Volatility Skew

Volatility skews occurs where two or more options on the same underlying asset have considerable differences in implied volatility. There are two type of volatility skews: volatility time skew, volatility strike skew. Volatility skew can be used to identify trading opportunities.

IVolatility.com services allow for examination and analysis of the volatility time and strike skews to effectively capitalize on these opportunities.

Volatility strike skew

The Black-Scholes model suggests that every option imply the same volatility for underlying, but as it can be seen from practice every option implies different volatility. Implied volatility often tends to be higher for out-the-money (OTM) and in-the-money (ITM) options compared to at-the-money, in this case OTM and ITM options represent increased risk on potentially very large movements in the underlying; to compensate for this risk, they tend to be priced higher. This phenomena is known as a volatility smile. Sometimes Implied Volatility for OTM and ITM options is lower than for ATM.

Volatility smile

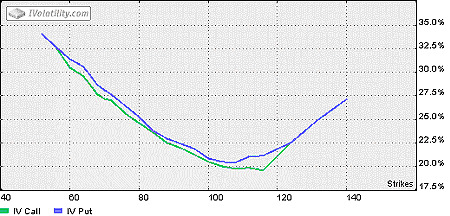

The following chart shows volatility for options with the same expiration but different strikes. The relationship between strike price and implied volatility is known as "volatility smile". The volatility smile shows that deep out-the-money and deep in-the-money options are priced by the market higher than theoretically forecasted by the formulas based on the lognormal distribution. The volatility smile is quite typical for options on currency.

Chart: Volatility smile

Chart: Volatility smile

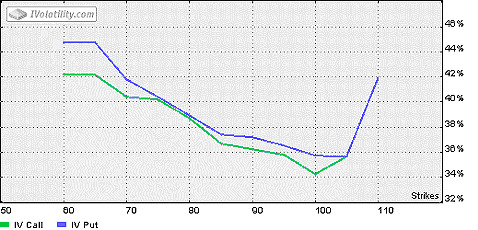

As a general rule, the lowest point of the volatility smile tends to correspond to the ATM strike, but this is not always the case. Often the lowest point can be found to the right of the ATMs, that is the upside "calls" relative to the ATMs. There is a natural bias in the markets for institutions to "write" upside calls against large long positions they hold in the underlyings as a way to increase returns. The market adjusts by shifting the lowest point of the smile to the right side to compensate for these "natural" sellers of options. If plotted independently, the put smile would have the same low point because at each strike the put and call, in combination with the stock, can be arbitraged against each other and thus they are adjusted accordingly. The low point of the volatility smile can be shifted to the left side too, but this occurs less frequently in the markets. This phenomena was more prevalent during the extended bull market when many companies sold puts against their own heavily promoted stocks.

For example see the following chart. This chart shows a volatility smile for IBM. The lowest point corresponds to the strike = $110, while the price of IBM is $82.79. It means that the lowest point of smile does not correspond to the ATM strike.

Chart: Volatility smile with shifted lowest point

Chart: Volatility smile with shifted lowest point

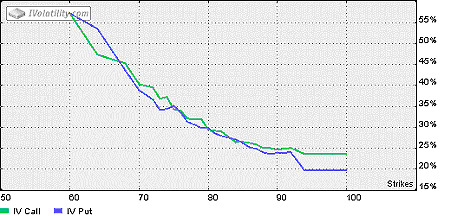

Volatility smirk

Often, the shape of the volatility smile for options on shares or an index is called a "volatility smirk", because of its ascending line.

Chart: Volatility smirk for DJX (expiration in April 2003).

Chart: Volatility smirk for DJX (expiration in April 2003).

The volatility smirk shows that deep in-the-money calls and deep out-the-money puts cost more than theoretically forecasted by the Black- Sholes formula, while deep out-the-money calls and deep in-the-money puts cost less. This type of shape of the volatility smile reveals that options sellers believe it is much more likely to suffer losses from selling out-the-money puts than out-the money calls.

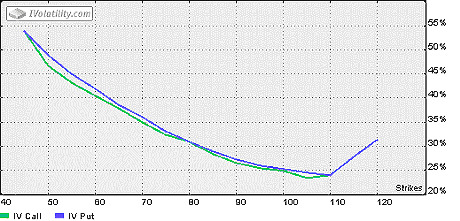

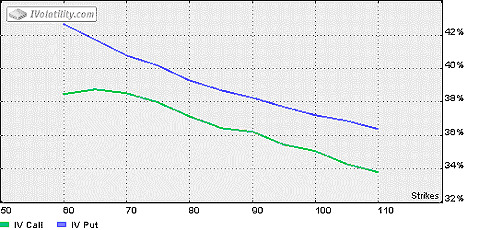

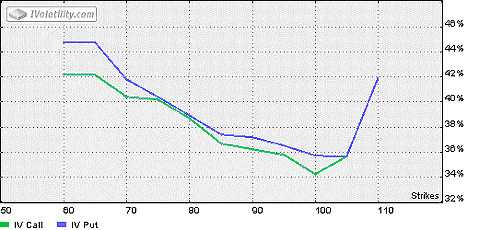

The shape of a volatility curve also depends on the number of days remaining until expirations. In most cases the smile becomes more clearly defined as expiration approaches. (See volatility charts for OSX for May 2003 and December 2003)

Chart: Volatility curve for OSX (expiration in December 2003).

Chart: Volatility curve for OSX (expiration in December 2003).

Chart: Volatility curve for OSX (expiration in May 2003).

Chart: Volatility curve for OSX (expiration in May 2003).

Note, the volatility of call can differ from the volatility of put with the same strike and expiration; It indicates the market's bias toward calls or puts. On the site you can see the volatility smile for call and put options displayed separately. If the ratio of Call Volatility to Put Volatility is greater than 100%, it means that Calls are priced higher than Puts. This shows that the market has a positive bias toward the upside. If the ratio of Call Volatility to Put Volatility is less than 100%, then puts are being valued higher. A large difference or spread between call and put volatilities often suggests a strong bias in the market's opinion of the stock.

Volatility time skew

Volatility time skew occurs where options with the same strike but with different number of days remaining until expiration have different volatility.