VIX

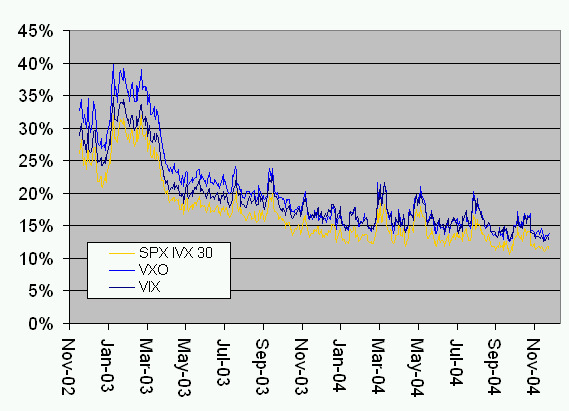

The CBOE Volatility Index, or VIX, is a measure of implied volatility on S&P 500(ticker SPX) options. Before September 2003 CBOE offered similar indicator for the S&P 100 options - this indicator is till available (ticker VXO). Launched in 1993, the VIX has now become a fixture on many a trader's monitor and the home page to many financial web sites. It can be called the market's "fear gauge". During times of uncertainty and market turmoil, the VIX will rise to reflect greater expectations regarding future volatility. When the VIX rises, it is a sign of investors' nervousness; when the VIX falls to low levels, it suggests investor bullishness or complacency. The CBOE Volatility Index has historically remained above the actual historical volatility of the SPX (OEX before September 2003)

The VIX is based on S&P 500 index option prices and incorporates information from the volatility "skew" by using a wider range of strike prices rather than just at-the-money series. Please refer to CBOE website for a complete description of VIX calculation: https://www.cboe.com/micro/vix/vixwhite.pdf (requires Adobe Acrobat Reader). One of its advantages, compared to our IV Index, is that VIX value is basically independent of the model used to derive implied volatilities - VIX is calculated as a weighted average of option prices. It is a relatively advanced topic, but indeed you can derive stock implied volatility without calculation of model-specific single option's implied volatilities. This technique is widely used for pricing Variance Swaps. This technique can be used only if you have a thick grid of activeky traded strikes though. This, of course, is true for the S&P 500, but not for the majority of optionable stocks. That's why we stick to our model-dependent way of calculating IV Index - it allows us to calculate this measure for each individual stock, not for the market in general.

Like the VIX, our 30-day IV Index looks at actual option premiums quoted in the market. We have taken great care to perfect our analysis of this data, resulting in higher quality signals. Any given expiration month can have over 50 different strikes, with each strike exhibiting differences in implied volatilities. Add to that, differences in implied volatilities between puts and calls, and you have a very complex problem in trying to estimate the market's expectation of future volatility. We believe that our approach to calculating implied volatilities produces a more accurate estimate of the market's expectations, is more valid in making comparisons from one day to the next, and provides a better indication of market sentiment based on option premiums. Note that the "new" CBOE VIX is much closer to IVolatility.com SPX IV Index than the "old" one (VXO).

For more information about the VXO, VIX and IV Index - see the following articles:

Implied Volatility Index and related indicators: How you can use them in trading & risk management