, the convergence of synthetic biology and advanced materials is providing the emerging blueprint for sustainable, ultra-high-density supercomputing.

Thank you for reading. Until next week's close,

Have a safe and productive Trading week!

Fauzia Timberlake

About the Author: Fauzia Timberlake is a professional options coach and financial strategist specializing in risk management and portfolio architecture for self-directed investors. She is Founder and Managing Partner of Option Engines.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to consider and/or analyze, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the Trade Ideas tab on our website.