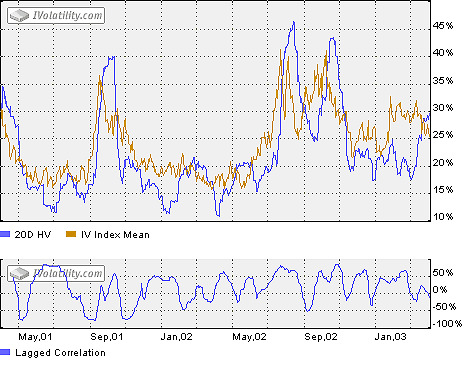

Lagged Correlation

Lagged correlation is defined as correlation between 20 days historical Volatility and 30days implied Volatility index shifted back in time by one month. As HV indicates Volatility in the past month and the IVIndex is Volatility expected in the nearest 30 days, lagged correlation is a good measure of how predicted Volatility (IV) correlates with realized (HV) over the same period.

\( LAG_{cov}(IV,HV)= \frac{1}{n-1}\displaystyle\sum_{t=1}^{n}(HV_t - averHV)(IV_t - averIV) \)

\( \text{LAGcor}(IV, HV) = \frac{\text{LAGcov}(IV, HV)}{\sqrt{\text{var} HV} * \sqrt{\text{var} IV}} \)

Lagged correlation is calculated for n= 30 days.

Chart: Lagged correlation vs 20d HV and 30d IV Index for DJX.

Chart: Lagged correlation vs 20d HV and 30d IV Index for DJX.

Note: those charts are available to Advanced

Historical Data service subscribers.